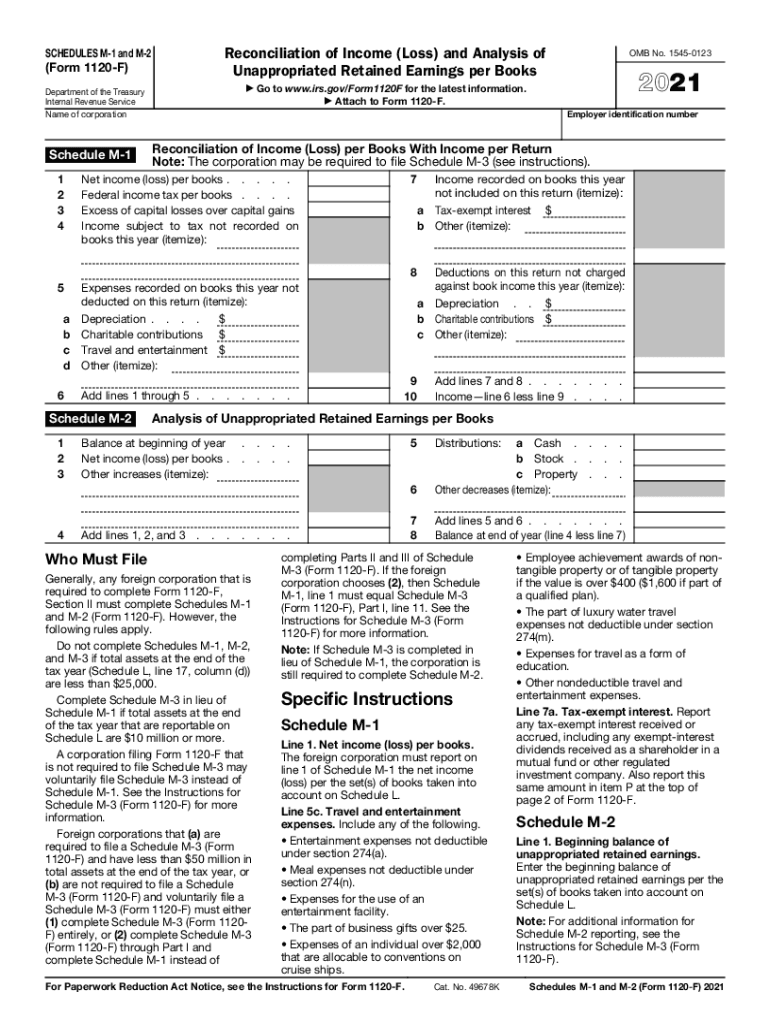

Definition and Meaning of Schedule M-2

Schedule M-2 is a vital component of the Form 1120-F, which is used by foreign corporations engaged in business within the United States. This schedule specifically focuses on analyzing unappropriated retained earnings. It examines the changes in a corporation's retained earnings during a specific tax period. By comparing beginning and ending balances, Schedule M-2 helps identify distributions, adjustments, and other transactions affecting retained earnings.

Key Aspects of Schedule M-2

- Purpose: It provides insight into the elements contributing to changes in retained earnings.

- Use Case: Corporations use it to illustrate profitability changes year over year.

- Connection to Other Forms: Complements Schedule M-1 by providing additional context for financial statement reconciliation.

Steps to Complete Schedule M-2

Completing Schedule M-2 requires attention to detail and following a structured approach. Below are the steps generally involved in completing this scheduled form:

- Gather Financial Information: Collect the necessary financial records, including balance sheets and statements showing changes to retained earnings.

- Calculate Opening Balances: Start with the retained earnings balance at the beginning of the fiscal year.

- Document Transactions: Include all transactions that impact retained earnings, such as net income, dividends, and adjustments.

- Calculate Ending Balance: Determine the closing balance of retained earnings.

Detailed Steps

-

Step 1: Prepare Documentation

Collect previous year financial records and current transactions. -

Step 2: Reconcile Changes

Review each entry to ensure changes align with corporate disclosures. -

Step 3: Verify Consistency with M-1

Ensure changes recorded on Schedule M-2 match income reconciliations on Schedule M-1.

Who Typically Uses Schedule M-2

Schedule M-2 primarily targets foreign corporations conducting business in the U.S. that need detailed earnings analyses. However, specific users include:

- Financial Analysts who assess corporate financial health.

- Corporate Accountants who prepare and file tax documents.

- Tax Consultants involved in complex tax compliance for multinational companies.

Industries Most Impacted

- Manufacturing Firms: often have complex distributions affecting retained earnings.

- Service Industries: where profit distributions frequently occur.

- Retail Corporations: with multiple subsidiaries across different jurisdictions.

Legal Use of Schedule M-2

The legal framework around Schedule M-2 ensures transparency and accountability for foreign corporations within the U.S. tax framework. It is mandated under federal law to ensure corporations accurately report their financial status.

Compliance Requirements

- Accurate Reporting: Ensure figures reflect true financial health.

- Audit Preparedness: Maintain thorough documentation for IRS reviews.

Key Elements of Schedule M-2

Schedule M-2 comprises various segments vital to understanding and documenting adjustments in retained earnings.

Major Components

- Beginning and Ending Retained Earnings: Reflect changes over the fiscal year.

- Adjustments to Retained Earnings: Include income adjustments and other transactions.

- Dividends Paid or Credited: Affecting retained earnings over the period.

IRS Guidelines for Schedule M-2

The IRS provides regulations specifying how foreign corporations should account for retained earnings, ensuring consistent documentation across entities.

Essential IRS Instructions

- Timely Filing: Schedule M-2 forms part of the annual tax return deadline, typically March 15 for calendar-year taxpayers.

- Accurate Documentation: Ensure reported figures align with supporting documentation.

Filing Deadlines and Important Dates

Filing deadlines are pivotal for compliance. Ensuring timely submission of Schedule M-2 is crucial to avoiding penalties.

- Calendar Fiscal Year Corporations: Must file by March 15, with possible extensions upon request.

- Other Fiscal Year Ends: The 15th day of the fourth month after the fiscal year-end.

Extensions

A six-month extension can often be requested by filing Form 7004.

Penalties for Non-Compliance

Corporations that do not comply with filing requirements may incur significant penalties, using Schedule M-2 incorrectly or failing to file can lead to:

- Monetary Penalties: Additional taxes and fines may apply.

- Increased Audit Risks: Non-compliance can trigger more rigorous IRS scrutiny.

- Reputational Damage: Among investors and stakeholders for financial mismanagement.

Avoiding Penalties

- Strict Adherence to Deadlines: Follow IRS timelines precisely.

- Ensuring Accuracy: Double-check all entries for mistakes or omissions.

These comprehensive details on Schedule M-2 provide the necessary framework for a thorough understanding of its purpose, compliance requirements, and associated implications for foreign corporations operating in the U.S.