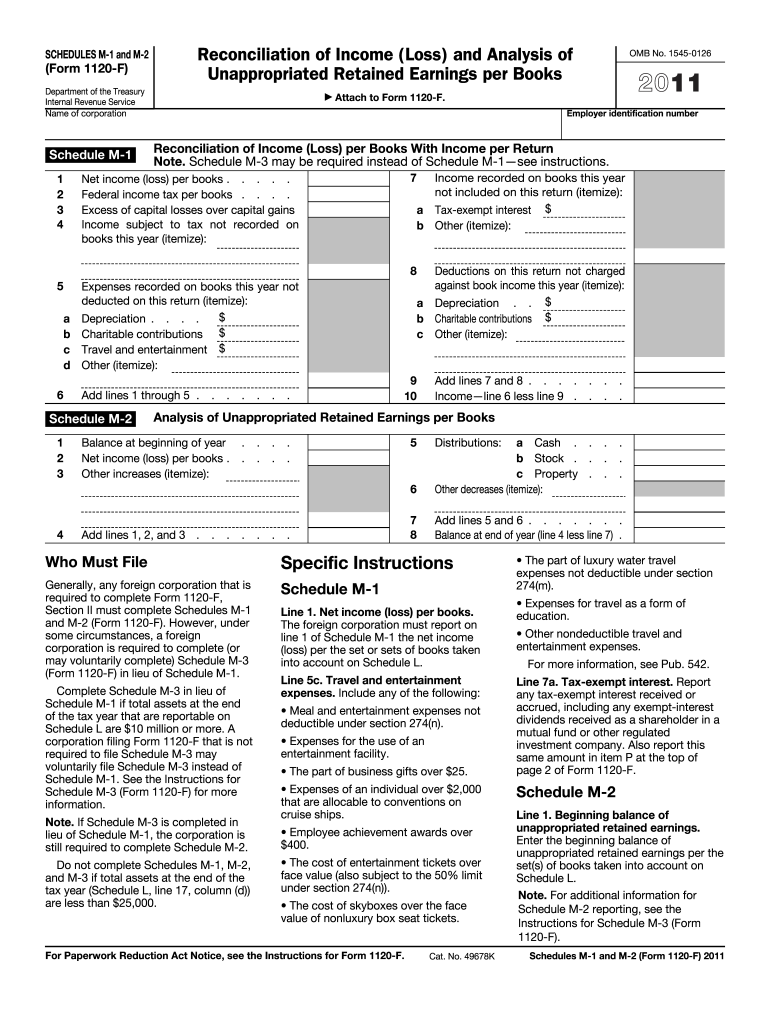

Definition and Meaning of Form 1120 M-2 2011

Form 1120 M-2, utilized during the 2011 tax year, is part of the U.S. corporate tax filing process. It specifically relates to Schedule M-2, which is used by corporations to analyze their unappropriated retained earnings. This process involves reconciling the corporation's income per books with income reported on tax returns. Understanding its role is crucial for corporations in ensuring they accurately track profits that have not been distributed as dividends but can still impact tax liabilities.

Steps to Complete Form 1120 M-2 2011

Completing Form 1120 M-2 involves several key steps.

- Gather Financial Information: Ensure access to comprehensive financial documents, including balance sheets and income statements, to correctly input unappropriated retained earnings data.

- Reconcile Income: Align the income per corporation's books with the taxable income reported on the return. This might involve adjustments for book-tax differences.

- Report Earnings: Document the unappropriated retained earnings beginning with amounts from the start of the accounting period, while accounting for adjustments throughout the fiscal year.

- Submit the Form: File the completed Form 1120, including Schedule M-2, by the stipulated IRS deadlines, ensuring to double-check all calculations and entries.

Important Terms Related to Form 1120 M-2 2011

Understanding key terminology is crucial:

- Unappropriated Retained Earnings: Profits not distributed as dividends; reflected in equity.

- Book-Tax Differences: Variations between financial accounting and tax accounting.

- Reconciliation: Process of ensuring all financial and tax records align.

IRS Guidelines for Form 1120 M-2 2011

The IRS provides specific guidance for filing Form 1120 M-2 as part of the corporate tax return. Tax preparers must adhere to instructions outlining how to adjust for book-tax differences, disclose non-deductible expenses, and report major changes in business activities that affect retained earnings. Compliance ensures accurate reporting and minimizes risk of audits.

Filing Deadlines and Important Dates

Corporations typically must file Form 1120 with Schedule M-2 by the 15th day of the third month following the end of their tax year. For most, this is March 15. Extensions may be available; however, forms must be postmarked or electronically submitted by the deadline to avoid penalties.

Penalties for Non-Compliance

Failing to file Form 1120 M-2 can result in substantial penalties. These may include fines for inaccurate reporting, late submission, or failure to file. Corporations might incur a monthly penalty calculated based on net worth and tax liability, stressing the importance of timely and accurate submissions.

Required Documents for Form 1120 M-2 2011

To complete and file Form 1120 M-2, corporations need:

- Balance Sheets: Outlining the fiscal assets and liabilities.

- Income Statements: Showing profit and loss.

- Adjusting Journal Entries: For corrections aligning book and tax records.

Who Issues Form 1120 M-2

Form 1120 M-2, part of the broader Form 1120 used for corporate tax returns, is issued by the Internal Revenue Service (IRS). It is specifically used by corporations to meet tax reconciliation requirements while providing a detailed report of their financial operations and retained earnings for federal tax purposes.