Definition & Meaning

Schedule D (Form 1041) is a crucial document used by estates and trusts to report their capital gains and losses. Estates and trusts use this form to detail transactions involving the sale or exchange of capital assets, which can include stocks, bonds, and real estate. The form separates transactions into short-term and long-term categories, reflecting different holding periods and tax rates.

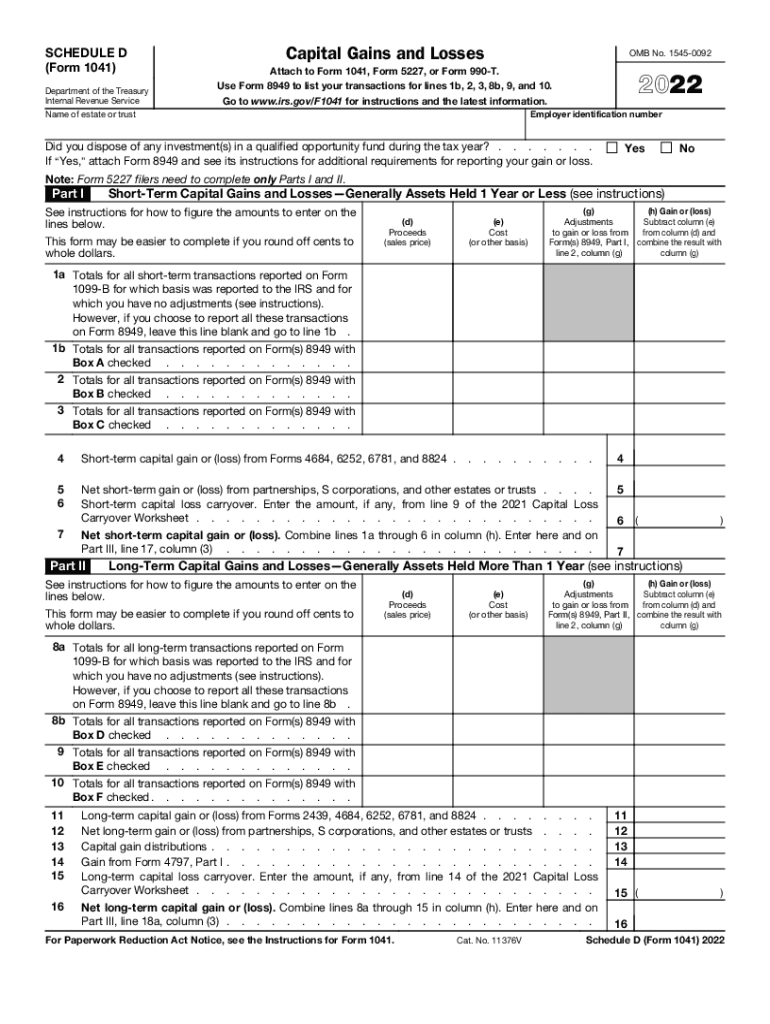

Key Sections of Schedule D

- Capital Gains and Losses: It breaks down into sections that handle short-term (assets held for one year or less) and long-term (assets held for more than one year) transactions, reflecting different tax treatments.

- Net Gains Calculation: Requires summing gains and losses, applying rates, and understanding potential impacts on overall tax liabilities.

Understanding these elements is essential for accurately reflecting the tax implications of an estate or trust's investment activities.

How to Use the Additional Items Related to Schedule D

To correctly fill out the Additional Items Related to Schedule D, one must:

- Identify Transactions: Gather a complete list of all capital asset transactions, noting dates of acquisition and sale to classify them as short-term or long-term.

- Document Proceeds and Costs: Accurately report the proceeds from each sale or exchange and the original cost or adjusted basis to determine gain or loss.

- Calculate Adjustments: Make necessary adjustments for items such as transfer costs or depreciation, closely following IRS instructions.

Being meticulous in each step prevents discrepancies and ensures compliance with IRS requirements.

Steps to Complete the Additional Items Related to Schedule D

Proper completion involves:

- Collate Necessary Information: Ensure all documents related to the assets’ acquisition and disposal are on hand, including invoices and broker statements.

- Organize by Transaction Type: Segregate based on short-term versus long-term to assist in applying the correct tax rate.

- Fill Out Schedule D: Accurately input details from collected documents, following IRS instructions for each section.

- Attach Additional Forms if Necessary: Forms such as 8949 may be required for detailed reporting of transactions.

Meticulous adherence to these steps ensures the form is completed accurately, avoiding processing delays.

IRS Guidelines

The IRS provides detailed guidance on completing Schedule D, which highlights:

- Transaction Reporting: Specific instructions for reporting different types of capital transactions, emphasizing accuracy and completeness.

- Form Attachments: Guidelines on when to attach additional forms like Form 8949 for detailed transaction listings.

- Tax Calculations: Procedures for applying favorable tax rates to long-term gains, requiring accurate classification.

Refer to the IRS instructions booklet for Schedule D to ensure compliance with all federal requirements.

Filing Deadlines / Important Dates

For estates and trusts using Schedule D (Form 1041), the critical filing deadline is typically:

- April 15: This is the standard deadline unless an extension is granted. Extensions generally extend the deadline to October 15.

- Fiscal Year End Considerations: For entities operating on a fiscal year, the due date is the 15th day of the fourth month following the close of their fiscal year.

Mark these dates carefully to avoid penalties for late filing.

Required Documents

Compiling the Additional Items Related to Schedule D requires:

- Brokerage Statements: Detailed lists of transactions from brokers.

- Receipt and Sale Invoices: Document purchase and sale dates along with prices.

- Cost Basis Documentation: Proof of the purchase price and any improvements or depreciation.

Proper documentation facilitates smooth and accurate completion.

Penalties for Non-Compliance

Failing to comply with IRS requirements can lead to:

- Fines & Interest: Costly fines and accruing interest on late payments or filings.

- Audit Risks: Increased likelihood of audits, necessitating meticulous record-keeping.

- Legal Repercussions: Potential legal consequences or tax court proceedings for fraudulent reporting.

Maintaining compliance is critical to avoid such negative outcomes.

Eligibility Criteria

Eligibility for filing Schedule D (Form 1041) includes any estate or trust with:

- Capital Transactions: Involvement in capital transactions that result in gains or losses.

- Investment Assets: Ownership of investments requiring tax reporting per IRS standards.

Understanding these criteria ensures proper adherence to IRS filing requirements.