Definition & Meaning

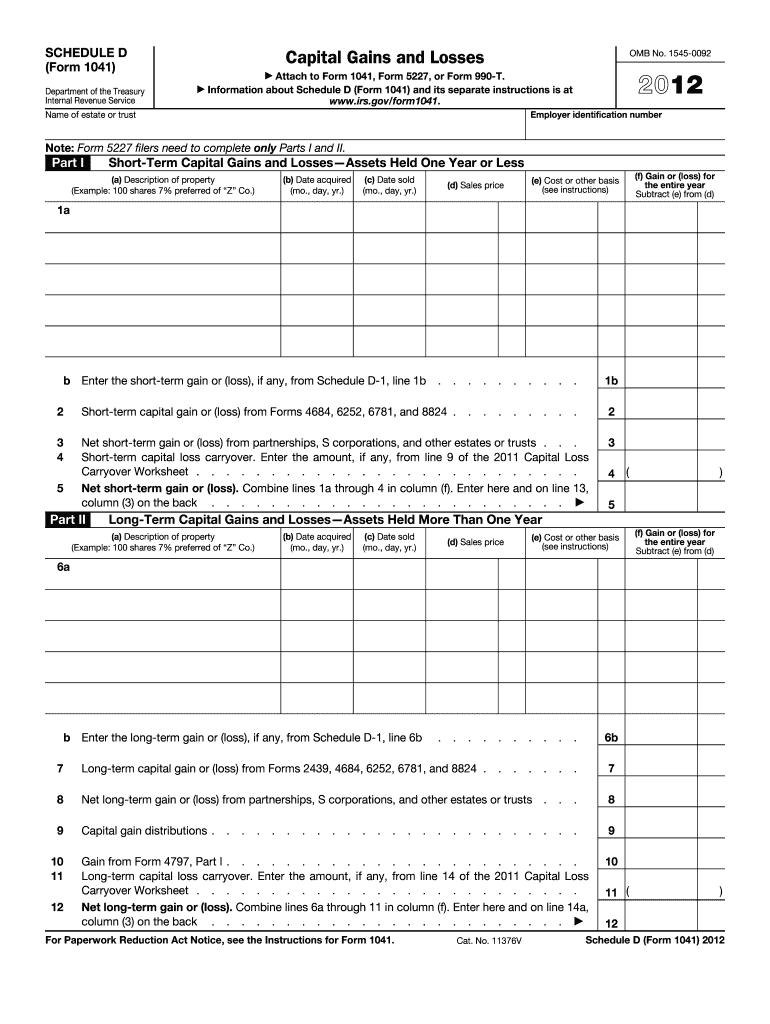

The 2012 Schedule D (Form 1041) serves as a critical tax document used specifically by estates and trusts to report capital gains and losses incurred during the tax year. It involves detailing transactions related to capital assets, such as securities, which were held, bought, or sold by the estate or trust. The form meticulously captures short-term and long-term capital gains, providing a framework to calculate the net capital gains or losses impacting the overall tax liability. A precise understanding of this document is essential for ensuring accurate tax calculations, and it plays a vital role in transparent reporting of financial activities pertaining to an estate or trust.

How to Use the 2 Schedule D Form

To utilize the 2012 Schedule D effectively, begin by organizing all records of financial transactions that involved the sale or exchange of capital assets. The form requires meticulous input of details like the description of the asset, acquisition date, sale date, purchase price, and selling price. These inputs are categorized into short-term and long-term sections, which assist in computing relevant gains or losses. After gathering the necessary information, carefully follow the IRS guidelines to fill out each part of the form, ensuring the correct reporting of the estate or trust's capital income. This systematic approach guarantees compliance with tax obligations and aids in the accurate computation of potential liabilities or refunds.

Steps to Complete the 2 Schedule D Form

-

Prepare Documentation: Collect all necessary documentation related to capital transactions, including purchase and sale invoices, brokerage statements, and any relevant financial records.

-

Enter Short-Term Gains and Losses: In the designated section of Schedule D, enter details for each short-term transaction. This includes the asset description, purchase and sale dates, and transaction values.

-

Detail Long-Term Transactions: Following short-term entries, provide information on transactions held for more than one year. Utilizing separate lines for each transaction prevents errors and ensures clarity.

-

Calculate Totals: Summarize short-term and long-term capital gains and losses separately. Ensure arithmetic accuracy to avoid discrepancies in subsequent taxation calculations.

-

Net Gains or Losses: Use the form's instructions to calculate the net gains or losses. This step is essential for figuring out the estate’s taxable capital income.

-

Attach to Form 1041: Once completed, attach Schedule D to Form 1041. This consolidation provides the IRS with a comprehensive view of the estate’s or trust’s tax obligations.

Why Should You Use the 2 Schedule D Form

Utilizing the 2012 Schedule D form is crucial for accurately reporting the estate's or trust's capital financial activities. The form not only ensures compliance with tax regulations but also aids in optimizing tax outcomes by distinguishing between short- and long-term gains and losses, which are often taxed differently. Moreover, it supports transparency and accountability in financial disclosures, providing an accurate reflection of the estate’s fiscal health. This precision aids estate executors or trustees in fulfilling fiduciary duties and mitigating potential penalties due to underreporting or errors.

Key Elements of the 2 Schedule D Form

-

Structured Sections: Distinct sections for short-term and long-term gains or losses enable detailed reporting based on asset holding periods.

-

Transaction Details: Requirements for detailed transaction inputs, including acquisition and disposition dates, assist in traceable record-keeping.

-

Summarized Totals: Summation spaces for gains and losses facilitate straightforward, error-free computation.

-

Netting Calculations: Clear instructions for calculating net capital gains or losses help ensure adherence to correct accounting principles.

IRS Guidelines

The Internal Revenue Service provides specific instructions to assist taxpayers in filling out the 2012 Schedule D. These guidelines outline the criteria for reporting, calculation methods for gains or losses, and strategies for tax computations under maximum capital gains tax rates. Additionally, they offer clarification on the handling of wash sales and like-kind exchanges, which can impact the accurate representation of an estate’s financial activities. Adherence to these guidelines is paramount to maintaining compliance with federal tax laws.

Filing Deadlines / Important Dates

The filing deadline for estates and trusts using the 2012 Schedule D aligns with the general deadline for Form 1041, typically April 15 of the following year, unless that date falls on a weekend or holiday. Extensions are available through Form 7004, providing additional time to gather accurate information without incurring penalties. Awareness of these crucial deadlines is necessary to prevent late filing fees or compounding interest on unpaid taxes, ensuring a smooth tax reporting process.

Required Documents

To accurately complete the 2012 Schedule D, maintain comprehensive records, such as:

- Transaction Records: Detailed records of all buy-sell activities, including receipts and contracts.

- Brokerage Statements: Monthly or yearly statements from brokerage firms that detail all transactions related to capital assets.

- Cost Basis Documentation: Evidence or calculations supporting the cost basis of assets, which is essential for accurate gain or loss reporting.

Ensuring thorough documentation streamlines the completion process and aids in swiftly addressing any IRS inquiries that may arise.