Definition and Meaning

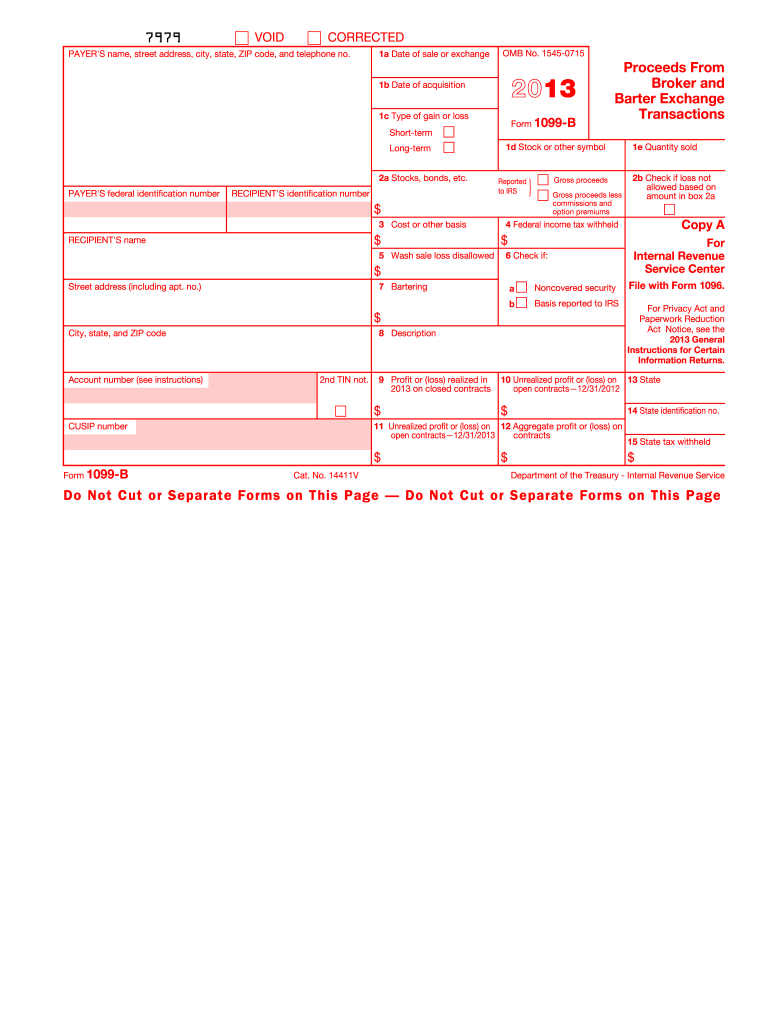

The "Sales and Other Dispositions of Capital Assets - IRS.gov" pertains to the reporting of sales and exchanges of capital assets, typically documented using Form 8949. Capital assets refer to items like stocks, bonds, and real estate, among others, that are held for investment purposes. The form captures details about the transaction, ensuring that any gains or losses are accurately reported for tax purposes. When completing this form, individuals must differentiate between short-term and long-term gains based on the holding period of the asset.

How to Use the Form

To complete the "Sales and Other Dispositions of Capital Assets" form, individuals must gather information about each asset transaction. This involves listing details such as the description of the asset, purchase date, sale date, proceeds from the sale, and the cost basis. Calculations of gain or loss are necessary, factoring in any relevant adjustments. The finalized information should then be transferred to Schedule D which summarizes and calculates the tax implications of capital gains and losses.

How to Obtain the Form

Form 8949, which is used for reporting capital gains and losses, is available on the IRS website. Users can download the form directly from IRS.gov under the "Forms" tab. Alternatively, tax software often provides electronic versions of the form for added convenience, allowing individuals to complete it digitally and submit it as part of their tax return process.

Steps to Complete the Form

- Gather Transaction Details: Collect all receipts, statements, and trade confirmations related to the asset sale.

- Fill in Personal Information: Include your name, Social Security Number, and tax year.

- List Asset Transactions: For each sale:

- Enter the description of the property.

- Record the asset’s purchase and sale dates.

- Fill in the proceeds and the cost basis of the asset.

- Calculate Gain/Loss: Subtract the cost basis from the sale proceeds, noting whether it resulted in a gain or loss.

- Adjustments: Include any wash sale losses disallowed or adjustments for option trades.

- Transfer Totals to Schedule D: Group the sales into short-term and long-term, depending on the duration the asset was held, and summarize the totals on Schedule D.

Who Typically Uses the Form

The form is utilized by anyone who has sold or disposed of capital assets, particularly those engaging in transactions involving stocks, bonds, or real property. It is essential for individual taxpayers filing standard or complex tax returns, including self-employed individuals and other investors. Businesses may also use this form when disposing of assets beyond their standard inventory or product line.

IRS Guidelines for the Form

The IRS provides comprehensive instructions for completing Form 8949, detailing taxpayer obligations regarding the classification and reporting of capital asset sales. Taxpayers must report all transactions, even those resulting in a loss. It’s crucial to follow IRS guidance on adjusting cost basis, computing wash sales, and differentiating between short-term and long-term holdings.

Filing Deadlines and Important Dates

The form must be filed alongside your annual tax return, typically due by April 15. Extensions are available, but they require timely submission requests. Specific deadlines may vary slightly based on weekends or federal holidays, so checking the IRS website for exact yearly deadlines is advisable.

Penalties for Non-Compliance

Failing to file or inaccurately completing the "Sales and Other Dispositions of Capital Assets" form can result in penalties from the IRS, including fines and accruing interest. More severe cases of misreporting, such as deliberate falsification, might lead to audits or criminal charges under tax fraud statutes.

Key Elements of the Form

The form is divided into two main parts for reporting short-term and long-term transactions. Critical sections include:

- Description of Property: Identification details for each asset.

- Dates Acquired and Sold: To determine the holding period.

- Proceeds and Cost Basis: Financial figures necessary for calculating gain or loss.

- Adjustments: Specific adjustments as per IRS rules, like code-based notations for wash sales.

Examples of Using the Form

Consider an investor who buys shares in a tech company in January and sells them the following December. Given the under-one-year holding, these transactions are documented as short-term. Alternatively, if an investor sells a rental property held for five years, this transaction is captured under long-term sales, impacting the tax rate applied.

Important Terms Related to the Form

- Capital Asset: Item held for investment, such as securities or real estate.

- Cost Basis: The original value or purchase price of an asset.

- Short-Term/Long-Term Gains: Distinctions based on the holding period, affecting tax rates.

- Wash Sale: An IRS rule disallowing a loss deduction if a similar asset is repurchased within 30 days.