Definition and Meaning of Form 1120-REIT

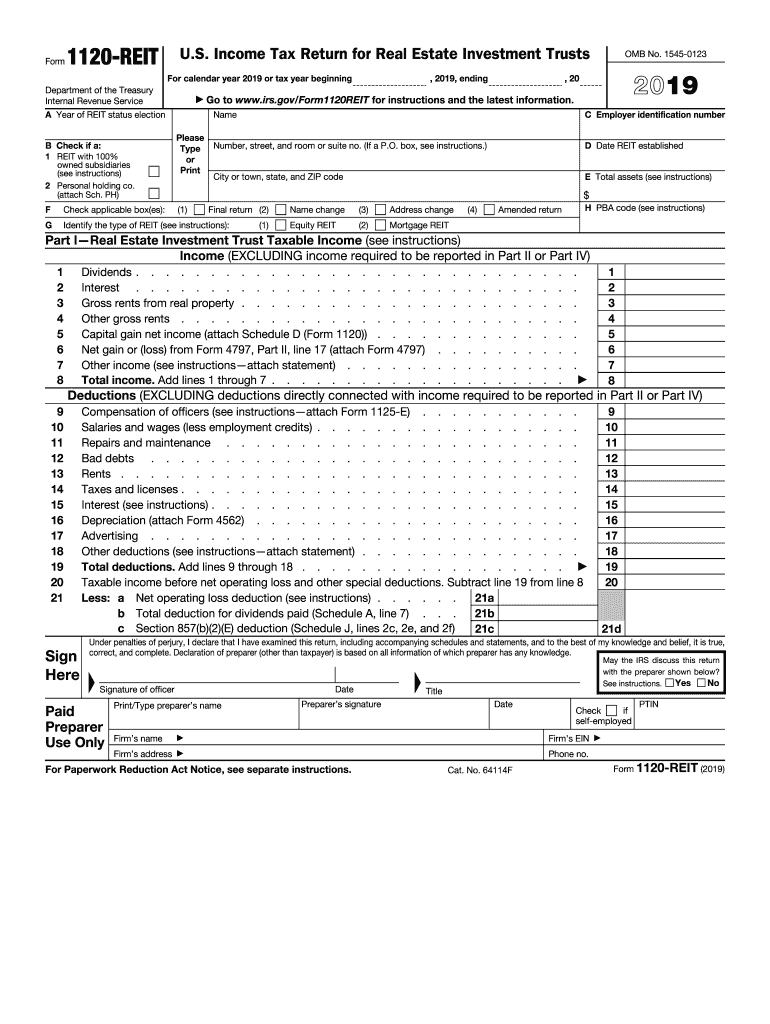

Form 1120-REIT is the U.S. Income Tax Return specifically designated for Real Estate Investment Trusts (REITs). This form is critical for REITs as it facilitates the process of reporting income, deductions, and taxes owed. Different from standard corporate tax forms, Form 1120-REIT addresses unique elements associated with real estate investments, ensuring compliance with IRS regulations.

REITs are required to distribute at least 90% of taxable income to shareholders, which affects how income and dividends are reported on this form. Certain schedules within the form address taxable income from foreclosure properties and prohibited transactions, adding layers of complexity to the filing process. Understanding these nuances is crucial for precise reporting and compliance.

Steps to Complete Form 1120-REIT

-

Gather Required Documents: Collect financial statements, records of dividends paid, and details of any taxable foreclosure property transactions.

-

Fill Out Basic Information: Enter the REIT’s name, address, and employer identification number (EIN) in the initial sections of the form.

-

Report Income and Deductions: Accurately report income sources and permissible deductions specific to REIT operations. Ensure that calculations adhere to IRS guidelines to prevent discrepancies.

-

Calculate Tax Liability: Utilize included worksheets to determine tax owed, factoring in applicable credits and unique deductions available to REITs.

-

Attach Supplemental Schedules: Provide necessary supporting documentation, such as Schedule A for dividends received and other relevant schedules that support the financials presented.

-

Review and Submit: Double-check for completeness and accuracy before submission. Submit the form through designated IRS channels, either online or via mail.

Completing Form 1120-REIT requires a detailed approach due to its complexity and the specific requirements related to real estate investments.

Key Elements of Form 1120-REIT

-

Income Reporting: Includes sections for declaring various income types, such as rental income, interest, and capital gains specific to real estate transactions.

-

Dividend Distribution: Detailed instructions for listing dividends paid to shareholders; essential due to the requirement for REITs to distribute a majority of taxable income.

-

Schedules for Special Transactions: Covers special circumstances such as income from foreclosure and non-permissible transactions, with dedicated sections requiring meticulous reporting.

These elements are vital for ensuring compliance with tax regulations and complete financial transparency.

IRS Guidelines for Form 1120-REIT

REITs must adhere to IRS guidelines when filing Form 1120-REIT, which includes specific instructions on how income and deductions must be reported. There are strict regulations concerning what qualifies as permissible deductions and income due to the unique nature of real estate investments.

Moreover, the IRS requires that REITs maintain certain standards for record-keeping and documentation to substantiate claims made within the form. Adherence to these guidelines helps prevent penalties and ensures the tax reality of the REIT is accurately represented.

Filing Deadlines and Important Dates

Real Estate Investment Trusts must file Form 1120-REIT by the 15th day of the third month following the end of the taxable year. For companies operating under a calendar year cycle, this typically means a due date of March 15th. Extensions may be available but must be formally requested through the proper channels.

These timely submissions are critical; failure to meet deadlines could result in significant penalties and interest charges, which could affect the financial health and operations of the REIT.

Eligibility Criteria for Using Form 1120-REIT

REITs, by definition, must meet specific eligibility criteria, such as having at least 75% of its assets in real estate and earning 75% of its income from real estate-related sources. These criteria influence eligibility for using the 1120-REIT form. The trust structure must also allow for pass-through of income to shareholders, meaning tax obligations are met at the individual investor level rather than the corporate level.

Understanding these eligibility requirements ensures that an entity rightfully qualifies as a REIT and appropriately utilizes the designated tax form.

Penalties for Non-Compliance

Non-compliance with Form 1120-REIT's requirements can result in significant penalties. This includes failing to file on time, discrepancies in reported earnings and actual income, or underpayment of taxes due. The IRS enforces penalties that can financially strain a REIT, affecting its investor relations and market credibility.

Thus, it is imperative that REITs maintain rigorous internal controls and financial reporting systems to ensure compliance and avoid these costly repercussions.

Digital vs. Paper Version of Form 1120-REIT

The IRS facilitates different methods of submitting Form 1120-REIT, including electronic and paper submissions. Digital filing is encouraged due to its efficiency, reduced processing times, and lower potential for errors through integrated checks within e-filing systems.

However, some entities may choose traditional paper submissions, depending on their internal processing capabilities. Each method has its advantages, but digital submissions align with modern trends towards streamlined and automated compliance processes.