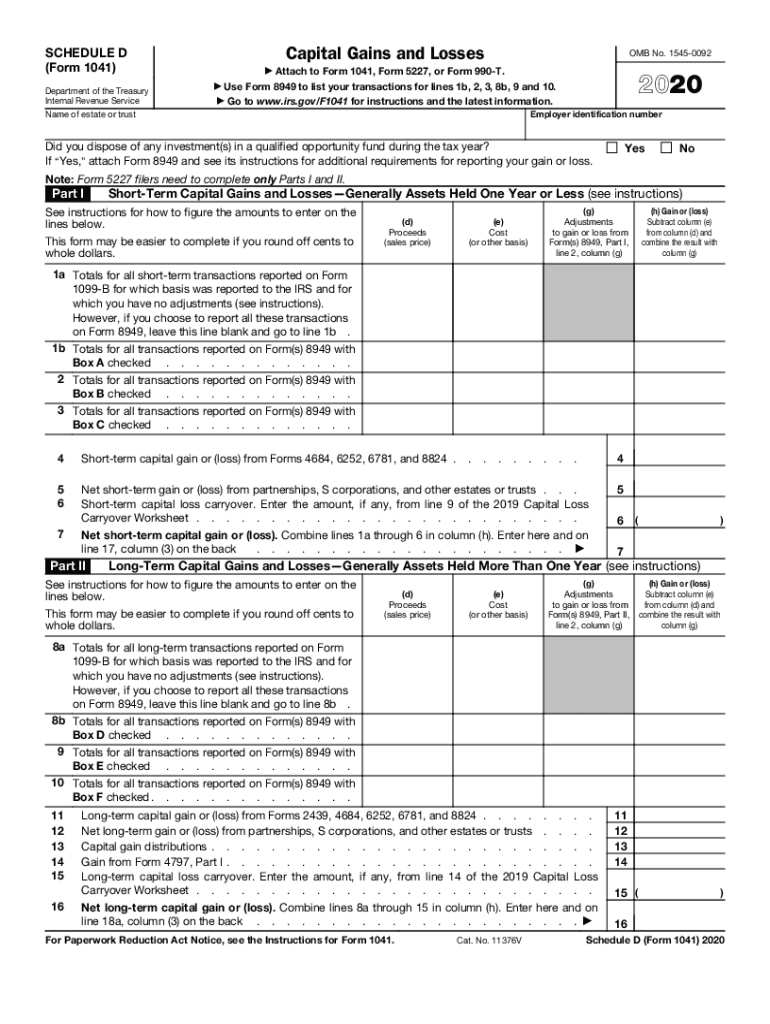

Definition and Purpose of IRS Schedule D

IRS Schedule D is a tax form used by taxpayers in the United States to report capital gains and losses from investments. This includes transactions involving stocks, bonds, capital assets, and other similar financial instruments. The primary purpose of Schedule D is to help individuals and entities accurately calculate their taxable income by accounting for any profits or losses incurred through these investments during the tax year.

Schedule D separates these capital transactions into short-term and long-term categories. Short-term refers to assets held for one year or less, while long-term pertains to those held for more than one year. This differentiation is crucial as it affects the tax rates applied to the gains. Understanding the role of Schedule D is essential for anyone engaged in buying or selling investments, as it directly impacts their tax liability.

How to Use IRS Schedule D

Using IRS Schedule D involves several steps to accurately report capital gains and losses. The form requires detailed information about each transaction, including the dates of acquisition and sale, the cost basis, and the proceeds from the sale.

- Gather Required Information: Collect statements and records of all transactions involving the sale or exchange of capital assets.

- Categorize Transactions: Separate your transactions into short-term and long-term categories based on the duration the assets were held.

- Calculate Gains and Losses: For each transaction, calculate the gain or loss, considering the sale proceeds and the cost basis. This determines the increase or decrease in asset value.

- Complete Form Sections: Input the results into the appropriate sections on Schedule D. The form provides guidance on calculating your net gains or losses.

- Transfer Results: Transfer the totals from Schedule D to the relevant line on Form 1040 or other applicable tax returns to reflect these figures in your overall taxable income.

Steps to Complete IRS Schedule D

Completing IRS Schedule D involves a systematic approach to ensure accuracy and compliance:

- Record Short-Term Transactions: Begin by listing all short-term transactions, including sale dates, cost basis, and proceeds.

- Calculate Short-Term Totals: Sum the gains and losses from short-term transactions to get a net short-term gain or loss.

- Record Long-Term Transactions: Document all long-term transactions with equivalent details.

- Calculate Long-Term Totals: Sum these to obtain a net long-term gain or loss.

- Determine Overall Gain or Loss: Combine short-term and long-term results for an overall figure.

- Input Final Figures: Enter the final numbers on the appropriate IRS forms, ensuring alignment with any additional schedules or worksheets.

Who Typically Uses IRS Schedule D

Individual taxpayers who buy and sell investments, such as stocks or bonds, commonly use Schedule D. It is also applicable to estates and trusts, as well as various entities like corporations and partnerships that engage in similar transactions.

Investors and day traders often rely on Schedule D to report frequent securities trading. Similarly, businesses involved in buying and selling significant capital assets are required to use this form for accurate tax reporting. Understanding which taxpayers must file Schedule D can help ensure compliance with IRS regulations.

Important Terms Related to IRS Schedule D

Several key terms are integral to understanding IRS Schedule D:

- Capital Asset: Any property or investment held by a taxpayer that is not inventory, accounts receivable, or depreciable property used in a business.

- Cost Basis: The original value of an asset, adjusted for various factors such as improvements or dividends, used to determine gain or loss on a sale.

- Proceeds: The amount received from selling an asset before subtracting the cost basis or any fees.

- Short-Term Gain/Loss: Gains or losses on assets held for one year or less.

- Long-Term Gain/Loss: Gains or losses on assets held for more than one year. These are generally taxed at a lower rate than short-term gains.

Filing Deadlines and Important Dates

Schedule D follows the general tax filing calendar set by the IRS. The standard deadline for submitting Schedule D along with Form 1040 is April 15th of the following year. If this date falls on a weekend or holiday, the deadline may be extended to the next business day. Taxpayers should ensure all information is compiled and accurate before this date to avoid penalties.

Extensions can be requested using Form 4868, which gives additional time to file but not to pay any taxes due. Awareness of these key dates helps prevent late filing penalties and interest on unpaid taxes.

Required Documents for Completing IRS Schedule D

To complete IRS Schedule D accurately, you will need access to several documents:

- Brokerage Statements: Provide detailed records of transactions, including dates and amounts.

- 1099-B Forms: Issued by brokers, detailing the proceeds from buys and sells.

- Receipts and Invoices: Relevant for assets that are not typically reported by brokers, such as personal property sales.

- Prior Year Forms: Helpful for calculating carryover losses and tracking investments over multiple years.

Keeping these documents organized ensures that all necessary information is available when preparing your taxes.

Penalties for Non-Compliance with IRS Schedule D

Failure to accurately file Schedule D can lead to various penalties. The IRS may impose fines for underreporting income or making false statements on tax forms. Additionally, failing to file altogether can result in a failure-to-file penalty, which accumulates monthly until the return is submitted.

In severe cases, intentional misreporting can lead to additional scrutiny or audits by the IRS. To avoid these repercussions, ensure that Schedule D is filled out comprehensively and submitted on time.