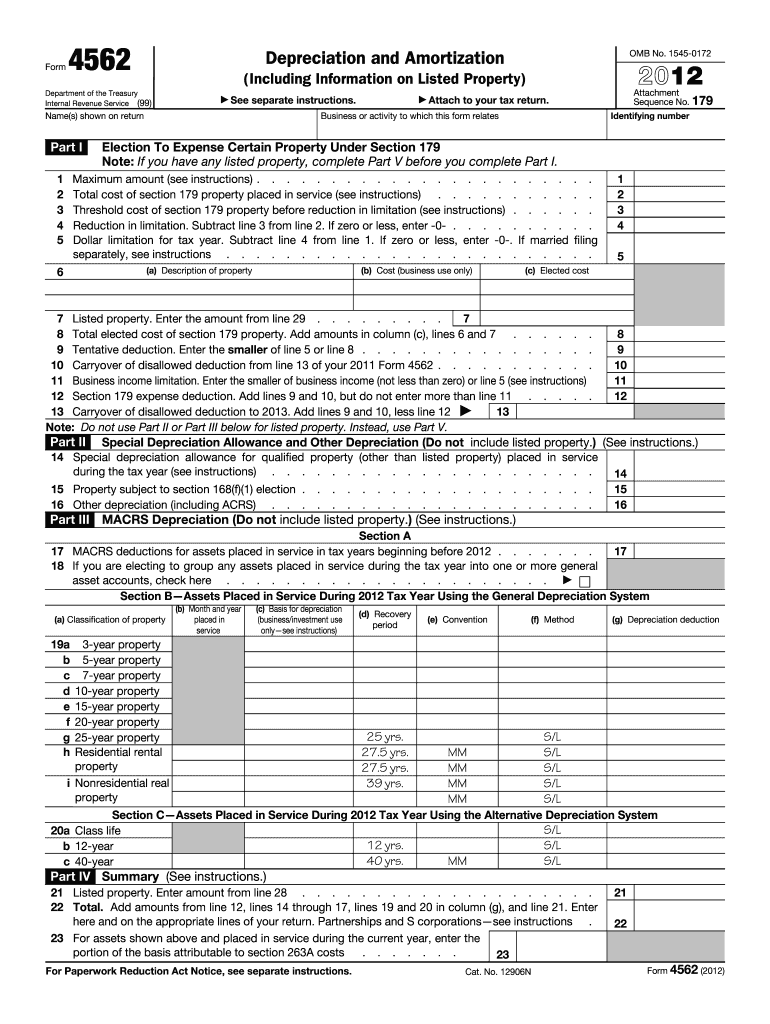

Definition & Purpose of the 2012 Form 4562

Form 4562, for the year 2012, is primarily used for reporting taxpayer deductions related to depreciation and amortization. This form allows individuals and businesses to deduct the cost of depreciable business assets over time. It includes provisions for electing to expense certain property under Section 179 and outlines the processes for claiming special depreciation allowances and Modified Accelerated Cost Recovery System (MACRS) deductions.

Key Components

- Section 179 Investment: Taxpayers can choose to expense up to a certain limit on qualifying property, providing an immediate deduction instead of spreading it over several years.

- Special Depreciation Allowance: Allows for accelerated depreciation on specific property types.

- MACRS Depreciation: A critical component that provides guidelines for calculating depreciation expenses over time.

Who Typically Uses the 2012 Form 4562

The 2012 Form 4562 is generally utilized by businesses and individuals who own tangible property used in a trade or business. This includes:

- Small Businesses and Corporations: Companies leveraging large amounts of equipment purchases.

- Sole Proprietors: Self-employed individuals who need to report depreciation on business assets.

- Partnerships and LLCs: Entities can optimize asset depreciation through strategic financial planning.

How to Obtain the 2012 Form 4562

There are several ways to access the 2012 Form 4562:

- IRS Website: Direct download from the official IRS website.

- Tax Software Integration: Utilize platforms like TurboTax or QuickBooks to obtain and fill out the form digitally.

- Professional Assistance: Accountants or tax professionals often have access to archived forms and can provide guidance in obtaining and filling out the form.

Steps to Complete the 2012 Form 4562

Completing the form requires precise financial documentation and an understanding of tax regulations:

- Gather Required Documentation: Collect purchase receipts, asset descriptions, and business use percentages.

- Determine Depreciable Property: Identify which assets qualify for depreciation under IRS rules.

- Calculate Section 179 Deduction: Elect to expense part of asset costs immediately, within IRS limits.

- Apply Special Depreciation Allowances: Utilize any applicable accelerated depreciation options.

- Enter MACRS Deductions: Calculate and document standard depreciation using MACRS tables.

Detailed Breakdown

- Section A: Has entries for electing Section 179 deductions.

- Section B: Involves special depreciation allowances.

- Section C and beyond: Covers asset classification and MACRS deductions.

IRS Guidelines on the 2012 Form 4562

Understanding the IRS's expectations for form submission can significantly impact the accuracy of your tax filings. The IRS provides strict guidelines regarding:

- Eligibility and Asset Types: Specific criteria for asset depreciation.

- Documentation: Detailed records showing business use and asset acquisition.

- Filing Accuracy: All information must be complete and accurate to avoid penalties.

Examples of Using the 2012 Form 4562

Business Equipment

A small business purchases $50,000 worth of machinery. By using Form 4562, they can depreciate these costs over the machinery's useful life, reducing taxable income each year.

Practical Application

- Immediate Deduction: Use Section 179 to deduct a significant portion in the first year.

- Standard Depreciation: Employ MACRS to spread the remaining cost over subsequent years.

Important Terms Related to the 2012 Form 4562

Familiarity with key terms can greatly aid in form comprehension:

- Depreciation: Reduction in asset value over time, recognized for tax benefits.

- Amortization: Similar to depreciation but generally for intangible assets.

- Qualified Property: Assets meeting specific IRS criteria for depreciation or expensing.

Penalties for Non-Compliance

Failure to accurately complete and submit the 2012 Form 4562 can result in penalties, including:

- Interest Charges: Accumulate on any unpaid taxes resulting from incorrect filings.

- Fines: Imposed for late submission or misinformation.

- Audit Risks: Increased risk of IRS audit if discrepancies are found.