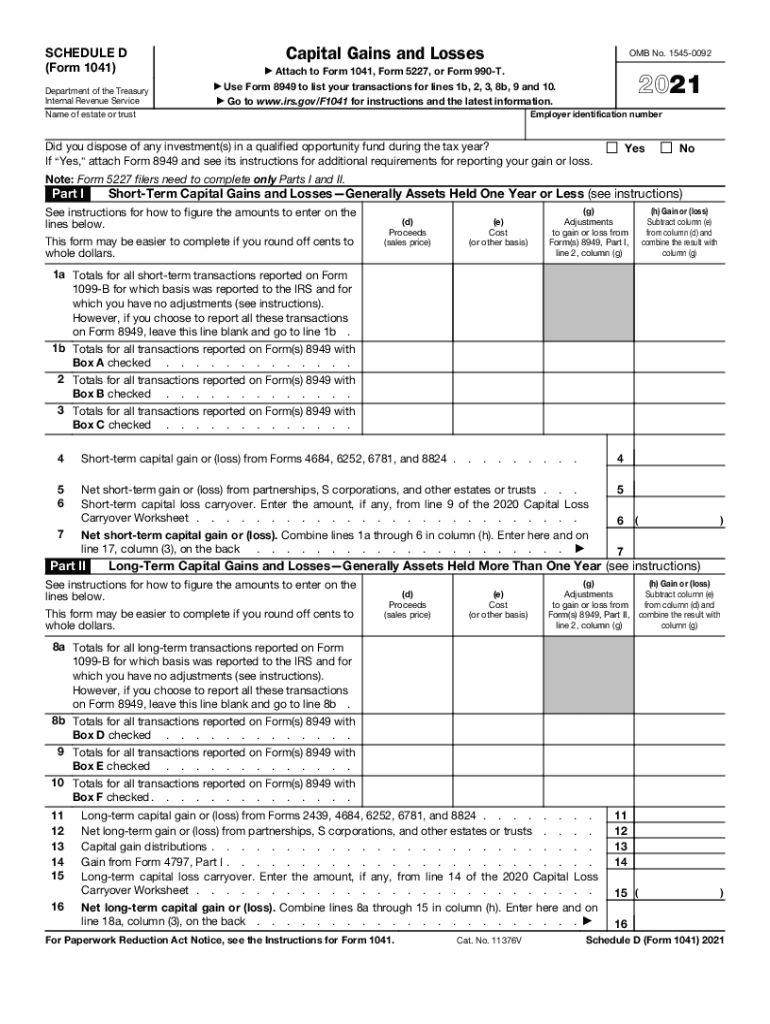

Definition and Meaning of IRS Schedule D

IRS Schedule D is a tax form used to report capital gains and losses from various investment transactions such as stocks, bonds, and property sales. The form is essential for individuals and entities filing Form 1040, Form 1040-SR, or Form 1041, providing a detailed summary of all capital asset sales or exchanges that occurred over the tax year. It breaks down transactions into short-term and long-term gains, helps in calculating the total net capital gain or loss, and determines taxable amounts subject to federal income tax. Proper completion of Schedule D ensures compliance with IRS regulations and allows taxpayers to report financial activities accurately.

- Short-term Gains/Losses: Assets held for one year or less.

- Long-term Gains/Losses: Assets held for more than one year.

- Tax Rates: Vary depending on asset type and holding period.

How to Use IRS Schedule D

Using IRS Schedule D involves systematically recording each capital transaction throughout the year, including the dates of acquisition and sale, the amount realized from the sale, and the cost or other basis of the asset. Taxpayers must categorize each transaction as either short-term or long-term to apply the appropriate tax treatments.

- Gather Documents: Collect brokerage statements, sale receipts, and relevant documents detailing investment transactions.

- Categorize Transactions: Identify each transaction as short-term or long-term based on holding periods.

- Calculate Totals: Sum up gains and losses separately for short-term and long-term transactions.

- Complete the Form: Enter the detailed transaction data and calculation results in the specified sections of Schedule D.

Steps to Complete IRS Schedule D

Completing IRS Schedule D requires precision and an understanding of tax rules for capital gains and losses. Here's a simplified step-by-step guide:

- Identify Transactions: List all your capital asset transactions, noting the sale dates and purchase prices.

- Determine Gains/Losses: Calculate the difference between the sales price and purchase price for each asset.

- Categorize: Separate transactions into short-term and long-term categories.

- Input Data: Fill in the respective sections for both short-term and long-term gains and losses on Schedule D.

- Calculate Net Gains/Losses: Use Schedule D to determine total capital gain or loss by subtracting losses from gains.

- Transfer Totals: Carry the calculated amounts to the designated lines on your main tax form (e.g., Form 1040).

Examples of Using IRS Schedule D

Various scenarios illustrate the use of IRS Schedule D, offering practical insights into handling the form:

- Stock Sales: An investor sells shares of a corporation after holding them for more than one year, classifying it as a long-term capital gain.

- Real Estate: A homeowner sells a rental property after three years, reporting the transaction as a long-term gain due to the extended holding period.

- Cryptocurrency Transactions: A taxpayer sells cryptocurrency held for less than a year, requiring classification as a short-term gain or loss.

Key Elements of IRS Schedule D

Schedule D requires comprehensive data entry and includes several critical components:

- Transaction Dates: Dates of acquisition and disposal.

- Cost Basis: Original purchase price or adjusted cost.

- Proceeds: Amount of money received from the sale of assets.

- Net Gain or Loss: Calculated result from individual asset sales.

IRS Guidelines on Schedule D

The IRS provides specific guidelines for accurately completing Schedule D, which include:

- Form 8949: In cases where adjustments are needed, taxpayers may need to include Form 8949 to detail each transaction's basis adjustment.

- Wash Sales: Rules disallow losses from wash sales where stocks were repurchased within 30 days.

- Loss Limitation: The IRS restricts the deduction of net capital losses to $3,000 per year for individuals, with the remaining balanced carried forward.

Filing Deadlines and Important Dates

Timely submission of IRS Schedule D is crucial to avoid penalties. Typically, the form is due with the taxpayer's annual tax return:

- Deadline for Individuals: Generally, April 15 of the subsequent year.

- Extensions: Taxpayers can file Form 4868 to request an extension, potentially extending the deadline to October 15.

Penalties for Non-Compliance

Failing to submit IRS Schedule D accurately or on time may lead to penalties, including:

- Filing Penalties: Charges for late submission of tax returns.

- Accuracy-related Penalties: Fines for substantial understatement or misreporting of tax liabilities.

- Interest Charges: Accrued interest on unpaid taxes or underreported amounts.