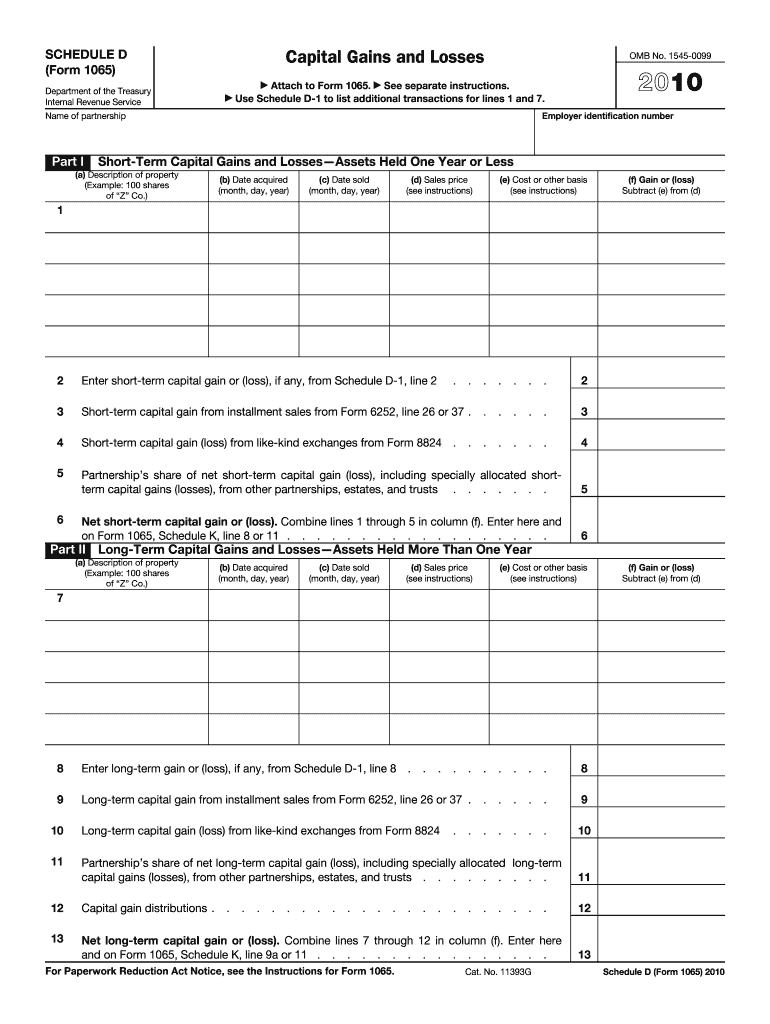

Definition and Purpose of the 2010 Schedule D (Form 1065)

The 2010 Schedule D (Form 1065) is used by partnerships to report both short-term and long-term capital gains and losses. These pertain to assets a partnership holds for one year or less for short-term gains, and more than one year for long-term gains. The form is essential for detailing property descriptions, acquisition and sale dates, sales prices, costs or other bases, and the total gain or loss. This separation aids in more accurate tax reporting as different tax rates apply to short and long-term capital gains and losses.

Steps to Complete the 2010 Schedule D (Form 1065)

-

Gather Required Information: Initially, collect all pertinent details related to your partnership’s capital assets. This includes acquisition dates, original purchase prices, and the date and sale price of the asset.

-

Determine Holding Period: Identify whether each asset qualifies as short-term or long-term based on the holding period. This distinction affects how gains and losses are reported.

-

Calculate Gains and Losses: Use the provided calculation sections to determine the gain or loss for each transaction. This involves subtracting the asset's original purchase price (or cost basis) from the final sale price.

-

Complete Each Section: Enter all calculated gains and losses into the form, ensuring the correct sections are used for short-term and long-term assets.

-

Reconcile Totals: Sum all listed transactions to determine your partnership's total capital gains or losses for the year.

Who Uses the 2010 Schedule D (Form 1065)

Typically, partnerships engaged in buying and selling assets use the 2010 Schedule D (Form 1065) to determine and report their capital gains and losses. This includes businesses that might have a range of investments or fixed assets, such as real estate holdings or securities. Importantly, the form allows partnerships to fulfill their tax obligations correctly by ensuring all gains and losses are accurately recorded and reported.

IRS Guidelines for the 2010 Schedule D (Form 1065)

The IRS provides specific guidelines to aid partnerships in correctly filling out the 2010 Schedule D. These guidelines emphasize the distinction between short-term and long-term transactions, proper documentation of sales, and ensuring that the form reflects all capital gain or loss activities within the tax year. The IRS stresses maintaining comprehensive records and understanding the tax implications of capital gains or losses for annual tax return accuracy.

Key Elements of the 2010 Schedule D (Form 1065)

- Property Descriptions: Detailed descriptions of the assets involved are essential for clarity and record-keeping.

- Transaction Dates: The form requires specification of both acquisition and sale dates to accurately assess the holding period.

- Sales Price and Costs: Listing the exact sales prices alongside the acquisition costs or other bases is necessary for precise calculations.

- Total Calculated Gains/Losses: The form culminates in the tally of gains and losses, providing a final number for tax obligations.

Important Terms Related to Capital Gains and Losses

- Short-Term Gain: Gains from the sale of an asset owned for one year or less, usually taxed at a higher rate.

- Long-Term Gain: Gains from the sale of an asset held for more than one year, often taxed at a more favorable rate.

- Cost Basis: The original value of a purchased asset, essential for calculating gains or losses.

- Capital Asset: Any significant piece of property (including stocks) that a partnership may own and sell.

Penalties for Non-Compliance

Failure to properly complete and file the 2010 Schedule D (Form 1065) can lead to significant penalties from the IRS. These might include fines for late submission or inaccuracies in the reported information. It is vital for partnerships to ensure thorough completion of the form and timely filing to avoid these potential costs.

Software Compatibility and Integration

Many modern accounting software applications, such as TurboTax and QuickBooks, support the 2010 Schedule D (Form 1065). These tools can simplify the process by auto-importing transaction data and conducting necessary calculations. This integration helps ensure accuracy and efficiency, particularly for partnerships managing numerous transactions and assets.