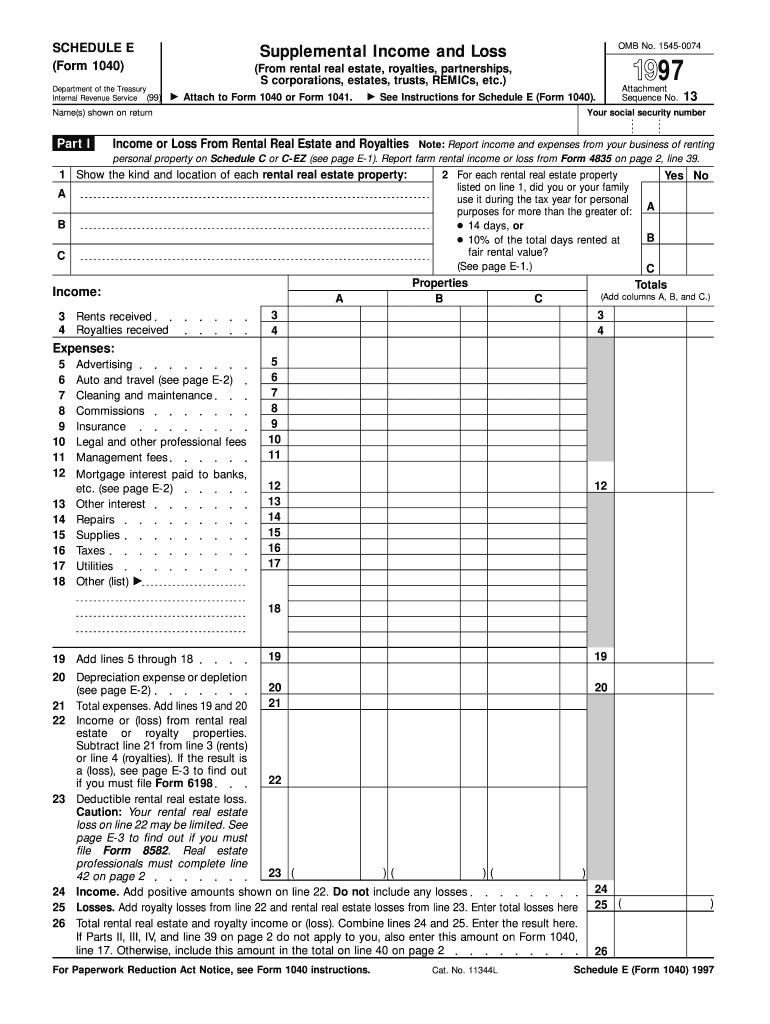

Definition and Purpose

Schedule E (Form 1040) is used by individuals in the United States to report supplemental income and loss from various sources, such as rental real estate, royalties, partnerships, S corporations, estates, trusts, and REMICs. The 2013 version of this form is designed for activities related to the year 1997. It serves as a comprehensive document for the detailed reporting of various income streams that differ from standard wages and salaries. This specificity provides a clear structure for taxpayers to itemize their earnings and expenses to ensure accurate tax liability computations.

Key Elements of Schedule E 2013 Form 1997

The form includes various sections tailored to capture different types of income. It encompasses individual spaces for each type of income and its related expenses, thus avoiding potential discrepancies. For example:

- Rental Income and Expenses: Captures gross income from rental properties, including allowable deductions such as property taxes and mortgage interest.

- Royalty Income: Accounts for payments from intellectual property rights or resource extraction leases.

- Partnership and S Corporation Income: Details pass-through income that individuals receive from these business ventures.

Each part of the form is accompanied by clear instructions to guide users in accurately recording their financial information.

How to Obtain the Schedule E 2013 Form 1997

Individuals can access the form through various methods to suit different preferences. Options include:

- Online Download: The most efficient way is to download the form directly from the IRS website, ensuring it's the officially endorsed version.

- In-person Pickup: Forms can also be retrieved from IRS offices or certain public libraries that provide tax form access during tax season.

- Mail: Taxpayers can request that printed copies of the form be mailed directly to their residence through an IRS request service.

Steps to Complete Schedule E 2013 Form 1997

Filling out the form requires careful attention to detail. The process involves:

- Gather Required Information: Collect documentation, such as lease agreements, royalty contracts, or K-1 forms, which provide necessary information about income sources.

- Enter Income and Expense Details: Input data into the appropriate sections while ensuring figures are accurate.

- Calculate Totals: Sum totals in designated areas for income and any expenses that apply, using specific guidance in the form to handle unique cases like passive loss limitations.

- Review and Sign: Once completed, thoroughly review entries for accuracy before signing.

Who Typically Uses the Schedule E 2013 Form 1997

This form is typically utilized by:

- Property Owners: Individuals who own rental properties must disclose earnings and costs associated with these assets.

- Creative Professionals: Artists and writers often use this form to report royalties.

- Business Stakeholders: Partners or S corporation shareholders need this form for reporting their share of income or losses.

IRS Guidelines Regarding the Form

The Internal Revenue Service provides specific guidelines to ensure compliance. These include:

- Accuracy Requirements: It's important to provide precise information reducing error risks which may lead to audits.

- Submission Deadlines: Typically coincides with the annual tax filing date, often April 15th unless extensions are granted.

- Documentation: IRS guidelines suggest maintaining all relevant financial documents for at least three years after filing in case of review or audit.

Filing Deadlines and Important Dates for the Form

Specific timelines must be adhered to when submitting the Schedule E 2013 Form 1997:

- Standard Due Date: Aligns with the federal tax deadline, usually April 15th.

- Extensions: Taxpayers may apply for an extension, providing extra time to file without incurring penalties, generally extending the deadline to October 15th.

- Amendment Periods: Corrections can often be made by submitting an amended form up to three years from the original due date.

Penalties for Non-Compliance

Failing to complete or submit the form by the deadline can lead to significant repercussions. These may include:

- Late Fees: Imposed for delays in submission, often calculated as a percentage of unpaid taxes due.

- Interest on Unpaid Taxes: Accumulated on outstanding balances from the original filing date.

- Possible Criminal Prosecution: In severe cases of fraud or intentional evasion.

In-depth understanding and adherence to these sections ensure taxpayers accurately report their income, remain compliant with IRS regulations, and avoid unnecessary penalties.