Definition and Purpose of 2004 Form 8829

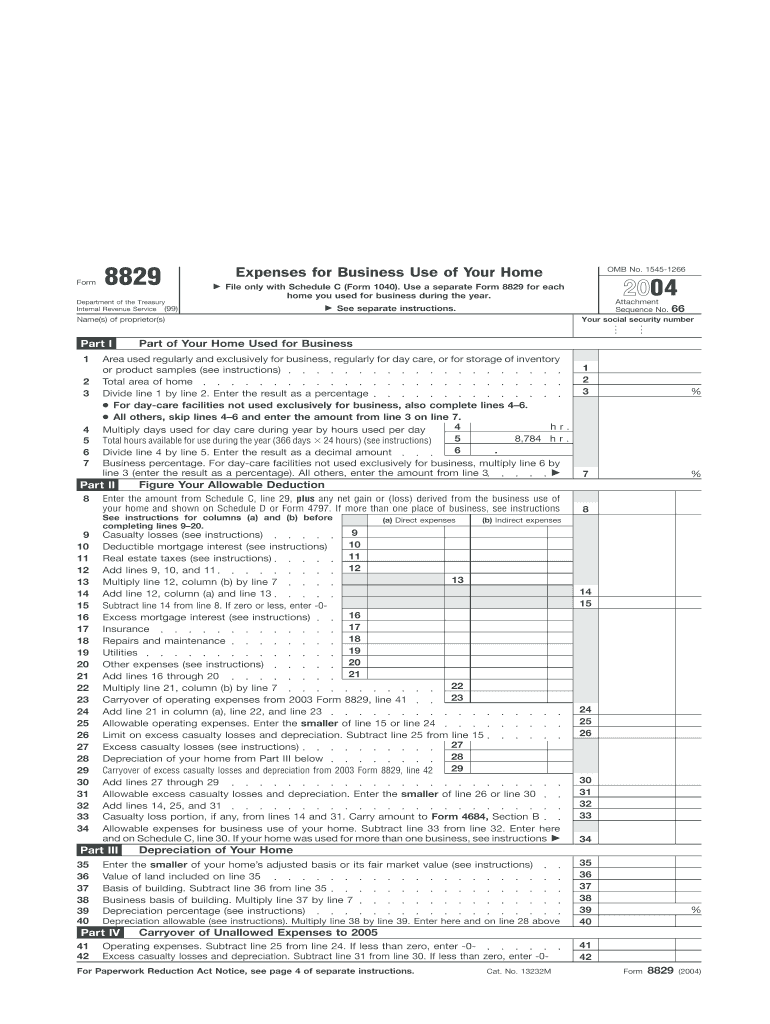

The 2004 Form 8829, titled "Expenses for Business Use of Your Home," is an IRS form used by U.S. taxpayers to calculate and report eligible expenses related to using their home for business purposes. It is primarily used by self-employed individuals or small business owners who operate from a part of their residence. The form allows taxpayers to determine the deduction amount they can claim for a proportionate share of their home expenses, such as mortgage interest, utilities, and depreciation.

Key Elements Covered in the Form

- Direct and indirect expenses: Differentiates between expenses directly related to the business area (e.g., painting a home office) and general home expenses (e.g., heating), which require allocation based on space usage.

- Depreciation: Calculates depreciation on the portion of the home used for business, considering factors like the home's fair market value and its useful life.

- Multiple business use sections: Provides guidelines for different areas used for separate business activities, ensuring accurate allocation of expenses.

Steps to Complete the 2004 Form 8829

Preparation and Required Documentation

- Gather records of direct expenses related to the business area and indirect expenses for the entire home.

- Calculate the percentage of home used for business by dividing the business-use area by the total area of the home.

Completing the Form

-

Part I - Calculate Your Home's Business Use:

- Enter the square footage of your home and the area used for business.

- Compute the percentage used for business purposes.

-

Part II - Figure Your Allowable Deduction:

- List direct expenses (e.g., repairs to the home office) and indirect expenses (e.g., utilities for the entire home).

- Multiply indirect expenses by the business-use percentage to get deductible amounts.

-

Part III - Depreciation of Your Home:

- Provide details about the property, including purchase price and improvement costs.

- Calculate depreciation specific to the business-use portion.

-

Part IV - Carryover of Unallowed Expenses:

- Report any expenses that could not be deducted in previous years due to limitations.

Why You Should Use the 2004 Form 8829

The form enables business owners to take advantage of the home office deduction, thus potentially reducing taxable income significantly. Claimed correctly, these deductions can lead to substantial tax savings by accurately attributing home expenses to business activities.

- Tax Efficiency: Deductions on valid business expenses reduce overall taxable income.

- Compliance: The form ensures adherence to IRS guidelines, minimizing audit risks.

- Clarification: It provides a standardized method for tracking and reporting home office expenses.

IRS Guidelines and Compliance for 2004 Form 8829

Eligibility Criteria

- Must use a portion of your home exclusively and regularly for business purposes.

- The home office should be the principal place of business or used for meeting clients regularly.

Legal Use and Compliance

- The IRS requires that the home office is utilized solely for business activities, with no personal use.

- Keep detailed records and documentation supporting the deduction claim in case of an audit.

Who Typically Uses the 2004 Form 8829

Primary Users

- Self-Employed Individuals: Such as freelancers and consultants who work from home.

- Small Business Owners: Particularly those conducting operations within their residences.

Business Entity Types

- Sole proprietorships and single-member LLCs primarily utilize this form with Schedule C of Form 1040.

- Partnerships and corporations might need different protocols or forms for similar deductions.

Examples and Scenarios of 2004 Form 8829 Usage

- Freelance Graphic Designer: Uses part of their home studio strictly for designing projects, claiming expenses for the specific area.

- Independent Consultant: Meets clients in a dedicated home office and claims proportional deductions on home expenses.

Real-World Scenario

An independent accountant uses her basement exclusively for business activities. Her total home is 2,000 square feet, with a 200 square foot office. She will claim 10% of indirect home expenses and direct office supplies as deductions, precisely calculated using Form 8829.

Filing Deadlines and Submission Methods

- Filing Deadlines: Aligns with the taxpayer's annual tax filing deadline, typically April 15th. Extensions may apply if requested.

- Submission: File with IRS Form 1040 Schedule C. Options include electronic filing via tax software or mailing a printed copy, ensuring comprehensive documentation accompanies the submission.