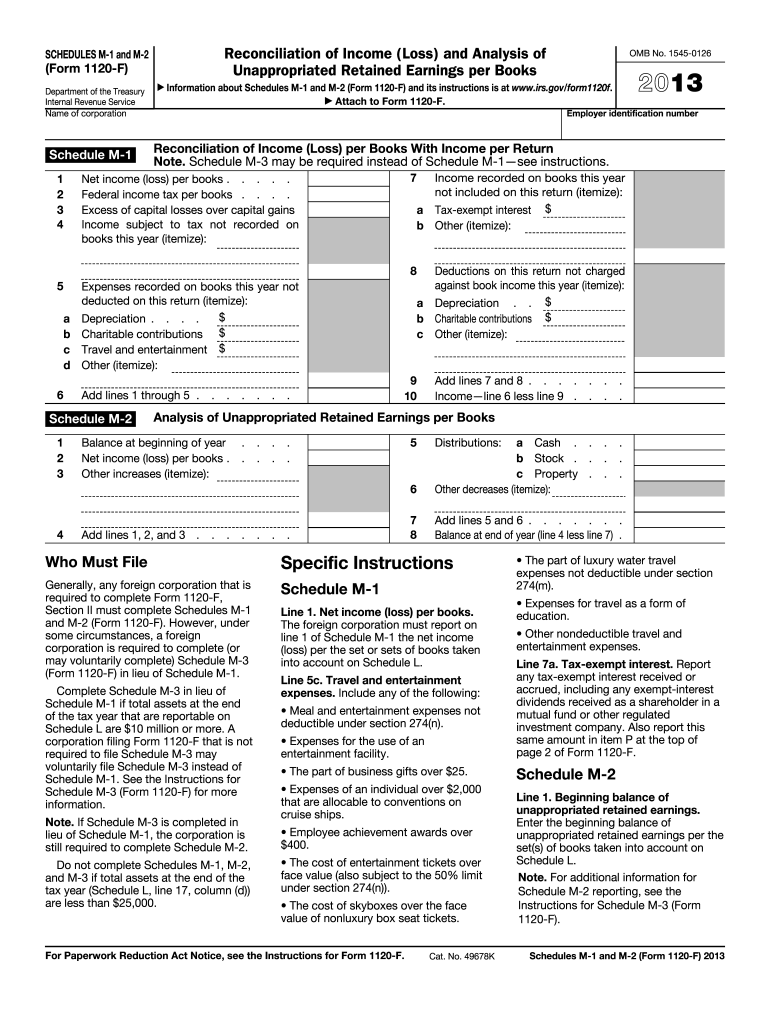

Definition and Meaning of the 2013 M-2 Form

The 2013 M-2 form is a component of the IRS Form 1120-F, required for foreign corporations to reconcile book income with taxable income and to analyze unappropriated retained earnings. It provides a detailed breakdown of undistributed income after accounting for taxes and deductions. The form aims to ensure transparency and compliance with U.S. tax regulations for foreign corporations doing business in the United States. By understanding the specific details required in Schedule M-2, businesses can accurately report financial data to the IRS.

Steps to Complete the 2013 M-2 Form

- Gather Financial Statements: Collect the company's comprehensive financial statements, including balance sheets, income statements, and retained earnings reports.

- Calculate Unappropriated Retained Earnings: Start with the beginning balance of unappropriated retained earnings, add net income, and subtract any dividends and distributions.

- Adjust for Income and Deductions: Incorporate adjustments for book-tax differences using details from Schedule M-1.

- Review for Accuracy: Ensure all numbers align with reported figures on Form 1120-F.

- Submit with Form 1120-F: Attach the completed Schedule M-2 to the corporate tax return.

Important Terms Related to the 2013 M-2 Form

- Unappropriated Retained Earnings: Profits that have not been allocated for paying dividends.

- Book Income vs. Taxable Income: Financial income reported on statements versus income subject to taxation.

- Schedule M-1: A related form that details adjustments for income and deductions.

- Form 1120-F: The U.S. Income Tax Return form specifically for foreign corporations.

IRS Guidelines for the 2013 M-2 Form

The IRS mandates that foreign corporations use Schedule M-2 to reconcile financial and taxable income accurately. The form requires corporations to itemize changes in retained earnings, ensuring they match income reported on other schedules. Businesses should refer to IRS Publication 542 for more detailed instructions on corporate taxation and compliance.

Who Issues the 2013 M-2 Form

The Internal Revenue Service (IRS) issues the 2013 M-2 form. As part of Form 1120-F, it is integral for foreign corporations operating in the U.S. to file their tax returns. It is accessed primarily through IRS publications and tax preparation software recognized by the IRS.

Examples of Using the 2013 M-2 Form

- Foreign Subsidiary of a Multinational Corporation: A company with global operations uses the form to report U.S. income and expenses.

- Bi-national Partnership Countries: These entities utilize the form to declare U.S.-sourced income and ensure tax compliance.

- U.S.-based Branch of a Foreign Corporation: U.S. subsidiaries file the form to reconcile income differences between U.S. books and foreign tax records.

Filing Deadlines and Important Dates for the 2013 M-2 Form

The typical deadline for filing Form 1120-F, and thus the M-2 form, is the 15th day of the fourth month after the fiscal year ends. However, extensions may be available. For example, if a corporation operates on a calendar year, the due date would be April 15.

Penalties for Non-Compliance with the 2013 M-2 Form

Failing to file the 2013 M-2 form accurately and on time can result in penalties, including fines and interest on unpaid taxes. The IRS may impose penalties for understating income and inaccurately reporting retained earnings, emphasizing the need for accuracy and completeness when submitting tax documents.