Definition & Meaning

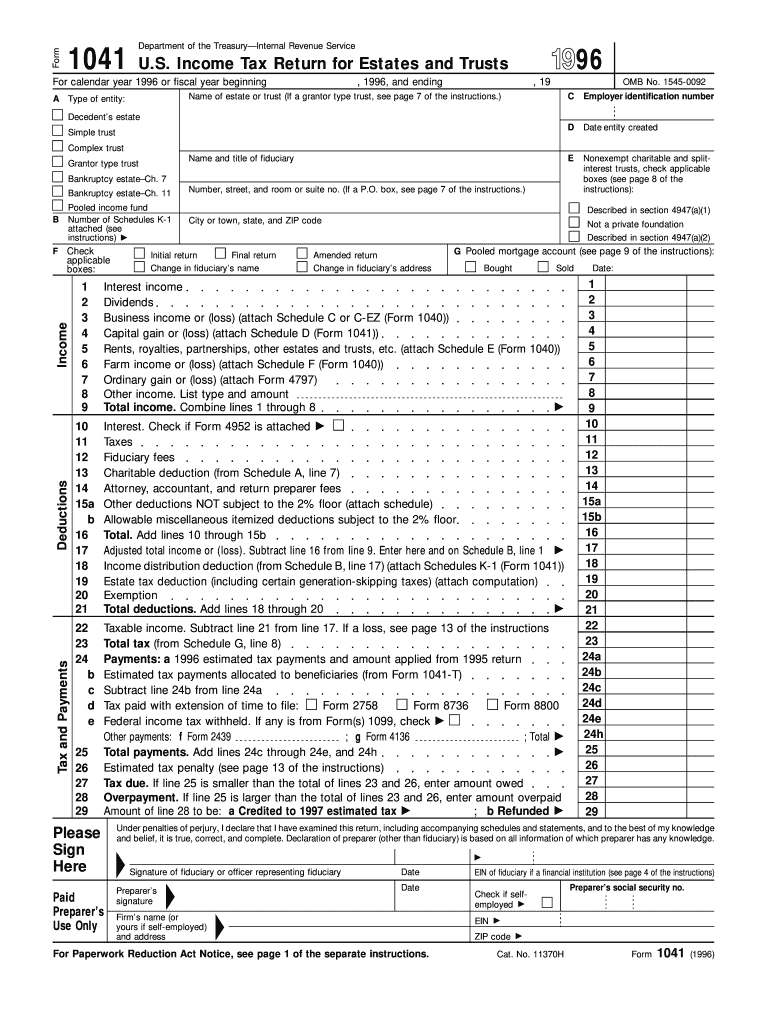

Form 1041 is the U.S. Income Tax Return for Estates and Trusts, a critical document used for reporting the income, deductions, and tax liabilities of estates and trusts for the tax year 1996. This form is essential for fiduciaries managing estates and trusts to comply with IRS requirements, ensuring transparency and accountability in declaring financial activities. The form includes sections for income such as dividends, capital gains, deductions like charitable donations, and calculations of taxable income and tax due. Understanding Form 1041 is crucial for accurate tax filing and compliance.

How to Use the IRS Form 1041 for 1996

To efficiently utilize the IRS Form 1041 for 1996, follow a methodical process:

-

Gather Necessary Information: Collect all relevant income records, including interest, dividends, rental income, and any other sources of income related to the estate or trust.

-

Complete Income Sections: Accurately fill in details pertaining to the income the estate or trust received during the year. This includes specifying any gains from securities or properties.

-

Identify Allowable Deductions: Determine deductions applicable to the estate or trust, such as administrative expenses, distributions to beneficiaries, and charitable contributions.

-

Calculate Taxable Income: Subtract total deductions from total income to determine the taxable income of the estate or trust.

-

Compute the Tax: Use tax tables or applicable rates for 1996 to calculate the tax liability based on the calculated taxable income.

These steps provide a structured approach to completing the form, ensuring accurate reporting and compliance.

Key Elements of the IRS Form 1041 for 1996

Several critical elements are pivotal in preparing IRS Form 1041 correctly:

- Filing Status: Confirm if the form pertains to a simple or complex trust, or a decedent’s estate.

- Deposit Requirements: Determine if estimated tax deposits are necessary for the fiscal year.

- Identification Section: Properly fill in identifying details, including the estate or trust’s name, fiduciary’s name and address, and employer identification number (EIN).

- Beneficiary Information: List the beneficiaries to whom income was distributed during the tax year.

- Schedule D: Include the report of capital gains and losses realized during the year.

Understanding and accurately filling each of these components ensures precise compliance and prevents errors leading to potential fines.

Legal Use of the IRS Form 1041 for 1996

The legal obligations surrounding the IRS Form 1041 rely heavily on correct usage and compliance:

- Fiduciary Responsibilities: Fiduciaries must ensure the form represents truthful financial information, accurately reporting income and deductions while aligning with the legal requirements.

- Tax Compliance: Meeting IRS guidelines and deadlines is crucial to avoid penalties. Legal use dictates adherence to the set tax laws for estates and trusts specific to 1996.

Strict compliance ensures legal protection and accountability under U.S. tax law, reinforcing the fiduciary’s role in estate and trust management.

Steps to Complete the IRS Form 1041 for 1996

Completing the form involves following detailed steps for accuracy:

-

Prepare Form: Use the correct 1996 version of Form 1041.

-

Enter Basic Information: Fill out the identification section with the estate or trust’s details.

-

Document Income Sources: List all income received, such as dividends, interest, and other income.

-

Capture Deductions: Input permissible deductions, ensuring all claimed deductions have proper supporting documentation.

-

Finalize Section Totals: Review and verify each section to ensure mathematical accuracy and compliance. Ensure totals are accurately computed across sections for consistency.

-

Review Fiduciary Details: Ensure the fiduciary signs and dates the document, affirming the accuracy and completeness of the information.

This step-by-step guide ensures fiduciaries complete the form efficiently, reducing errors and potential compliance issues.

Required Documents

Several documents are necessary for accurately completing Form 1041:

- EIN Assignment: Use the IRS-issued employer identification number pertinent to the estate or trust.

- Income Summaries: Collect all relevant financial forms, including 1099s and other income documentation. These provide verified income amounts for the tax year.

- Expense Receipts: Ensure you maintain a record of receipts for deductible expenses to support claims for deductions.

- Beneficiary Statements: Gather information on beneficiaries to whom distributions are made, necessary for completing schedules.

These documents support the information entered into Form 1041, ensuring all claims are validated.

Filing Deadlines / Important Dates

Adhering to the filing deadlines is crucial to avoid penalties:

- Standard Deadline: File the form by April 15, the common tax filing deadline unless an extension is applied for.

- Extension Possibility: Request an extension using Form 7004 if more time is required to prepare accurate reports.

- Estimated Tax Payments: Note due dates for any estimated payments required throughout the tax year to avert potential interest on underpayments.

Maintaining awareness of these timelines is vital for fiduciaries managing estates or trusts in 1996 to ensure compliance and avoid unnecessary penalties.

Penalties for Non-Compliance

Failure to submit Form 1041 timely and accurately can result in significant complications:

- Monetary Fines: Penalties for late filing can accrue rapidly and are based on the unfiled timeline duration.

- Interest on Late Payments: Interest will also be charged on late payments, compounding the financial burden.

- Increased Scrutiny: Non-compliance could result in heightened IRS scrutiny or audits, leading to thorough examinations of financial activities.

Ensuring timely and accurate submissions will mitigate these risks, promoting a smooth tax filing process and preserving the financial health of the estate or trust.