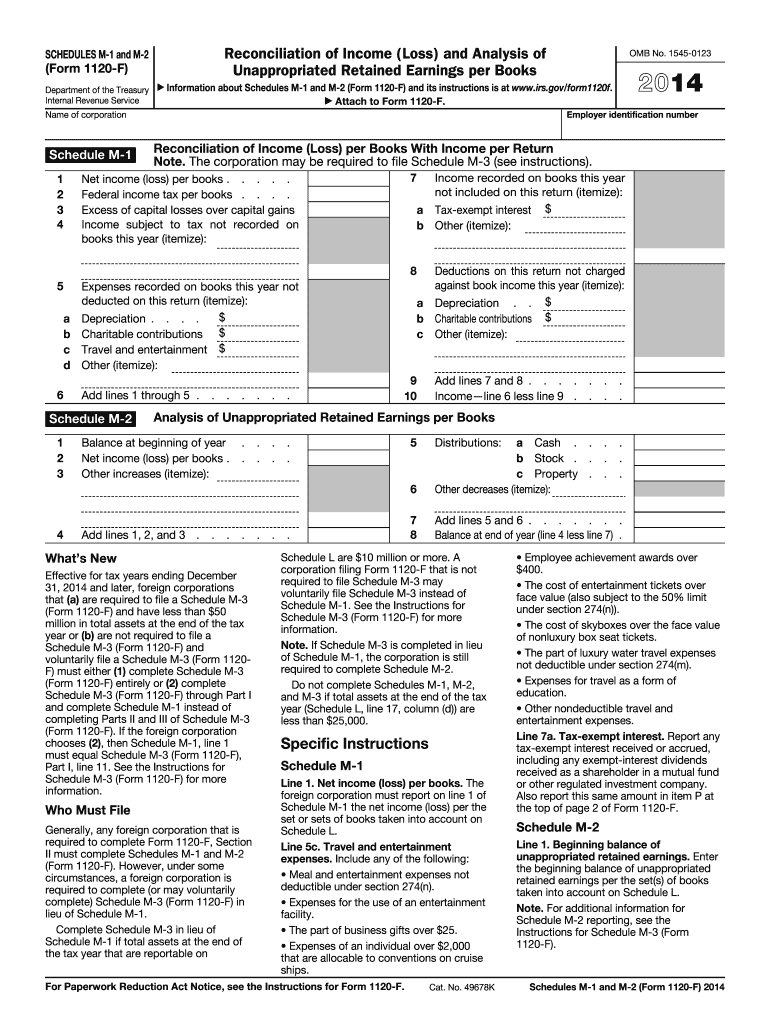

Definition & Purpose of the 2014 M-2 Form

The 2014 M-2 form is a critical component of Form 1120-F, used primarily by foreign corporations to reconcile income or loss per books with income reported on tax returns. This specific form also assists in analyzing unappropriated retained earnings. It is essential for corporations that need to provide a detailed account of their financial activities as regulated by the IRS.

- Role in Financial Reconciliation: The M-2 form helps reconcile discrepancies between book-maintained earnings and tax-computed income.

- Scope: Applicable to foreign corporations, ensuring compliance with U.S. tax regulations.

- Primary Objective: Understanding and documenting changes in a corporation's retained earnings over the year.

How to Obtain the 2014 M-2 Form

Accessing the 2014 M-2 form is essential for ensuring timely compliance for foreign corporations.

- Download from IRS Website: The IRS provides access to downloadable PDF versions of the form.

- Use Tax Preparation Software: Tools like TurboTax or QuickBooks often include downloadable tax forms within their platforms for easy access.

- Request via Mail: Corporations can request the form directly from the IRS if preferred.

Steps to Complete the 2014 M-2 Form

Understanding the completion process of the M-2 form is crucial for accuracy in financial reporting.

- Gather Required Information: Before starting, collect all financial records, including income statements and balance sheets.

- Identify All Income and Adjustments: Clearly note all income streams and necessary adjustments from book income to tax income.

- Complete Financial Reconciliation: Accurately calculate differences and provide explanations for any discrepancies.

- Review and Validate Entries: Ensure all figures are accurate and entries match supporting documentation.

- Submit in Accordance with IRS Guidelines: Follow the IRS-defined methods for submitting the form, ensuring it meets all regulatory criteria.

Key Elements of the 2014 M-2 Form

Focusing on the central components of the M-2 form enables corporations to meet all necessary filing requirements.

- Reconciliation Details: Includes summarizing the opening balance, additions, and subtractions to determine closing retained earnings.

- Book-to-Tax Differences: Clarify all adjustments made from book to tax.

- Supporting Documentation: Link all figures to corresponding documents to substantiate claims.

Who Typically Uses the 2014 M-2 Form

The M-2 form is tailored for specific organizational use cases.

- Foreign Corporations: Primarily designed for corporations operating outside the United States but conducting business that is taxable within its jurisdiction.

- Entities with IRS Filing Obligations: Those required to file Form 1120-F under IRS standards.

IRS Guidelines for the 2014 M-2 Form

Understanding IRS guidelines ensures compliance and avoids common pitfalls.

- Regulatory Requirements: Follow the stipulated rules regarding the form's preparation and submission.

- Use of Schedule M-3: Recognize instances where Schedule M-3 may be necessary as an alternative.

- Asset Thresholds: Pay special attention to asset thresholds and related regulations.

Filing Deadlines & Important Dates

Timely submission is necessary to avoid penalties and align with IRS standards.

- Annual Filing Deadline: The form should be submitted on the same day as the annual tax return for foreign entities.

- Extensions: Understanding options for deadline extensions can provide additional filing time if necessary.

Penalties for Non-Compliance

Non-compliant submissions can lead to significant financial and legal repercussions.

- Fines and Interest: Failure to file or incorrect filing may result in monetary penalties.

- Increased Scrutiny: Repeated non-compliance could lead to more rigorous IRS investigations.

Digital vs. Paper Submission

Entities should choose the submission method that best aligns with their operational workflows.

- Electronic Filing: Provides efficiency, with built-in error-checking mechanisms in tax software.

- Paper Submission: Continue using the traditional submission method, with extra care given to ensuring all paperwork is correctly compiled and mailed.

By covering these critical elements of the 2014 M-2 form, corporations can navigate the complexities of international tax compliance with greater confidence and accuracy.