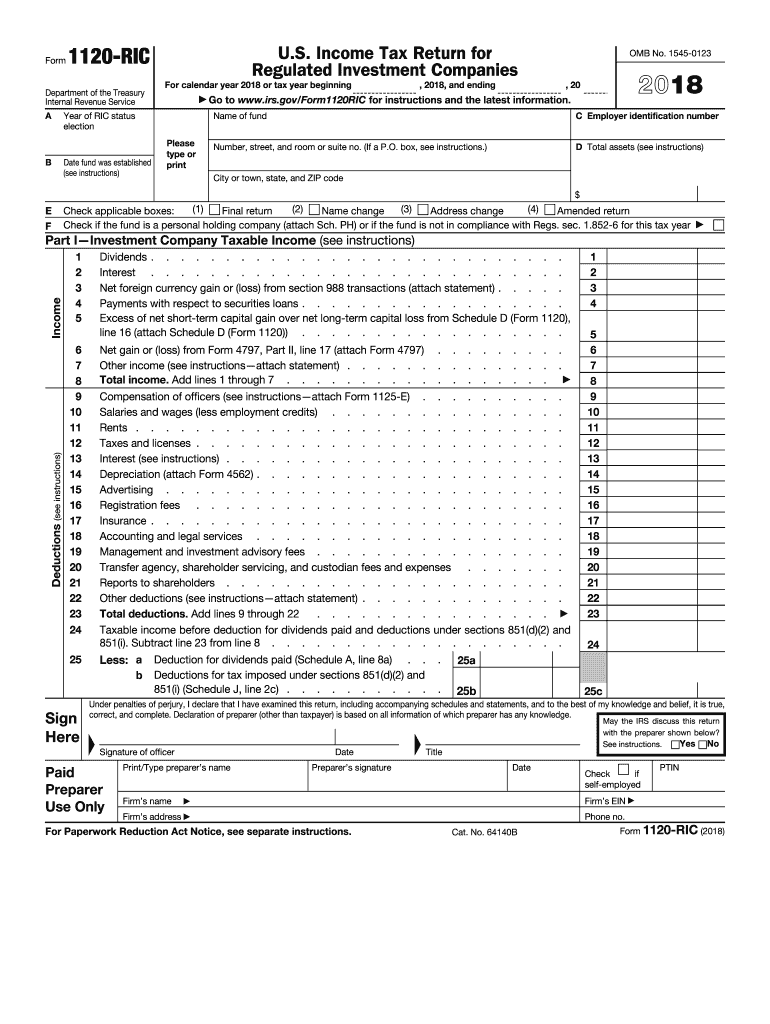

Definition and Meaning of RIC 2015

The "RIC 2015" pertains to Form 1120-RIC, used by Regulated Investment Companies (RICs) to report their income, deductions, and taxable earnings for the tax year in question. This form is crucial for entities such as mutual funds, which must declare their financial activity and compliance with regulations set forth by the Internal Revenue Service (IRS). The form establishes the framework within which these companies report figures like net investment income, capital gains, and the dividends paid to shareholders, adhering closely to the provisions within the IRS code.

Steps to Complete the RIC 2015

-

Gather Required Documents: Ensure you have all necessary financial statements, previous tax returns, and dividend records to accurately report on the form.

-

Calculate Income and Deductions: Start with reporting gross revenue before moving on to specific deductions, including operational costs and dividends paid.

-

Complete Tax Schedules: Fill out associated schedules that detail capital gains, losses, and any applicable tax credits or adjustments.

-

Verify Accuracy: It’s crucial to double-check all figures and calculations to ensure compliance and avoid penalties for erroneous submissions.

-

Submit the Form: Depending on operational preferences, you can either submit the form electronically or via mail to the IRS before the filing deadline.

Who Typically Uses the RIC 2015

Regulated Investment Companies, notably mutual funds and certain investment trusts, are the primary users of the RIC 2015. These entities must report financial activities that affect their shareholders, which include distributing dividends, capital gain distributions, and any other taxable events. The necessity to file this form arises from the specific tax treatment provided to RICs, which allows them to avoid double taxation under certain conditions.

Key Elements of the RIC 2015

- Income Reporting: Includes all income derived from investments, such as interest, dividends, and capital gains.

- Deduction Details: Lists applicable deductions, such as management fees, distribution costs, and advertising expenses.

- Dividends Paid Deduction: An important element allowing RICs to deduct distributions to shareholders, thereby minimizing taxable income.

- Tax Computation: Assesses the overall tax liability after accounting for various tax credits and adjustments.

IRS Guidelines for Filing RIC 2015

The IRS provides explicit guidelines that Regulated Investment Companies need to follow while filling out the 2015 form. These guidelines cover the classification of income, allowable deductions, and specific IRS codes that apply to the calculations on the form. Following these guidelines is crucial for compliance and to prevent potential audits or penalties due to misreporting or omissions.

Filing Deadlines and Important Dates for RIC 2015

The typical due date for filing the RIC 2015 corresponds with the 15th day of the third month after the end of the company’s tax year, usually March 15. Extensions are available upon filing Form 7004, which can grant an additional six-month period. Keeping track of these deadlines is crucial for maintaining good standing with the IRS and avoiding late filing penalties.

Examples of Using the RIC 2015

Consider a mutual fund managing a diversified portfolio. By completing the RIC 2015, the fund can accurately report its earnings, deductions, and dividends paid to shareholders. This not only ensures compliance with tax laws but also optimizes tax obligations by leveraging allowable deductions. For instance, if a fund distributes most of its revenue through dividends, it significantly reduces its taxable income.

Penalties for Non-Compliance

Failing to file the RIC 2015 or inaccurate submissions can result in substantial penalties from the IRS. These include fines assessed on a monthly basis for late submissions and additional penalties for underreporting income. Misinterpretation or disregard of filing requirements can lead to audits or investigations, ultimately impacting the credibility and financial standing of the company.