Definition & Purpose of Form 1120-RIC

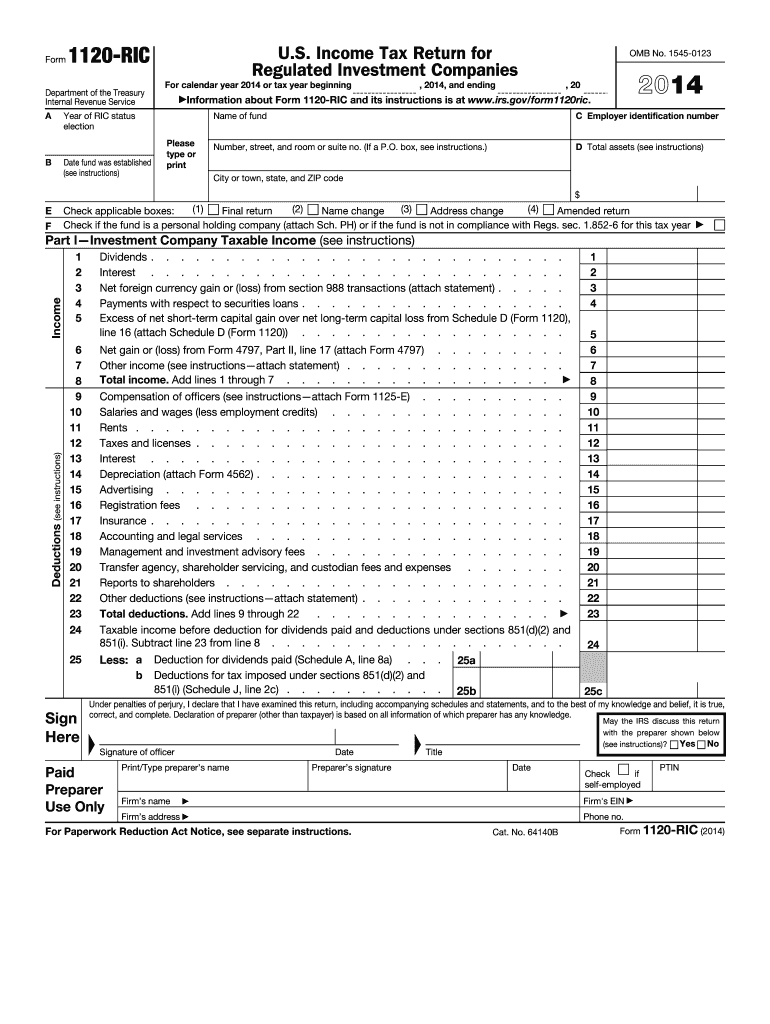

Form 1120-RIC is defined as a U.S. Income Tax Return specifically for Regulated Investment Companies (RICs). This form is vital for companies that manage mutual funds, ETFs, and other investment fund types to report their income, deductions, and tax obligations to the IRS. The primary goal is to determine the taxable income of these entities and ensure compliance with federal tax regulations.

- Regulated Investment Company: An RIC is an entity, like a mutual fund, that meets specific IRS criteria, enabling it to pass its earnings, profits, or gains directly to shareholders to avoid being taxed at the corporate level.

- Relevance: Completing Form 1120-RIC is crucial for RICs to maintain their tax status and ensure that income received does not undergo double taxation, protecting both the corporation and individual investors.

Steps to Complete Form 1120-RIC

Completing Form 1120-RIC requires careful attention to detail and understanding of each section.

-

Gather Financial Data: Begin by collecting relevant financial documents, including records of income, expenses, and distributions.

-

Fill in General Information: Input basic details such as the company's name, address, and Employer Identification Number (EIN).

-

Report Income: List all income sources, including interest, dividends, and capital gains, ensuring all amounts align with supporting documentation.

-

Deductible Expenses: Identify allowable deductions, such as management fees and shareholder communication expenses, to reduce taxable income.

-

Calculate Taxable Income: Subtract deductions from total income to determine taxable income. Ensure all calculations are precise to avoid discrepancies.

-

Determine Tax Liabilities: Apply the applicable tax rate to the calculated taxable income.

-

Sign and Submit: Review the completed form for accuracy, sign, and either file electronically or mail it to the appropriate IRS address.

Key Elements of Form 1120-RIC

Several elements within Form 1120-RIC are critical for accurate reporting:

- Schedule A: Details the dividends received and paid by the RIC, essential for ensuring proper distribution records.

- Schedule B: Focuses on the fund’s balance sheet, asset-liability overview, and shareholder equity, which is crucial for transparency of financial health.

- Schedule J: Covers the tax computation and tax credits, personalizing tax obligations for the investment entity based on specific circumstances.

- Reconciliation of Income (Schedule M-1): This adjusts differences in reported income between financial and tax records.

IRS Guidelines & Compliance

Adhering to IRS guidelines ensures compliance and reduces audit risks:

- Accurate Reporting: The IRS mandates that all financial figures submitted must align with records and public reports, supporting transparency.

- Timely Filing: RICs must file Form 1120-RIC by the 15th day of the third month after the tax year ends, typically March 15 for calendar-year entities.

- Proper Documentation: Retain all supporting documents for a minimum of three years from filing to provide verification in case of an audit.

Filing Deadlines and Important Dates

Adhering to critical deadlines is essential for compliance:

-

Annual Deadline: The filing date is the 15th day of the third month following the end of the tax year. Extensions can be requested using Form 7004, but any taxes owed must still be paid by the original deadline.

-

Amendments: Should discrepancies or errors be discovered post-filing, amended returns should be submitted as soon as possible to avoid penalties.

Required Documents for Submission

Preparation of Form 1120-RIC involves compiling several key documents:

- Income Statements: Ensure all revenue streams are documented clearly.

- Expense Reports: Supporting documentation for all deductions claimed.

- Distribution Records: Details of dividends or capital gains distributed to shareholders.

- Balance Sheets: Year-end figures that reflect asset and liability standings.

Legal Use of Form 1120-RIC

Understanding the legal framework surrounding Form 1120-RIC is crucial for correctly interpreting and applying its requirements:

- Tax Code Adherence: RICs must adhere to subchapter M of the Internal Revenue Code to maintain favorable tax conditions.

- Shareholder Protections: Accurate filing protects shareholders from unnecessary tax burdens and ensures transparency in dividend distributions.

Software Compatibility

Various tax preparation software can facilitate filing Form 1120-RIC:

- TurboTax and QuickBooks: Both platforms support corporate tax forms and offer guides for proper input of financial data relevant to Form 1120-RIC.

- DocHub Integration: For document management, DocHub assists by providing a robust tool for annotation, sharing, and signing related documentation securely.

This comprehensive coverage ensures users have access to detailed guidance on completing Form 1120-RIC, focusing on practicality and compliance.