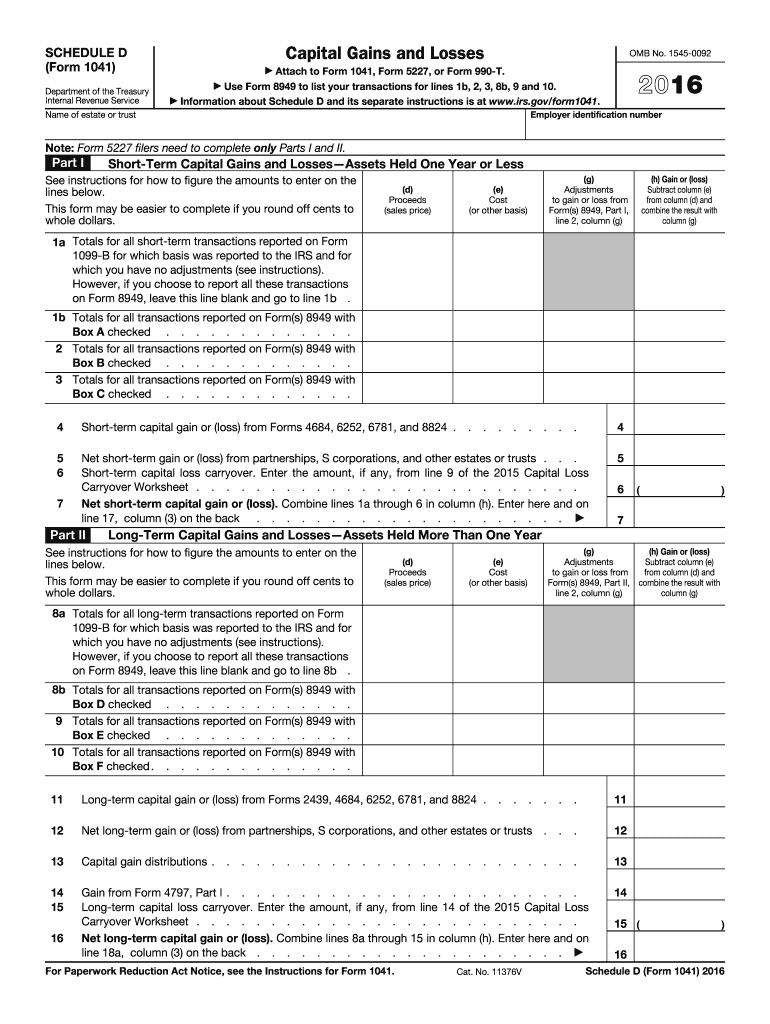

Definition & Meaning

IRS Form Capital 2016, officially known as Schedule D (Form 1041), is utilized by estates and trusts in the United States to report capital gains and losses for the tax year 2016. This form provides a detailed breakdown of capital transactions, both short-term and long-term, and aids in calculating the net impact of these transactions for tax purposes. Filers must include data on the sales proceeds, cost, and any necessary adjustments, providing a comprehensive view of gains or losses.

How to Use the IRS Form Capital 2016

Using IRS Form Capital 2016 involves a series of steps to properly document capital gains or losses. Users must:

- Gather Financial Records: Compile documentation on all asset transactions, including purchase and sale receipts.

- Classify the Transactions: Distinguish between short-term and long-term transactions based on asset holding periods.

- Complete the Form: Utilize the specified sections of Schedule D to enter detailed information on each transaction.

- Verify Information: Double-check all calculations and ensure compliance with IRS guidelines.

- Attach to Return: Attach the completed form to the main tax return form for estates or trusts.

How to Obtain the IRS Form Capital 2016

Estates and trusts can obtain the IRS Form Capital 2016 through various methods:

- Official IRS Website: The form is downloadable directly from the IRS website in PDF format.

- Local IRS Office: Request a copy in person at an IRS office.

- Tax Software: Accessible through authorized tax preparation software that supports form 1041.

Steps to Complete the IRS Form Capital 2016

Completing the form requires careful attention to detail:

- Input Basic Information: Include estate or trust name and tax identification number.

- Report Short-Term Gains or Losses: Fill in Part I with details of short-term transactions.

- Report Long-Term Gains or Losses: Enter information in Part II for long-term transactions.

- Calculate Totals: Use Part III to summarize and derive total gains or losses.

- Review Accuracy: Ensure all calculations align with financial data.

- Submit with Tax Return: Attach the form to the estate or trust's tax return and file by the appropriate deadline.

Key Elements of the IRS Form Capital 2016

The form consists of multiple critical parts:

- Part I: Short-term capital gains and losses section.

- Part II: Long-term capital gains and losses section.

- Part III: Summary of net gains or losses, used to report on tax returns.

- Additional Fields: For adjustments, exemptions, and other specific concerns based on circumstances.

IRS Guidelines

The IRS provides specific guidelines for Schedule D (Form 1041), ensuring users accurately report capital gains and losses:

- Documentation: Retain proof of each transaction for at least three years.

- Accuracy: Double-check numbers to prevent errors in reporting.

- Compliance: Ensure all data follows IRS definitions and rules for qualifying transactions.

Filing Deadlines / Important Dates

For the tax year 2016, the filing deadline for estates and trusts utilizing Schedule D was generally mid-April 2017, with extensions available under specific conditions:

- Standard Deadline: April 17, 2017, due to adjustments.

- Extended Deadline: October 16, 2017, if an extension was filed.

Required Documents

To accurately complete the form, several documents are necessary:

- Transaction Records: Sales receipts, contracts, settlement documents.

- Cost Basis Records: Proof of original purchase value.

- Adjustments Proof: Documentation of any adjustments.

Examples of Using the IRS Form Capital 2016

Real-world examples can clarify the use:

- Estate Liquidation: Reporting gain from the sale of estate-held investment properties.

- Trust Management: Tracking both short- and long-term gains from diversified portfolio sales.

- Charitable Remainder Trusts: Documenting capital gains from asset disposition before distribution to beneficiaries.

Form Submission Methods

Submit completed forms using one of the following methods:

- Online: Through e-filing services compatible with IRS systems.

- Mail: Physical submission through certified mailing.

- In-Person: Directly at a local IRS office, ensuring receipt confirmation.