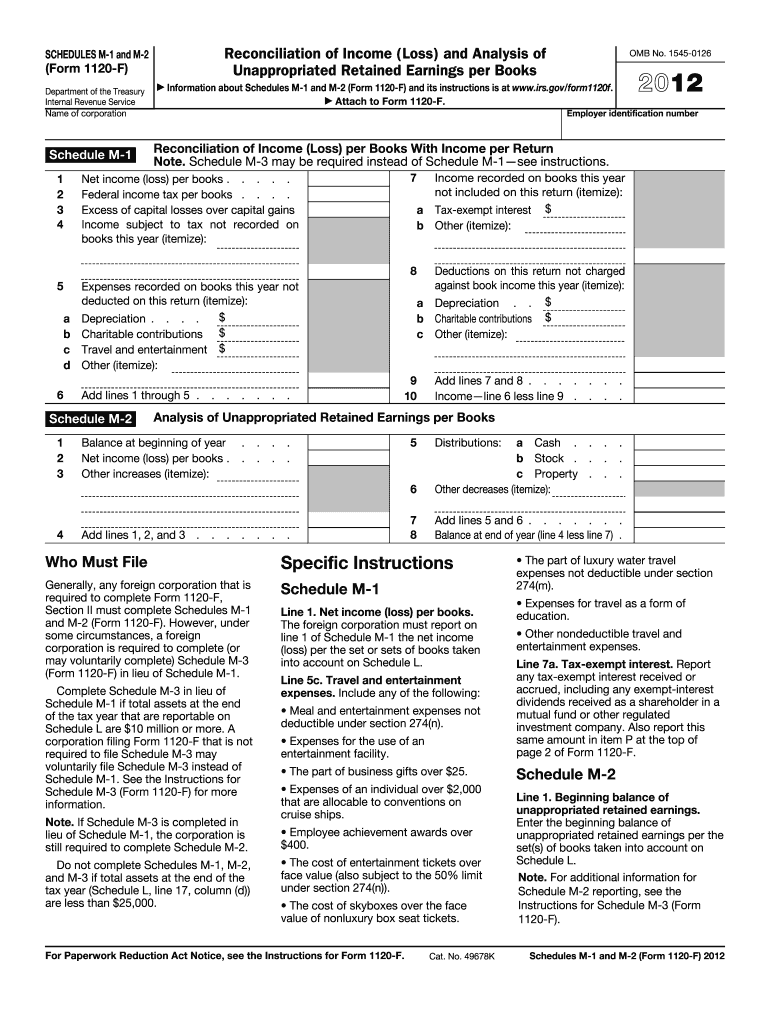

Definition and Meaning of the 2012 M-1 Form

The 2012 M-1 form serves as a crucial schedule associated with Form 1120-F, which is primarily utilized by foreign corporations conducting business within the United States. This specific form is designed to aid in reconciling differences between book income and taxable income for these foreign entities. The form ensures that all necessary financial adjustments are accurately reported to align with U.S. tax regulations. By meticulously outlining both the recorded book income and the corresponding taxable figures, the form facilitates compliance with statutory requirements in the United States.

Steps to Complete the 2012 M-1 Form

-

Preparation of Financial Statements:

- Ensure all financial statements are up-to-date and reflect accurate figures.

- These statements form the basis for completing the M-1 schedule, providing a clear starting point for reconciliation.

-

Reconciliation of Book to Tax Income:

- Identify all book income discrepancies when compared to taxable income.

- Adjustments should be clearly documented for deductions and income not recorded on books as per IRS rules.

-

Completion of Specific Income Adjustments:

- Document all tax adjustments, including permanent differences like non-taxable income.

- Ensure accuracy in reporting to prevent discrepancies during IRS evaluations.

-

Verification and Submission:

- Double-check all entries for accuracy and consistency.

- Submit the completed M-1 form along with Form 1120-F by the specified tax deadline.

Who Typically Uses the 2012 M-1 Form

The 2012 M-1 form is specifically directed towards foreign corporations that have a presence or engage in business activities within the United States. This includes entities that have established a U.S. branch, execute transactions that result in U.S.-sourced income, or otherwise fulfill obligations under U.S. tax law. By reconciling book and tax income, these corporations ensure compliance with the IRS and avert potential penalties associated with inaccurate reporting.

Key Elements of the 2012 M-1 Form

- Documentation of Book Income: Clearly outlines the reported book income for the fiscal period.

- Reconciliation Adjustments: Details the various adjustments made to convert book income into taxable income.

- Reconciliation Entries: Captures specific transactional discrepancies such as non-deductible expenses or non-taxable income.

- Income and Deduction Reconciliations: Summarizes the differences between financial records and tax reporting requirements.

IRS Guidelines for the 2012 M-1 Form

The Internal Revenue Service (IRS) provides specific guidance for completing the 2012 M-1 form to ensure proper compliance:

- Follow all declared timelines and submission processes to avoid late penalties.

- Maintain thorough records of all income and adjustments reported on the form.

- Ensure consistency with generally accepted accounting principles (GAAP) when applicable for financial records.

Filing Deadlines and Important Dates

The M-1 form must be submitted in conjunction with the corporation's 1120-F filing. Generally, the deadline for filing tax returns for corporations, including the M-1 form, falls on the fifteenth day of the fourth month following the end of the corporation’s fiscal year, unless an extension is granted. Timely submission is essential to avoid late filing penalties.

Required Documents for Completing the 2012 M-1 Form

To accurately complete the 2012 M-1 form, the following documentation is typically required:

- Comprehensive financial statements for the applicable tax year.

- Detailed accounting records illustrating all book-to-tax adjustments.

- Previous tax filings for cross-reference and consistency checks.

Software Compatibility with the 2012 M-1 Form

For the convenience of tax filing, the 2012 M-1 form is compatible with various tax preparation software systems, enhancing ease of use and accuracy in reporting. Programs like TurboTax and QuickBooks offer functionality to assist users in inputting the requisite information and automating calculations where feasible. Selecting appropriate software can streamline the filing process by validating entries and ensuring adherence to IRS guidelines.

Penalties for Non-Compliance with the 2012 M-1 Form

Failure to accurately complete and submit the M-1 form in accordance with IRS regulations can result in significant penalties for foreign corporations. These can include monetary fines and additional scrutiny from tax authorities. Therefore, it is crucial for entities to review and understand the requirements thoroughly or consult tax professionals specializing in U.S. corporate taxes to mitigate risks associated with non-compliance.