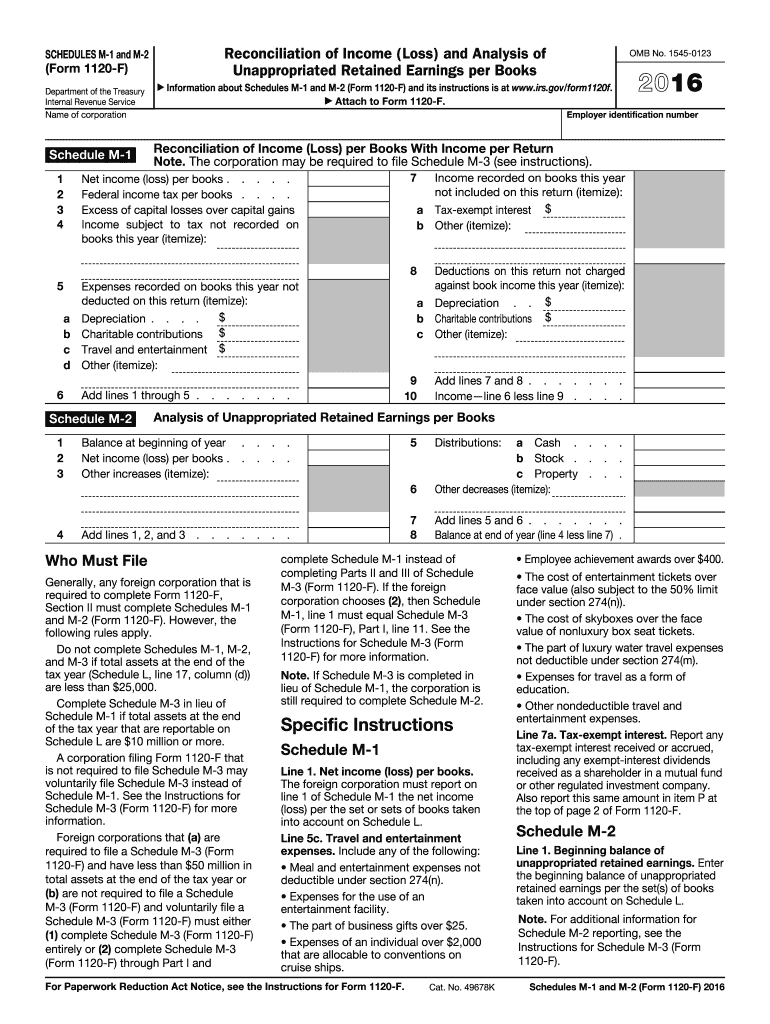

Definition & Meaning

Schedules M-1 and M-2 are essential components of Form 1120-F, specifically designed for foreign corporations to report key financial information. Schedule M-1 reconciles the income (or loss) recorded on a corporation's financial books with the income reported on its tax return. This process ensures that any discrepancies between financial accounting and tax reporting are clearly explained. In contrast, Schedule M-2 analyzes the corporation’s unappropriated retained earnings. These schedules play a crucial role in maintaining transparency and accuracy in the reporting of financial activities.

How to Use the 2016 Schedules M-1 and M-2 (Form 1120-F)

To effectively use Schedules M-1 and M-2, it's important to understand their distinct purposes and requirements:

-

Schedule M-1:

- Reconcile financial book income with tax return income.

- Address common discrepancies like nontaxable income, nondeductible expenses, and timing differences.

-

Schedule M-2:

- Review changes in retained earnings not appropriated for specific purposes.

- Analyze items affecting the retained earnings balance such as dividends and adjustments due to accounting changes.

Ensuring that these schedules accurately reflect the corporation’s financial activities is critical for compliance with IRS regulations.

Steps to Complete the 2016 Schedules M-1 and M-2 (Form 1120-F)

-

Collect Financial Statements:

- Gather comprehensive financial records, including all income and expenses recorded for the fiscal year.

-

Reconcile Income with Schedule M-1:

- Identify income items not included in the tax return.

- Specify expenses deducted on the tax return not included in financial records.

- Explain any other discrepancies between book and tax income.

-

Analyze Retained Earnings with Schedule M-2:

- Detail opening balances, additions, and subtractions from retained earnings.

- Include dividends paid out and net income retained within the corporation.

-

Review and Verify:

- Carefully check all entries for accuracy.

- Ensure that all mathematical calculations are correct and that entries align with financial documents.

Important Terms Related to the 2016 Schedules M-1 and M-2 (Form 1120-F)

- Reconciliation: The process of ensuring financial book income matches with tax return income.

- Unappropriated Retained Earnings: Profits not distributed as dividends or allocated to specific reserves.

- IRS Filing: The process of submitting the completed form to the IRS.

- Foreign Corporation: A company incorporated outside the United States but operating or earning income within U.S. borders.

Understanding these terms is crucial for accurately completing the schedules.

IRS Guidelines

The IRS provides specific instructions for completing Schedules M-1 and M-2. These guidelines outline who must file the schedules, the type of information to be included, and how to correct errors if discovered later. Following IRS guidelines is essential for avoiding penalties and ensuring all required information is accurately reported.

Legal Use of the 2016 Schedules M-1 and M-2 (Form 1120-F)

Foreign corporations are legally required to file Schedules M-1 and M-2 as part of Form 1120-F if they engage in U.S. trade or business activities. The schedules must accurately reflect the corporation’s financial activities and adhere to IRS reporting standards. Non-compliance or inaccuracies can lead to significant legal consequences and financial penalties.

Penalties for Non-Compliance

Failure to file Schedules M-1 and M-2 or providing incorrect information can result in penalties from the IRS. Common penalties include fines for late submission and other punitive charges for deliberate misinformation. Ensuring timely and accurate filings is critical to avoid these penalties.

Filing Deadlines / Important Dates

The filing deadline for Form 1120-F, including Schedules M-1 and M-2, is typically the fifteenth day of the sixth month after the end of the corporation's tax year. It is crucial to adhere to this deadline to avoid late filing penalties and to maintain compliance with IRS regulations.

Digital vs. Paper Version

Form 1120-F, along with its schedules, can be filed both digitally and on paper. While a paper submission might be preferred by some, electronic filing offers advantages like faster processing times and immediate confirmation of receipt. It is essential to choose the method that best suits the corporation’s needs and ensures compliance with IRS deadlines.