Definition and Meaning of Form 656

Form 656 is utilized by taxpayers in the United States to propose an Offer in Compromise (OIC) to settle outstanding tax liabilities with the IRS for less than the full amount owed. This form is part of the broader IRS program aimed at assisting those in financial difficulty. An OIC can be an effective tool for taxpayers experiencing certain financial hardships, allowing them to negotiate manageable payment agreements based on their financial situation.

Key Elements of Form 656

- Taxpayer Information: Provides personal details of the taxpayer, including name, address, and Social Security number.

- Offer in Compromise Terms: Specifies the proposed amount to settle the tax liabilities and the payment terms.

- Reason for Offer: Requires taxpayers to indicate the reason for their offer, such as doubt as to collectability or effective tax administration.

- Financial Disclosure: Involves providing detailed financial information that supports the taxpayer's inability to pay the full tax debt.

How to Use Form 656

Using Form 656 requires a thorough understanding of your financial situation as it directly impacts your offer's acceptance. The IRS evaluates your ability to pay, income, expenses, and asset equity to determine if the offered amount is sufficient. Taxpayers should ensure all necessary documentation accompanies the form to streamline the consideration process.

Steps to Complete Form 656

- Gather Financial Information: Collect comprehensive records of your income, living expenses, assets, and liabilities.

- Calculate Your Offer: Based on IRS guidelines, compute an offer amount that reflects your financial capability.

- Complete Necessary Sections: Fill out each section of the form, including personal details and offer terms.

- Attach Supporting Documents: Ensure all required financial documentation and any other relevant forms are attached.

- Submit the Form: Send the completed form and documentation to the IRS, while keeping copies for personal records.

Who Typically Uses Form 656

Form 656 is predominantly used by individuals, self-employed individuals, and businesses who face significant financial hardship. Taxpayers must demonstrate that they cannot meet their tax liabilities in order to use this form effectively. It's an option for those with limited income, unmanageable debts, or significant financial burdens beyond their control.

Important Terms Related to Form 656

Understanding the terminology associated with Form 656 is crucial for completing it accurately:

- Offer in Compromise (OIC): A negotiated agreement to satisfy tax liabilities for less than owed.

- Doubt as to Collectability: A situation where a taxpayer's financial condition suggests they will never be able to pay the full amount.

- Effective Tax Administration: Used when full payment would create an undue economic hardship for the taxpayer.

Eligibility Criteria for the Offer in Compromise

To determine if you qualify for using Form 656, review the IRS guidelines on eligibility:

- Filing Status: All required tax returns must be filed before applying for an OIC.

- Estimated Payments: Must be up to date with current year's estimated tax payments.

- Revenue Officer Scenario: Taxpayer should not be bankrupt or in an active bankruptcy proceeding.

IRS Guidelines for Completing Form 656

Accurate completion in line with IRS guidelines is essential:

- Payment Options: Choose between lump-sum or periodic payment plans.

- Current Compliance: Ensure compliance with IRS filing requirements.

- Documentation: Submit complete financial disclosure statements alongside the form.

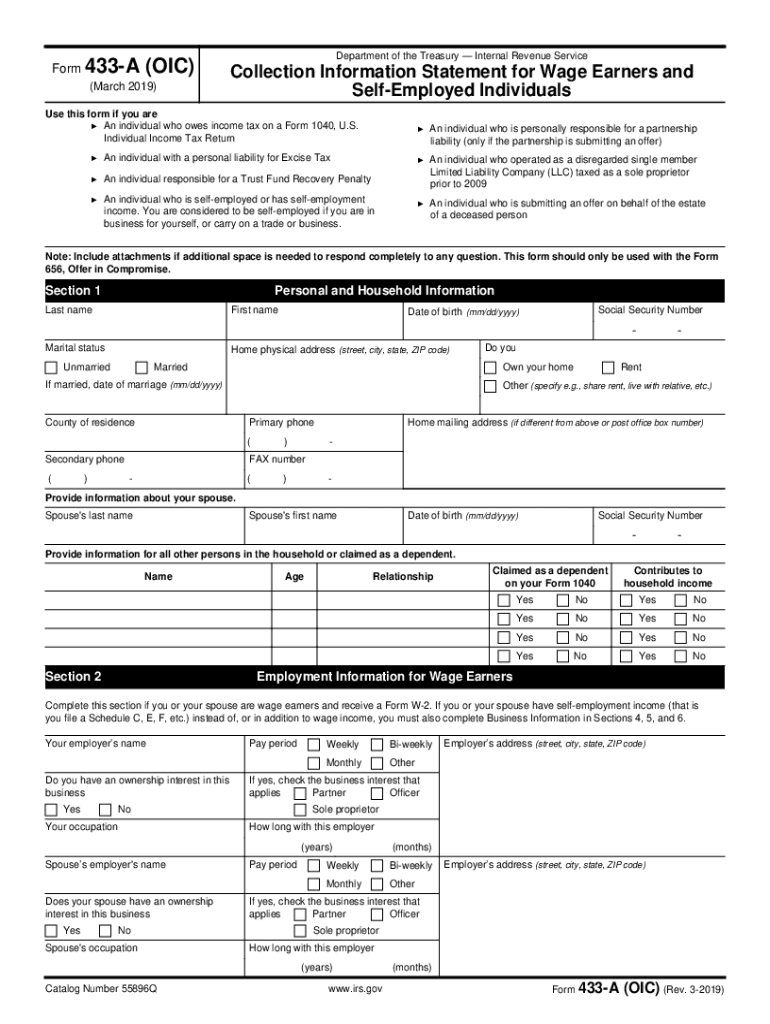

Required Documents

- Form 433-A: For individuals to list personal financial details.

- Form 433-B: For businesses to provide essential financial information.

- Verification: W-2s, 1099s, bank statements, and expense documentation.

Penalties for Non-Compliance

Failing to comply with the terms post-approval can result in penalties:

- Rejection of Offer: Incomplete forms or insufficient documentation can lead to rejection.

- Continuing Interest and Penalties: Accruing until the offer is considered and approved.

- Potential for Agreement Nullification: If terms of the offer are breached, the IRS may void the agreement, reinstating the original debt.

Form Submission Methods

Form 656 can be submitted through:

- Mail: Send to the IRS office specified for OIC submissions.

- In-Person: Drop-off at IRS Taxpayer Assistance Centers.

- Online: Utilize the IRS's online options for quicker response time.

State-Specific Rules for Form 656

While the IRS governs the overall OIC process, state-specific tax obligations may impact your situation:

- Align state and federal tax resolutions to maximize compliance.

- Consult state tax officials or financial advisors for area-specific guidance.

Understanding how these aspects apply to your circumstances can greatly enhance the likelihood of a favorable outcome when using Form 656 to settle tax obligations.