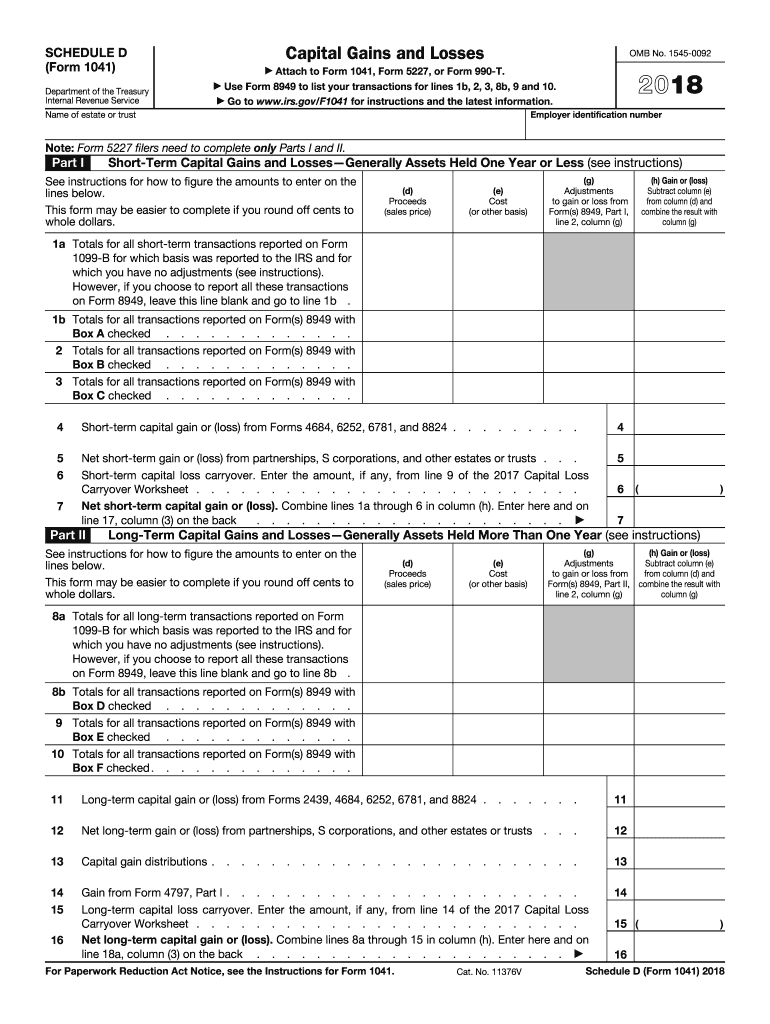

Definition & Context of IRS Schedule D (Form 1041) 2014

The IRS Schedule D (Form 1041) for 2014 is a supplemental tax form used by estates and trusts to report capital gains and losses from the sale or exchange of assets. This form is integral to accurately determining the tax liability associated with these transactions. It organizes data into sections covering short-term and long-term capital gains and losses, ultimately culminating in the net capital gain or loss for the fiscal year. Accurately completing Schedule D is crucial for ensuring compliance with tax regulations and optimizing tax outcomes for estates and trusts.

Short-Term vs. Long-Term Capital Transactions

- Short-Term Capital Transactions: Assets held for one year or less. Gains or losses from these transactions are generally taxed at ordinary income tax rates.

- Long-Term Capital Transactions: Assets held for more than one year. They are subject to preferential tax rates, which may be lower than those for short-term gains.

Understanding these categories and accurately segregating transactions into short-term and long-term on Schedule D is essential for accurate tax reporting and computation.

How to Use the IRS Schedule D Form

Using the IRS Schedule D Form 1041 involves a detailed process of entering data about capital transactions. This 2014 version specifically requires that you:

- Identify Asset Types: Record information about each asset sold, including stocks, bonds, or properties.

- Calculate Gains or Losses: Document the sale price against the original purchase price to ascertain whether each transaction resulted in a gain or a loss.

- Adjust for Expenses: Include any relevant expenses that can adjust the basis and affect the resulting gain or loss.

This meticulous approach ensures all capital transactions are captured and reported accurately, impacting the overall financial obligations of the estate or trust.

Step-by-Step Form Completion

- Gather Financial Documents: Collect all essential documents that detail purchase and sale transactions, such as stock sale receipts, settlement statements, or financial ledgers.

- Enter Transaction Data: Fill in the sale and purchase information on the form's applicable lines, ensuring each entry's accuracy.

- Summarize Net Gains and Losses: Calculate and enter the total short-term and long-term gains or losses, allowing for precise tax computations.

How to Obtain the IRS Schedule D Form

Obtaining the IRS Schedule D Form 1041 for 2014 can be done through several methods:

- IRS Website: Access the form by visiting the official IRS website, where downloadable versions of forms from previous years are available.

- Tax Software: Many tax preparation software programs, such as TurboTax or QuickBooks, offer integrated solutions that include the necessary forms for completing tax filings for estates and trusts.

- Tax Professionals: Utilize the services of a certified tax professional who can provide the form as part of their suite of tax preparation services.

Steps to Complete IRS Schedule D Form Fillable

Completing the IRS Schedule D Form 1041 comprises several steps:

- Download and Open the Form: Access the fillable PDF version of the form to enable direct input of data electronically.

- Enter Basic Information: Fill out the estate or trust's name, employer identification number (EIN), and other identifying information.

- Report Short-Term Gains/Losses: Accurately complete sections related to short-term transactions, detailing dates of acquisition and disposition, and compute the respective gains or losses.

- Report Long-Term Gains/Losses: Similarly, fill out the long-term section, following identical processes for long-held investments.

- Review Adjustments and Deductions: Note any applicable adjustments or deductions that may impact the taxable amount.

Completing these steps accurately will ensure the form reflects the true capital gains or losses, aligning with the estate or trust's financial reality.

Key Elements of IRS Schedule D Form

Several key elements define the structure and function of the IRS Schedule D Form 1041 for 2014:

- Capital Asset Descriptions: Detailed reporting of each transaction involving securities, real estate, or other capital assets.

- Proceeds from Sales: Accurate representation of gross proceeds from each sale or exchange of assets.

- Acquisition and Sale Dates: Clear documentation of the dates associated with both the acquisition and disposal of assets to determine holding periods.

- Cost or Other Basis: Original purchase price or adjusted basis of each asset, essential for calculating gains or losses.

IRS Guidelines on Schedule D Form 1041

The IRS provides specific guidelines on completing the Schedule D Form 1041:

- Proper Documentation: Ensure thorough record-keeping for all transactions entered on the form, which can include purchase invoices, sales receipts, and adjusted basis documentation.

- Accurate Categorization: Differentiate correctly between short-term and long-term holdings based on the holding period, as it significantly affects tax computation.

- Compliance with Filing Requirements: Follow specific IRS instructions for line-by-line completion of the form to ensure compliance and readiness in case of an audit.

Required Documents for Schedule D Form 1041 Filing

Supporting documents to complete the Schedule D Form 1041 include:

- Transaction Ledgers: Detailed logs of purchase and sales transactions.

- Property Acquisition Receipts: Documents affirming the ownership and cost basis of sold assets.

- Brokerage Statements: Financial statements from brokers detailing security transactions.

Gather these records to facilitate the accurate and efficient completion of the form, ensuring all reported data is verifiable.

Penalties for Non-Compliance

Failure to correctly complete and file the IRS Schedule D Form 1041 can lead to several penalties and repercussions:

- Fines and Interest: Incorrectly filed or late forms may result in financial penalties, including fines and accruing interest on unpaid taxes.

- Possible Audits: Inaccuracies or omissions on the form increase the risk of IRS audits, which can further delay estate or trust settlements.

- Legal Consequences: In severe cases, intentional misreporting may lead to legal actions or the revocation of responsible fiduciary licenses.

Understanding the penalties underscores the importance of compliance and accuracy in reporting capital gains and losses.