Definition & Meaning

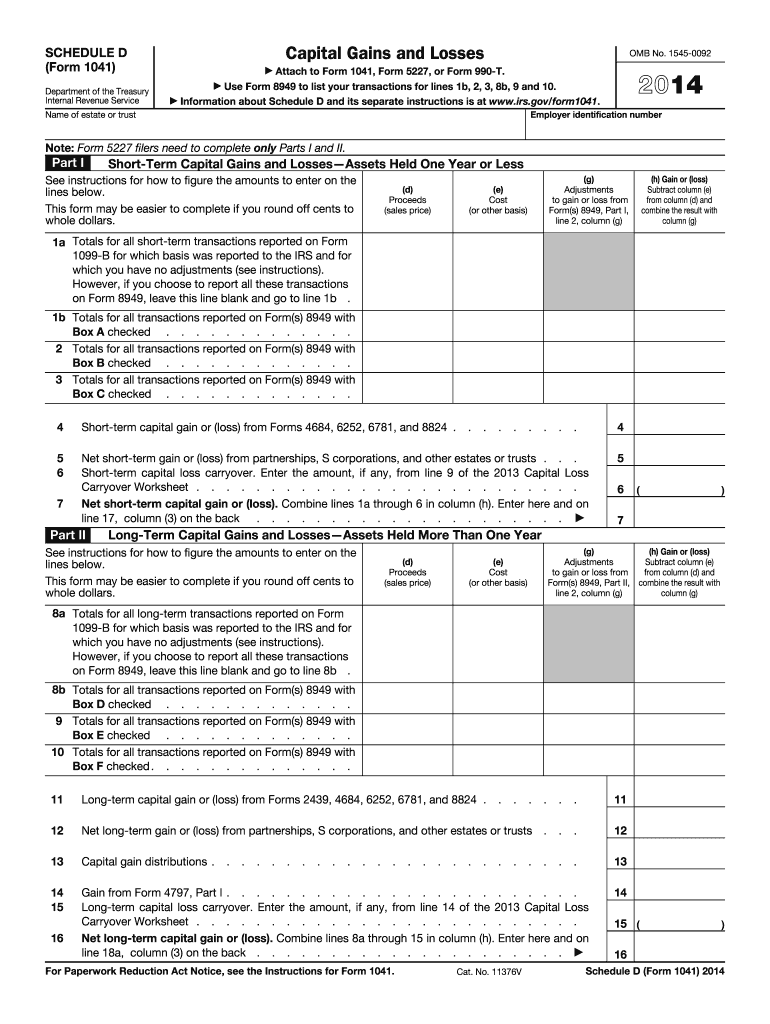

Schedule D (Form 1041) is used by estates and trusts to report capital gains and losses from asset sales throughout the tax year. This form includes sections for detailing short-term and long-term capital transactions, providing the necessary framework to calculate gains or losses. The form also includes guidance on how to report net gains or losses accurately, ensuring the correct computation of taxable income.

Important Terms Related to Schedule D (Form 1041)

Understanding specific terminology is crucial for correctly filling out Schedule D (Form 1041). Key terms include:

- Capital Gains: Profits from selling an asset or investment.

- Capital Losses: Financial loss from the sale of an asset below its purchase price.

- Short-Term: Refers to assets held for one year or less.

- Long-Term: Refers to assets held for more than one year.

- Proceed: The amount received from selling an asset.

- Adjusted Basis: The asset's original cost, plus improvements and minus deductions such as depreciation.

How to Use the Instructions for Schedule D (Form 1041)

The instructions provide a comprehensive guide for accurately completing Schedule D (Form 1041). They include detailed explanations of each form section, assist in understanding the necessary calculations, and give examples for clarity. The guidance includes interpreting various elements, such as distinguishing between short-term and long-term transactions, and calculating gains or losses.

Steps to Complete Schedule D (Form 1041)

-

Collect Necessary Documents: Gather all documents related to the transactions you need to report.

-

Identify Transaction Types: Differentiate between short-term and long-term transactions to report them correctly.

-

Calculate Capital Gains or Losses: Determine the gain or loss for each transaction based on sale price and adjusted basis.

-

Complete the Form: Enter calculated figures into the appropriate sections of Schedule D.

-

Review Instructions for Guidance: Use the provided instructions for any complex computations or specific questions.

Key Elements of Schedule D (Form 1041)

Sections for Reporting

-

Short-Term Capital Transactions: This section includes sales of assets held for one year or less. Each transaction must list proceeds, costs, and gains or losses.

-

Long-Term Capital Transactions: Includes assets held for more than one year, reported similarly to short-term assets but under different tax rate considerations.

Calculating Gains and Losses

The instructions provide methodologies for accurately computing the gain or loss and include formulas for adjustments to basis and other figures to ensure precise reporting.

IRS Guidelines for Schedule D (Form 1041)

The IRS outlines specific requirements and guidelines when reporting capital gains and losses via Schedule D (Form 1041). These include detailed definitions of qualifying transactions, instructions for using additional forms if thresholds are exceeded, and explanations of the limits on capital losses, especially for trusts and estates.

Filing Deadlines and Important Dates

The filing deadline for Schedule D (Form 1041) typically coincides with the deadline for Form 1041, which is April 15 for calendar-year filers. Extensions may be requested through IRS Form 7004, allowing additional time, but not extending the time to pay any taxes due.

Penalties for Non-Compliance

Failing to accurately report capital gains and losses using Schedule D (Form 1041) may result in penalties, interest on unpaid taxes, and further scrutiny by the IRS. Compliance with the instructions ensures accurate filings and minimizes the risk of penalties. Possible penalties include late filing and late payment fees, emphasizing the importance of meeting deadlines and providing accurate information.

Form Submission Methods

-

Online: Through authorized e-filing systems, ensuring quick and efficient submission.

-

Mail: Sending printed forms to designated IRS addresses, which may vary by state.

-

In-Person: Direct submission at IRS offices, though less common with available online methods.

This flexibility allows filers to choose the most convenient method based on their circumstances and preferences.