Definition and Meaning

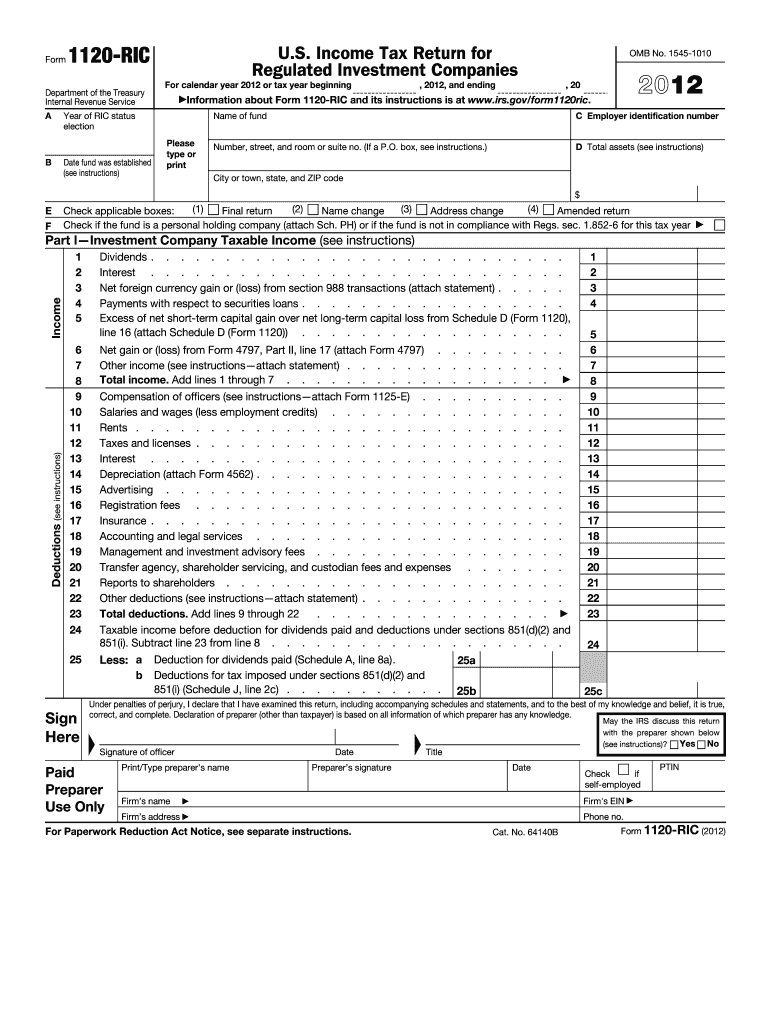

The 2012 Form 1120-RIC is a U.S. Income Tax Return specifically designed for Regulated Investment Companies (RICs). It's a critical form used by funds that qualify as RICs to report their earnings, taxes owed, and deductions. These funds often include mutual funds and certain exchange-traded funds (ETFs) that distribute income to shareholders. The form captures crucial details about investment income, compliance with the Internal Revenue Code (IRC) specifically applicable to investment companies, and statutory income distribution requirements.

Who Typically Uses the 2012 Form 1120-RIC

This form is primarily used by Regulated Investment Companies, which are typically mutual funds and ETFs operating under the terms outlined in Subchapter M of the IRC. These companies must meet specific requirements, such as distributing a substantial portion of their income to shareholders, to qualify for favorable tax treatment. The IRS grants RIC status to companies whose business involves investment in securities and who comply with specific asset diversification and income distribution laws.

Key Elements of the 2012 Form 1120-RIC

Income and Deductions

- Gross Income: Includes interest, dividends, and other taxable amounts.

- Deductions: Operating expenses, advisor fees, and other eligible costs which can be subtracted from gross income.

Tax Calculations

- Taxable Income: After deductions, this is the figure used to determine tax liabilities.

- Applicable Tax Rates: Specific rates applied to the RIC's taxable income.

Compliance and Reporting

- Distribution Requirements: Details on the legal requirement to distribute at least 90% of taxable income to shareholders.

- Asset Holdings: Information on the diversification of the fund's investments to meet regulatory standards.

Steps to Complete the 2012 Form 1120-RIC

- Gather Necessary Documents: Financial statements, records of income and expenses, and documentation of distributions to shareholders.

- Fill Out Income Section: Report all types of income, including dividends and interest.

- List Deductions and Expenses: Accurately document all allowable deductions and expenses incurred during the taxable year.

- Calculate Tax Owed: Use provided rates to determine the tax liability based on taxable income.

- Ensure Compliance Information is Complete: Check all distributions and asset diversification requirements are met to qualify as a RIC.

IRS Guidelines

- Record Maintenance: Ensure all financial data is precise, and the fund is prepared for any audits.

- Filing Requirements: Must be submitted within a specific period post-year-end of the regulated investment company.

- Additional Schedules: Use any applicable schedules for foreign investments or other special cases.

Filing Deadlines and Important Dates

Make sure to align the filing of the 2012 Form 1120-RIC with the tax year-end of the RIC, typically by March 15th following the close of the tax year. Extensions can be sought if required, often granting an additional six months.

Penalties for Non-Compliance

Failure to file on time or inaccurately reporting tax obligations can result in severe penalties from the IRS. These might include monetary fines and potential loss of RIC status, which would alter the tax treatment of the investment company drastically.

Form Submission Methods

Forms can be submitted electronically or via mail. Each method has specific instructions available for ensuring the secure and verified submission of the form. Given the importance of timely filing, electronic submission is recommended for faster processing and immediate confirmation.

Eligibility Criteria

To be eligible to use Form 1120-RIC, companies must:

- Be registered as a regulated investment company

- Comply with the IRS's income distribution and asset diversification mandates

- Maintain proper documentation to validate their tax position and RIC status

Ensuring compliance with these criteria is fundamental to optimizing tax advantages and maintaining lawful operational status.