Definition and Purpose of Form 8829

Form 8829 is used by individuals to calculate and report expenses related to the business use of their home. This form is part of the IRS's provisions for self-employed individuals who wish to claim deductions for home office expenses on their Form 1040, Schedule C. The 2012 version of Form 8829 maintains the core functionalities of helping taxpayers determine the allocation of various expenses, such as utilities and mortgage interest, between personal and business use.

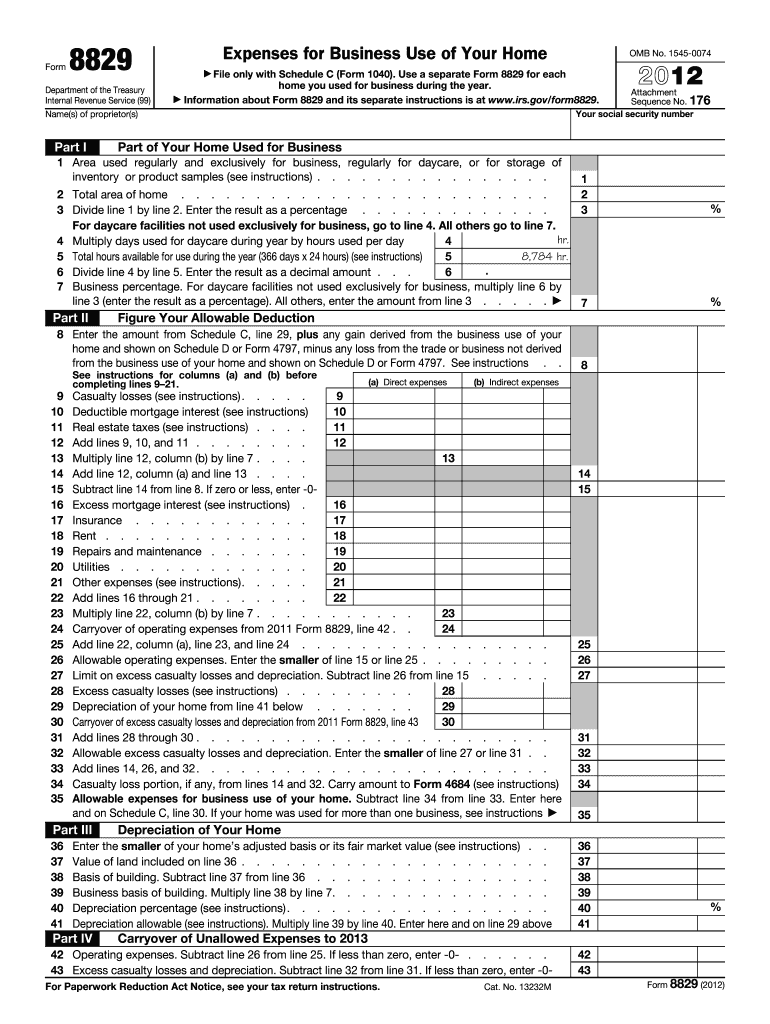

How to Use the 2012 Form 8829

- Calculate the Area Used for Business: Express this area as a percentage of your total home space.

- Direct and Indirect Expenses: Identify and allocate these expenses. Direct expenses are exclusively for the business portion of your home, while indirect expenses, such as utilities, are split based on the business use percentage.

- Depreciation Calculations: Calculate depreciation for the portion of your home used for business, which provides a significant tax benefit.

Steps to Complete the Form

- Fill out the Worksheet for Business Use of Your Home: Determine the percentage of your home used for business.

- List Direct Expenses: Include costs specific to the business portion, like repairs.

- Calculate Indirect Expenses: These include mortgage interest, insurance, utilities, and depreciation.

- Deduct Allowable Expenses: Only the business portion of each expense is deductible.

Obtaining the 2012 Form 8829

The 2012 Form 8829 can be accessed through several channels:

- IRS Website: It is downloadable in PDF format from the IRS's official site.

- Tax Software: Many tax preparation programs, such as TurboTax and QuickBooks, include this form within their suite of documents.

- Tax Professionals: Accountants and tax preparers can provide the form and assist with its completion.

Key Elements of Form 8829

- Business Percentage Calculation: Critical for determining deductible expenses.

- Direct vs. Indirect Expenses: Document both types separately for accuracy.

- Carryover of Unused Expenses: Expenses exceeding gross income can be carried over to future years.

Legal Use and Compliance

Individuals using Form 8829 must do so with the understanding that:

- Only Space Exclusively Used: The IRS mandates that the space must be primarily and exclusively used for business purposes.

- Compliance with IRS Guidelines: Proper documentation and accurate calculations are essential to avoid audits.

Examples of Using the 2012 Form 8829

- Freelance Graphic Designer: Uses a dedicated room as a studio, claiming deductions proportional to the studio's size relative to the home.

- Real Estate Agent: Conducts substantial business from an in-home office, deducting related utility costs.

IRS Guidelines and Important Dates

- Submission Deadline: Typically aligns with the federal tax filing deadline, April 15, unless an extension is granted.

- Record Keeping: Maintain records for at least three years in case of an audit.

Required Documents for Filing

- Mortgage Statements: For interest and principal payments.

- Utility Bills: Document all utilities used.

- Home Insurance: Obtain policy details for premium deductions.

Penalties for Non-Compliance

Failure to accurately complete Form 8829 can result in:

- Fines and Back Taxes: If deductions are improperly claimed.

- Increased Audit Risk: Business use must meet IRS stipulations.

Variants or Alternatives to Form 8829

While Form 8829 is primarily for self-employed individuals, other business entities like LLCs and corporations may use different IRS forms to claim business use deductions. Understanding the specific needs of your business type is essential for proper filing.