Definition and Purpose of the 2012 Form 1041

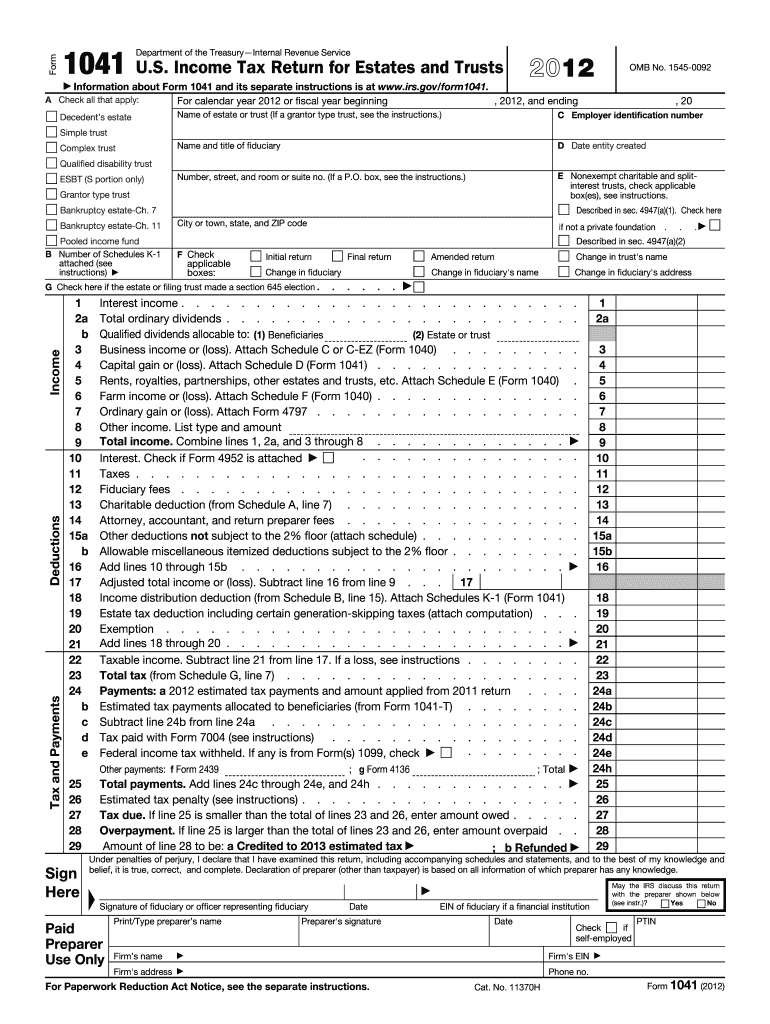

The 2012 IRS Form 1041, known as the U.S. Income Tax Return for Estates and Trusts, is essential for fiduciaries responsible for settling and managing the financial activities of estates and trusts. The form captures income, deductions, and tax liabilities specific to these entities, helping ensure accurate tax reporting and compliance with federal requirements. Estates and trusts use this form to report earnings from dividends, interests, and other income sources, as well as to declare applicable deductions. The form's design guides fiduciaries through the calculation of taxable income and tax owed, playing a key role in the tax reporting duties of estates and trusts.

Steps to Complete the 2012 Form 1041

-

Identify the Estate or Trust:

- Gather basic information, including the name, address, and identification number of the estate or trust.

- Identify the fiduciary managing the entity and any associated identification numbers.

-

Report Income:

- List all income types, such as rental income, dividends, and interest, relevant to the estate or trust.

- Record any capital gains or losses, ensuring proper classification according to IRS guidelines.

-

Account for Deductions:

- Outline expenses related to the administration of the estate or trust, including necessary legal or administrative fees.

- Capture any applicable charitable contributions and input them into the appropriate sections.

-

Calculate Taxable Income:

- Subtract allowable deductions from the total income to determine the taxable income.

- Utilize IRS tax tables or guidance to compute any taxes due based on the taxable income.

-

Complete Additional Schedules:

- If necessary, attach schedules for charitable deductions or income distribution deductions. Ensure accuracy in reporting to avoid discrepancies.

Key Elements of the 2012 Form 1041

-

Identifying Information:

- Essential details, such as the name and identification number of both the estate/trust and fiduciary, are required for processing.

-

Income Section:

- This area details all taxable income sources, which must be documented to comply with IRS regulations.

-

Deductions:

- Fiduciaries must carefully document any deductible expenses incurred during the management of the estate or trust.

-

Tax Computation:

- This section helps fiduciaries determine the correct tax liabilities and ensure that they conform with the statutory requirements set by the IRS.

Required Documents for Filing

To accurately complete and file the 2012 Form 1041, gather necessary documents like:

- Bank statements demonstrating income generated from investments.

- Documentation of deductible expenses such as legal fees and administrative costs.

- Relevant IRS publications and tables to verify tax rates and ensure accurate calculations.

Who Typically Uses the 2012 Form 1041

Fiduciaries of estates and trusts primarily use the 2012 Form 1041. These individuals are responsible for managing the assets of deceased individuals or entities funded for specific purposes, such as a trust. Fiduciaries must ensure taxes are reported correctly, meeting the legal obligations of managing estate or trust finances.

Legal Implications and Guidelines

The 2012 IRS Form 1041 carries critical legal significance, as incorrect filings can lead to IRS scrutiny and penalties. Complying with the IRS guidelines is imperative to avoid potential legal complications. Fiduciaries should consult IRS instructions specific to Form 1041 to confirm all parts of the form align with legal requirements and accurately reflect the estate or trust's financial status.

Filing Deadlines and Important Dates

For the 2012 tax year, Form 1041 was due by April 15, 2013. Fiduciaries could request an extension, changing the deadline to October 15, 2013. It's crucial for filers to keep abreast of IRS updates around deadlines and submit timely returns to avoid penalties.

Penalties for Non-Compliance

Failure to comply with Form 1041 filing requirements can result in penalties, calculated based on the overdue duration. The IRS mandates timely and accurate submissions of tax forms to prevent interest accumulation on unpaid or erroneous tax filings. Fiduciaries who delay or submit incorrect information risk fines that can significantly impact estate or trust funds, underscoring the importance of compliance.