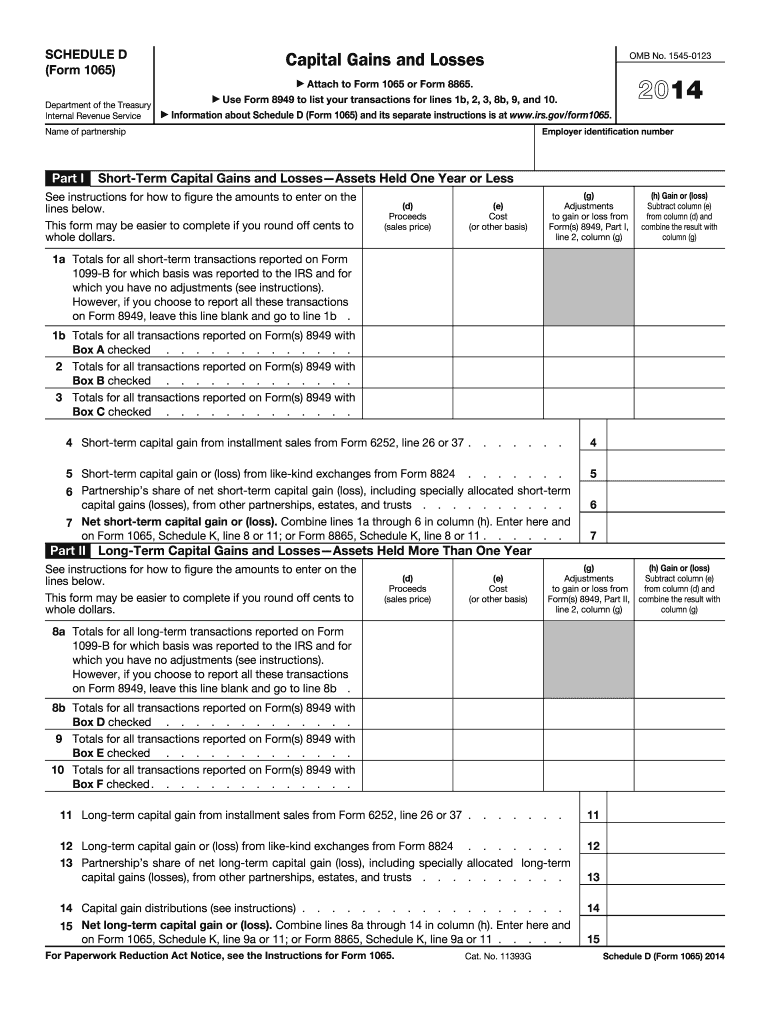

Definition and Significance of Schedule D (Form 1065)

Schedule D (Form 1065) is a crucial document required by the Internal Revenue Service (IRS) for partnerships to report capital gains and losses. It is part of the annual tax filing requirements and plays an essential role in determining the net capital gains or losses that affect a partnership's taxable income. This form consolidates various transactions, both short-term and long-term, outlining the proceeds, costs, and subsequent gains or losses. The completion of Schedule D is vital for achieving tax compliance and avoiding potential discrepancies in reported earnings.

How to Use Schedule D (Form 1065)

Proper usage of Schedule D involves a clear understanding of the form's structure and what it encompasses. Partnerships must detail each transaction that involves capital assets. This includes reporting figures from Form 8949, which itemizes each sale or exchange of assets. When completing Schedule D, ensure that all required calculations for net capital gains or losses are accurate. Cross-reference with other forms and schedules to maintain consistency in reporting.

Obtaining Schedule D (Form 1065)

Schedule D can be obtained directly from the IRS website. As part of the 1065 tax package, it is available for download in PDF format. Partnerships can download and print the form as necessary for filing purposes. For digital filing, many tax software providers incorporate Schedule D into their workflow, allowing for direct access and completion within the software environment.

Steps to Complete Schedule D (Form 1065)

- Gather Transaction Data: Collect all relevant documentation regarding capital asset transactions, including purchase and sale details.

- Complete Form 8949: Report each capital transaction on Form 8949, ensuring that all entries are accurate and complete.

- Transfer Totals to Schedule D: Summarize the information from Form 8949 onto Schedule D, categorizing gains and losses as short-term or long-term.

- Calculate Net Gain/Loss: Follow IRS guidelines to compute the overall net capital gain or loss for the tax year.

- Review and Submit: Double-check all figures for accuracy before submission. Ensure that Schedule D aligns with the partnership's overall tax filings.

Key Elements of Schedule D (Form 1065)

- Short and Long-Term Transactions: Clearly distinguish between transactions held for one year or less and those held for more than one year.

- Capital Gain Distributions: Include any capital gain distributions received from mutual funds or other investment vehicles.

- Adjustment Codes: Properly use IRS-specified codes to adjust gains or losses for special situations as required by tax laws.

Important Terms Related to Schedule D (Form 1065)

- Capital Assets: Generally includes stocks, bonds, and property owned for investment purposes.

- Basis: The original value of an asset for tax purposes, which is used to determine gain or loss upon sale or disposition.

- Proceeds: The total amount received from the sale or exchange of a capital asset.

Examples of Using Schedule D (Form 1065)

Consider a partnership that has several investments in stocks and real estate. Throughout the tax year, they sold multiple properties and shares. Each transaction—whether resulting in a capital gain or loss—must be calculated and documented on Schedule D to ensure accurate tax reporting. This ensures correct tax obligations are met and provides a clear picture of the partnership’s financial activities.

Required Documents for Schedule D (Form 1065)

To complete Schedule D, partnerships should have the following documents on hand:

- Transaction Records: Confirm purchase and sale dates and amounts for all capital assets.

- Form 8949: As a component of Schedule D reporting, completed Form 8949 entries are essential.

- Financial Statements: Include any relevant statements that provide additional context or verification of reported transactions.

Filing Deadlines and Important Dates

Partnerships must adhere to IRS deadlines to avoid penalties. Schedule D typically accompanies Form 1065, which is due on March 15th for calendar year partnerships. If more time is needed, a six-month extension may be requested, moving the deadline to September 15th. Staying aware of these deadlines helps maintain compliance and avoids unnecessary financial penalties.