Definition and Purpose of the 2015 Form 1120-F

The 2015 Form 1120-F, known as the U.S. Income Tax Return of a Foreign Corporation, is primarily utilized by foreign corporations to report their income, deductions, and tax liability to the Internal Revenue Service (IRS). The form is essential for businesses with income effectively connected to a trade or business in the United States. This document helps ensure compliance with U.S. tax laws and accurately reflects a corporation's financial activities within the country.

Understanding the Distinction

Foreign corporations must distinguish between income that is effectively connected to their U.S. operations and income that is not. The effectively connected income (ECI) is subject to U.S. taxation and must be reported on Form 1120-F. Income not considered ECI is generally not taxed unless specific provisions apply.

How to Obtain the 2015 Form 1120-F

Foreign corporations can acquire Form 1120-F through several methods to ensure they meet filing requirements. The IRS provides access via its official website, where corporations can download the form directly.

Alternative Acquisition Methods

- IRS Offices: Corporations can also visit local IRS offices to obtain physical copies.

- Tax Software: Some tax preparation software, such as TurboTax and QuickBooks, also offer downloadable versions of the form.

Instructions for Completing the 2015 Form 1120-F

Completing the Form 1120-F requires attention to detail, ensuring all financial data is accurately reported. The following steps outline the process:

- Enter Basic Information: Begin with entering the corporation's name, address, and Employer Identification Number (EIN).

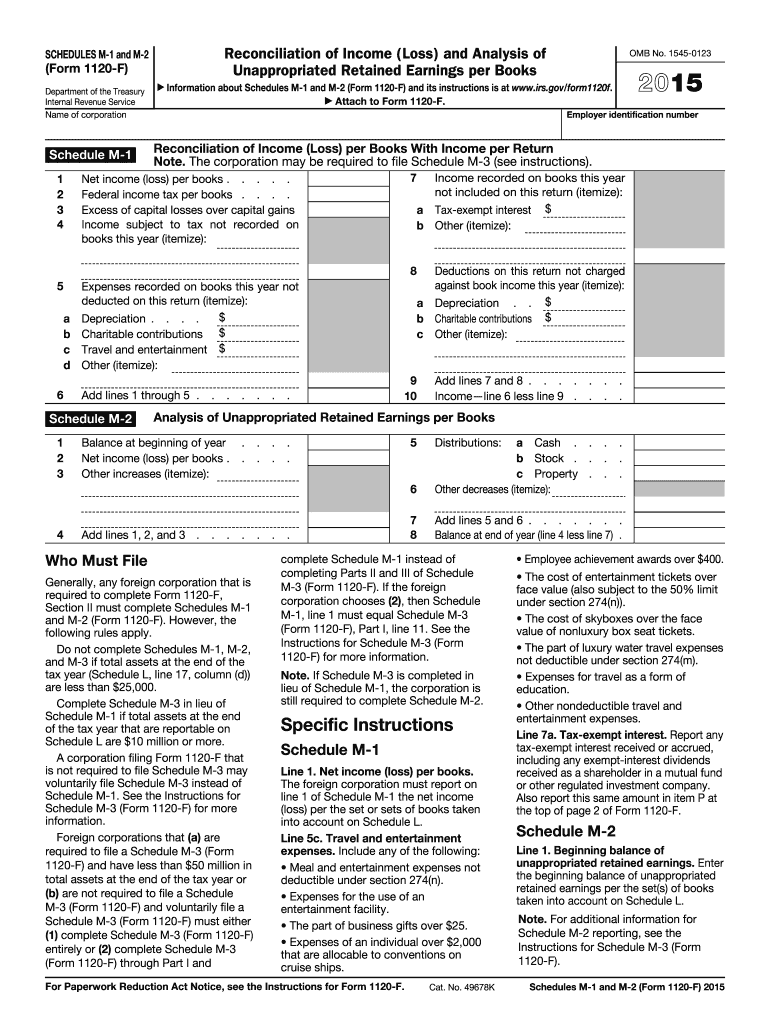

- Schedule M-1 and M-2: These schedules help reconcile book income with income reported on tax returns and analyze retained earnings.

- Determine Taxable Income: Include all effectively connected income, deductions, and other relevant financial data.

- Calculate Tax Liability: Use applicable U.S. corporate tax rates to determine the total tax owed.

Detailed Reporting

- Deductions: Deduct expenses related to ECI such as business travel, office supplies, and wages.

- Credits: If applicable, account for available credits that can reduce tax liability.

Eligibility for Filing the 2015 Form 1120-F

Form 1120-F applies to foreign corporations engaged in a trade or business within the United States. Eligibility is determined by the following criteria:

- Business Operations: Must have substantial business activities in the U.S.

- Income Requirement: Must have ECI within the U.S.

Exemptions and Special Cases

Certain foreign corporations may be exempt from filing if they engage in limited or no business activities within the U.S. It is important to consult IRS guidelines to understand these exemptions.

Key Elements of Form 1120-F

Several essential components make up Form 1120-F, each requiring careful attention:

- Schedule M-1: Reconciles book income with U.S. taxable income.

- Schedule M-2: Analyzes unappropriated retained earnings.

- Income Statement: Details income from all U.S. sources.

- Deductions: Allows subtraction of eligible business expenses.

Importance of Accurate Data

Precision in reporting ensures compliance and minimizes the risk of penalties. Corporations should maintain accurate bookkeeping throughout the fiscal year.

Penalties for Non-Compliance

Failing to file Form 1120-F or providing incorrect information may result in significant penalties imposed by the IRS. These include:

- Filing Penalties: Up to $10,000 or more for failing to file on time.

- Accuracy-Related Penalties: Additional penalties for underreporting income or providing inaccurate information.

Mitigation Strategies

Corporations should consider preparatory reviews or consulting tax professionals to ensure the form is completed correctly and submitted on time.

IRS Guidelines for the 2015 Form 1120-F

The IRS provides comprehensive guidelines to assist foreign corporations in preparing and filing Form 1120-F. These include specific instructions for:

- Filling out each section of the form accurately

- Identifying deductible expenses vs. non-deductible expenses

- Understanding obligations for paying estimated taxes

Utilizing IRS Resources

Corporations are encouraged to use IRS resources, such as the official instructions manual for Form 1120-F, to navigate any complex areas or seek clarification on unique scenarios.

Filing Deadlines for Form 1120-F

The filing deadline for Form 1120-F is typically the 15th day of the 6th month following the end of the corporation's tax year. For calendar year filers, this generally means a June 15th deadline.

Requests for Extensions

Corporations may file for an automatic extension by submitting Form 7004. This extension provides an additional six months to file but does not extend the time to pay any taxes due.

Business Entity Types Suited for Form 1120-F

Form 1120-F caters to various foreign business structures conducting U.S. activities, including:

- LLC: When classified as a corporation for tax purposes

- Corporation: Both C Corporations and other structures with similar tax obligations

Specific Considerations

Each entity type might have unique filing requirements or tax implications, emphasizing the need to determine proper classification and associated obligations before filing.

State-Specific Rules for Form 1120-F

While Form 1120-F addresses federal tax obligations, foreign corporations should also be aware of state-specific tax rules. States may impose their filing requirements or tax obligations on income within their jurisdictions.

Examples of State Variations

Some states might require additional forms or have different nexus thresholds, affecting which corporations must file and pay state taxes. Consulting with state tax authorities can aid in understanding these requirements.