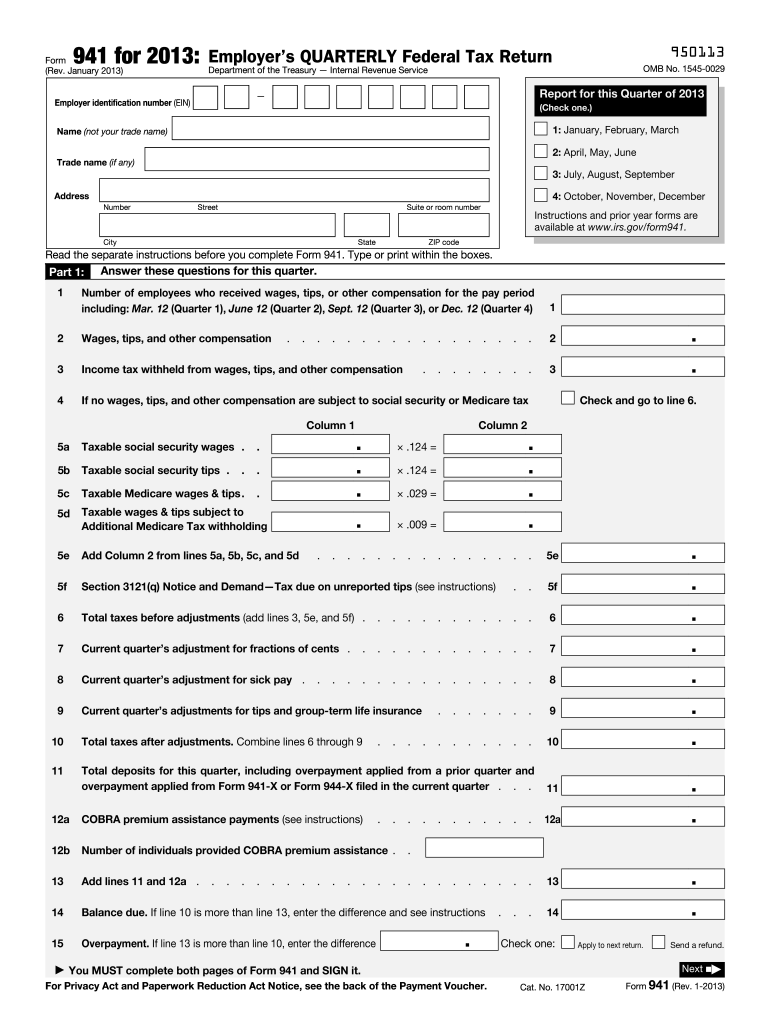

Overview of the 2013 Form 941

The 2013 Form 941, known as the Employer's Quarterly Federal Tax Return, is a vital document used by employers to report and remit federal taxes withheld from their employees’ wages. It includes detailed sections for ensuring accurate reporting of income taxes, Social Security tax, and Medicare tax. Employers need to complete this form each quarter to remain compliant with federal regulations.

Steps to Complete the 2013 941 Form

-

Gather Required Information: Before starting, compile all necessary data including employee wages, withheld income taxes, and details of Social Security and Medicare payments.

-

Fill Out Basic Employer Information: This includes the employer identification number (EIN), name, address, and the quarter being reported.

-

Report Employee Wages and Taxes:

- Start with total wages, tips, and other compensation paid to employees.

- Report the federal income tax and Social Security tax withheld from these wages.

- Provide details of employer and employee portions of Medicare tax.

-

Adjustments and Corrections: Make necessary adjustments for fractions of cents, sick pay, or tips, and include prior period adjustments if any errors were corrected in the current quarter.

-

Calculate Tax Liabilities: Calculate the exact tax amount owed for the quarter and verify the amounts.

-

Sign and Date the Form: An authorized person must sign the form to validate it.

How to Obtain the 2013 Form 941

- Download from the IRS Website: Employers can download the 2013 Form 941 directly from the IRS official website, ensuring they have the correct version.

- Request via Mail: You can request a physical copy from the IRS, which will be mailed to your business address.

- Tax Software and Services: Many tax preparation software programs, like TurboTax or QuickBooks, provide printable versions of Form 941, allowing for easy integration into electronic filing systems.

Important Dates for Filing the 2013 Form 941

- Quarterly Deadlines: The form must be filed quarterly. Key deadlines are as follows:

- First Quarter: Due by April 30

- Second Quarter: Due by July 31

- Third Quarter: Due by October 31

- Fourth Quarter: Due by January 31 of the following year

- Extensions: Extensions are generally not available for filing Form 941, emphasizing the importance of timely submission.

Penalties for Non-Compliance

Failure to file the 2013 Form 941 on time can result in substantial penalties, including:

- Late Filing Penalty: Generally 5% of the unpaid tax for each month the return is late, up to a maximum of 25%.

- Late Payment Penalty: Usually 0.5% per month of any taxes not paid by the due date, again capping at 25%.

Employers must ensure timely filing and payment to avoid these penalties, which can significantly affect a business’s finances.

Form Submission Methods

- Online Submission: Employers can file Form 941 through the IRS’s electronic filing system, making the process efficient and reducing errors.

- Mail: Alternatively, the form can be printed and mailed to the IRS. Ensure the correct IRS address is used based on your state and payment inclusion.

Key Elements of Form 941

- Part 1: Employee Information: Captures gross wages, tips, taxes withheld, and computes the total tax due.

- Part 2: Tax Calculation: Involves detailed calculations regarding Social Security and Medicare taxes.

- Part 3: Adjustments: Adjustments for fractions of cents, third-party sick pay, etc.

- Part 4: Additional Information: Requests signature, phone number, and date to complete the form.

Understanding these elements helps ensure correct completion and compliance.

Software Compatibility

Various tax software solutions support Form 941, enhancing efficiency in preparation:

- TurboTax and QuickBooks: These offer features for calculating taxes accurately and preparing the form seamlessly.

- Interfaces with Payroll Systems: Many software systems integrate with payroll services, automatically populating necessary data into the Form 941.

Verifying software compatibility ensures data integrity and streamlines the filing process.

Who Typically Uses the 2013 Form 941

- Employers Across Industries: Any employer withholding federal taxes must complete this form.

- Non-Profit Organizations: Entities exempt from income tax still use Form 941, as they withhold employment taxes.

- Government Agencies: Government bodies with employees also submit this form quarterly, reporting withheld taxes in a similar fashion to private employers.

Employers must be aware of their obligations to appropriately complete this quarterly form.