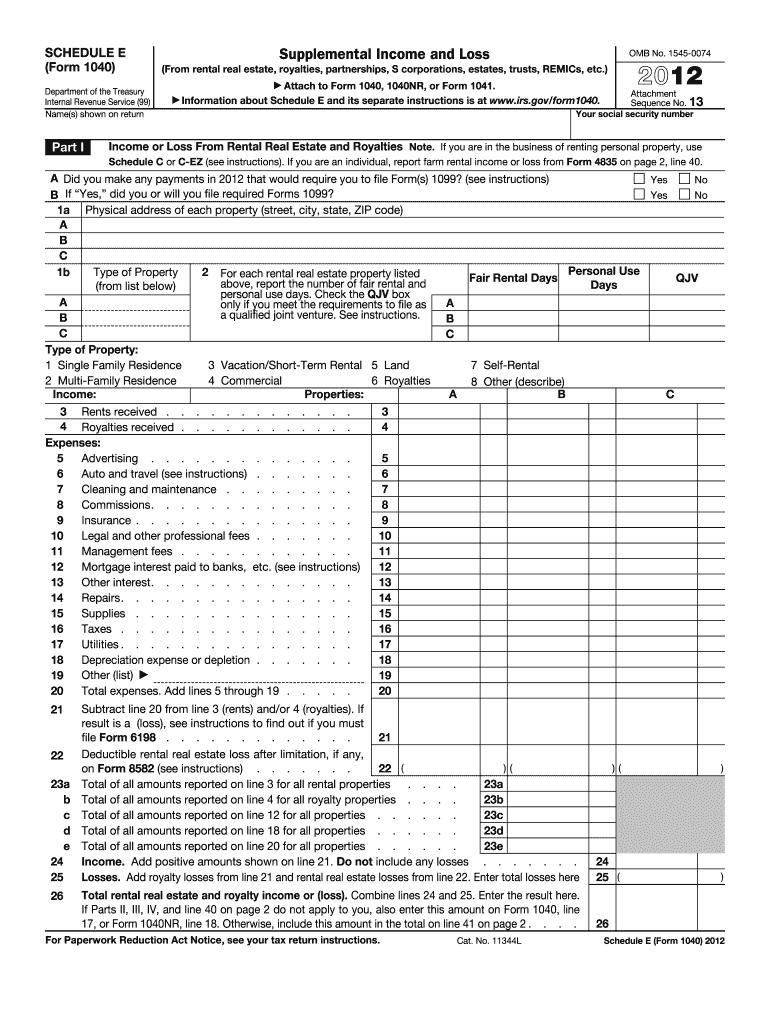

Definition and Purpose of the 2012 Form 1040 (Schedule E)

The 2012 Form 1040 (Schedule E) is used by individuals in the United States to report supplemental income and loss. This form is crucial for detailing income generated from various sources, including rental real estate, royalties, partnerships, S corporations, estates, trusts, and residual interest in Real Estate Mortgage Investment Conduits (REMICs). It aids taxpayers in documenting and calculating income and expenses related to these activities while adhering to IRS requirements. The form consists of different parts that guide users through reporting specifics for each income source, ensuring a comprehensive capture of financial information.

Steps to Complete the 2012 Form 1040 (Schedule E)

Completing the 2012 Form 1040 (Schedule E) involves several steps to ensure accuracy:

-

Gather Required Documents:

- Obtain records of all income sources such as bank statements, rent receipts, and partnership reports.

- Collect records of expenses incurred related to each income source.

-

Part I — Rental Real Estate and Royalties:

- Enter income received from rental properties or royalty payments.

- Deduct expenses like advertising, maintenance, property taxes, and depreciation.

-

Part II — Income or Loss from Partnerships and S Corporations:

- Include details from Schedule K-1 forms received from partnerships or S corporations.

- Report income and deductions as indicated on Schedule K-1.

-

Part III — Income or Loss from Estates and Trusts:

- Use Schedule K-1 from estates or trusts to report relevant distributions or losses.

-

Part IV & V — Income or Loss from Residual Interests:

- Document any income, deductions, and taxes paid for your interest in REMICs.

-

Review and Finalize:

- Double-check entries for accuracy and ensure all calculations are correct.

- Attach the completed Schedule E to your Form 1040 and file by the deadline.

Key Elements of the 2012 Form 1040 (Schedule E)

- Income Reporting: Accurately document the origin and amount of income from each source. This includes the differentiation between passive and non-passive income.

- Expense Documentation: Detail expenses associated with earning supplemental income, such as management fees for rental properties or business-related travel.

- Partnerships and S Corporations: Summarizes income, credits, and deductions passed through from business entities to individual taxpayers.

- Trust and Estate Distributions: Accurately reflect income received from estates and trusts, ensuring compliance with specific IRS guidelines.

- Tax Implications: Understanding potential tax liabilities associated with different income types, ensuring comprehensive compliance with tax laws.

Important Terms Related to the 2012 Form 1040 (Schedule E)

- Passive Activity: This refers to any business activity in which the taxpayer does not materially participate, such as rental income from property not actively managed by the owner.

- At-Risk Rules: Regulations limiting the amount of deductible loss to the amount a taxpayer has at risk in the activity.

- Material Participation: Engaging in the operations of an activity on a regular, continuous, and substantial basis.

- Depreciation: An income tax deduction that allows a taxpayer to account for the decrease in value of tangible property over time.

- Schedule K-1: A form used to report an individual’s share of income, deductions, and credits from a partnership, S corporation, estate, or trust.

Filing Deadlines and Important Dates

- Annual Tax Filing Deadline: Typically, April 15th is the due date for filing income tax returns, including Schedule E, unless the date falls on a weekend or holiday.

- Extension Requests: If more time is needed, a request for a six-month filing extension can be submitted using Form 4868 before the original deadline.

- Quarterly Estimated Tax Payments: For those with substantial supplemental income, estimated tax payments may be required quarterly to avoid underpayment penalties.

IRS Guidelines and Compliance

Adhering to IRS guidelines when completing Schedule E is essential. The IRS provides detailed instructions for each line item on the form. This ensures that taxpayers understand where specific income and deductions should be reported. Following these guidelines helps in avoiding discrepancies that could trigger audits or penalties. Understanding the rules for passive versus non-passive income, as well as at-risk limitations, is crucial for accurate reporting.

Taxpayer Scenarios and Examples

- Self-Employed Individuals: Those managing rental properties along with self-employment must report all rental income and related expenses on Schedule E while keeping self-employment income on Schedule C.

- Retirees with Rental Properties: Retirees who supplement their income with rental payments need to use Schedule E to account for this income stream accurately.

- Individuals with Multiple Income Sources: Taxpayers with income from diverse sources, like royalties and trust distributions, need to document each separately to meet IRS requirements effectively.

Penalties for Non-Compliance

Failing to file Schedule E accurately can result in penalties:

- Underreporting Penalties: Providing incorrect information could lead to fines or interest on unpaid taxes.

- Negligence or Fraud Penalties: Serious errors or deliberate misreporting may incur substantial penalties or even legal repercussions.

- Missed Deadlines: Late submission can result in penalties unless an officially granted extension is in effect.

Navigating the requirements of the 2012 Form 1040 (Schedule E) demands meticulous documentation and adherence to IRS guidelines. Proper filing ensures compliance, optimizes tax liabilities, and prevents costly errors.