Definition and Meaning

Form 656-B (Rev. 3-2018), known as the Form 656 Booklet Offer in Compromise, is a comprehensive guide provided by the Internal Revenue Service (IRS) that details the Offer in Compromise program. This program allows taxpayers to settle their tax debts for less than the full amount owed. It's designed to help individuals who might not be able to pay their full tax liabilities due to financial hardship. The booklet includes thorough explanations of eligibility criteria, application processes, and the various forms involved, such as Form 433-A and Form 433-B.

Taxpayer Scenarios

- Self-Employed: May use the Offer in Compromise if business income fluctuates greatly.

- Retired Individuals: Often apply due to reduced income and fixed expenses.

- Students: Might consider it if they have prior tax liabilities but limited current income.

How to Use the Form 656-B

The Form 656-B booklet provides a step-by-step guide on how to apply for an Offer in Compromise. It is crucial to follow the outlined process meticulously to ensure a complete application. The guide helps applicants determine their eligibility, fill out necessary paperwork, calculate an acceptable offer amount, and understand the financial documentation required. Accuracy and thoroughness in this process are vital, as incomplete applications may lead to rejection.

- Eligibility Verification: Review Chapter 1 to ensure all criteria are met before proceeding.

- Document Compilation: Gather all necessary financial statements and tax documents.

- Completion of Forms: Fill out Forms 433-A and 433-B meticulously with attention to detail.

- Offer Calculation: Use the guidelines to determine a realistic offer based on your financial capacity.

Key Elements of the Form 656-B

The booklet includes essential components necessary for the application process:

- Eligibility Requirements: Detailed in the early sections to quickly establish who can apply.

- Application Procedures: Step-by-step instructions on form completion and submission.

- Payment Options: Information on acceptable payment plans and terms.

- Required Documentation: Lists of all forms and financial documents needed.

Filing Deadlines and Important Dates

Timeliness is a vital aspect of the Offer in Compromise program. The booklet emphasizes adhering to submission deadlines and the importance of maintaining compliance with current tax return filings. Late submissions may result in penalties or application refusal.

Important Terms Related

Several critical terms are central to understanding the form:

- Offer in Compromise: An IRS program allowing partial settlement of taxes owed.

- Doubt as to Liability: A situation where the tax debt amount is questioned.

- Effective Tax Administration: Consideration for compromise when paying the full amount causes economic hardship.

Eligibility Criteria

The Form 656 Booklet notes the primary eligibility conditions for applying for an Offer in Compromise:

- Inability to Pay: The taxpayer must demonstrate that paying the full amount would create financial hardship.

- Compliance: All required tax returns must be filed for the current year and prior years.

- Income and Asset Evaluation: Thorough evaluation of financial situation to justify the offer amount proposed.

Business Entity Types

- LLC and Corporations: Can apply if demonstrating inability to meet tax obligations due to economic hardship.

- Partnerships: May also qualify under similar conditions as individuals.

IRS Guidelines

The IRS outlines specific guidelines to follow when preparing and submitting an Offer in Compromise. The booklet highlights adherence to these guidelines as crucial for successful application processing. Components include:

- Detailed Financial Disclosure: Accurate representation of current and future income, expenses, and asset values.

- Payment Options Compliance: Offers must be accompanied by initial payments and fees as specified by IRS guidelines.

Application Process and Approval Time

The application process involves several stages, including submission, review, and potential negotiation. The IRS typically evaluates offers within six to twelve months, depending on complexity.

- Pre-Submission Action: Confirm compliance with all tax obligations and prepare financial documentation.

- Submission: Include all completed forms, financial data, and applicable fees.

- Review Period: The IRS will audit the application for accuracy and eligibility, often requesting further information.

- Negotiation and Finalization: Some offers undergo negotiation if initial terms are not acceptable.

Examples of Using the Form 656-B

- Case of John Doe, a Single Parent: Faced with significant medical expenses, John utilized Form 656-B to propose an offer, demonstrating his inability to pay the full debt while supporting his family.

- Business Example: A restaurant owner experiencing a downturn applied for an Offer in Compromise to manage tax liabilities accumulated during the recession.

Required Documents

To complete the Offer in Compromise process, the following documents are typically required:

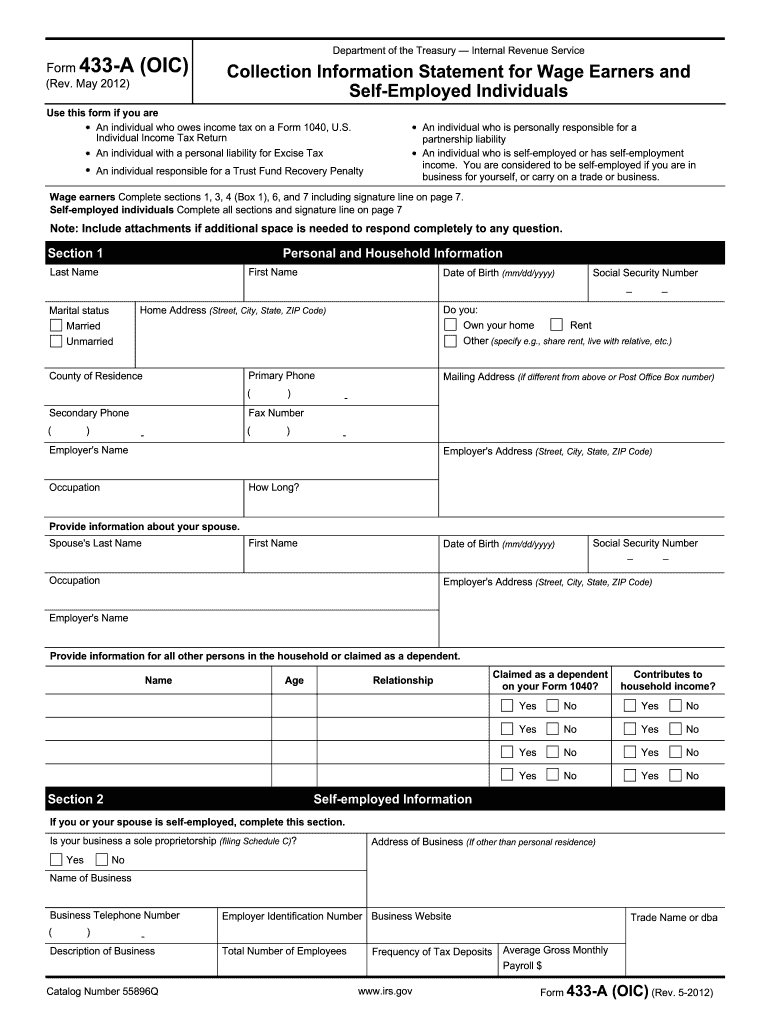

- Form 433-A (OIC): Collection Information Statement for wage earners and self-employed individuals.

- Form 433-B (OIC): Collection Information Statement for businesses.

- Latest Federal Tax Return: Supporting data regarding current financial status.

Form Submission Methods

The booklet specifies different methods of submission:

- Online: Via the IRS e-Services system for faster processing.

- Mail: Submissions can be sent directly to designated IRS addresses.

- In-Person: Handled at local IRS offices for more personalized assistance.

Understanding each of these sections ensures a well-prepared and timely submission of the Offer in Compromise application, maximizing the chances of success in resolving tax debts.