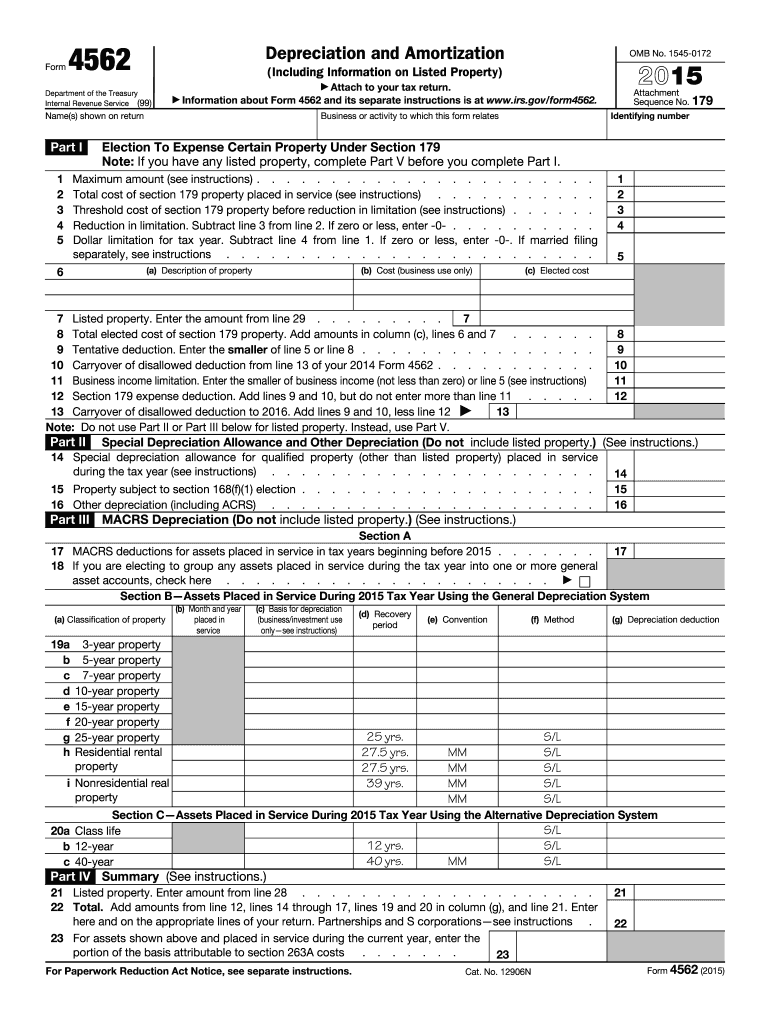

Definition & Purpose of Form 4562

Form 4562, also known as the Depreciation and Amortization form, is employed by businesses to report depreciation on assets and amortization of intangibles for tax purposes. This form allows businesses to deduct a portion of the cost of tangible property like buildings and machinery over several years. It is particularly pivotal for businesses making an election under Section 179 to expense certain properties, thus affecting their taxable income.

Detailed Sections in Form 4562

- Section 179 Election: Designed for small businesses, this section permits taxpayers to elect to deduct the cost of certain types of property as an expense when it is placed in service.

- Depreciation of Listed Property: This area addresses vehicles and other property with personal and business use. Specific rules and documentation requirements apply.

- Special Depreciation Allowance: Newly acquired assets may qualify for a special depreciation allowance in their first year of service. This rule aims to stimulate economic activity by encouraging investment in new assets.

How to Use the 2015 Form 4562

Completing the 2015 Form 4562 involves calculating deductions for the depreciation of assets placed into service during the tax year. Businesses need to list each property item, including its description, date placed in service, and cost. Calculations from this form directly reduce taxable income, reflecting the economic useful life of business assets.

Step-by-Step Process

- Identify Eligible Assets: Assess which assets qualify for depreciation or amortization deductions.

- Gather Documentation: Collect invoices, receipts, and other necessary documents that establish the purchase and service dates of each asset.

- Calculate Depreciation: Utilize IRS guidelines to compute the allowable depreciation for each asset.

- Complete Each Part of the Form: Follow the form's sequence, ensuring that each section is accurately filled out, such as Section 179 for immediate expensing and special allowances for new acquisitions.

Key Elements of the 2015 Form 4562

Form 4562 is structured to ensure taxpayers provide comprehensive details about depreciable property. It is divided into several critical components:

- General Information: Tax year and basic taxpayer details.

- Listed Property Computations: Detailed logging of properties like automobiles used for personal and business matters, subject to strict substantiation requirements.

- Summary & Totals: Concluding sections summarize deductions and transfer totals to relevant fields on primary tax returns.

Practical Examples

- Office Equipment: A business purchasing new computers can leverage the Section 179 election to expense these items immediately.

- Company Vehicles: Businesses must allocate personal versus business use and apply proportional depreciation accordingly.

Who Typically Uses the 2015 Form 4562

Form 4562 primarily serves businesses of various sizes, from sole proprietors to large corporations, seeking to report depreciation for newly acquired assets. Individuals part of partnerships or managing certain types of trusts and estates also engage with this form.

Business Entity Considerations

- Corporations and LLCs: Often dealing in large volumes of depreciable assets, requiring careful management of depreciation schedules.

- Partnerships: Allocating depreciation deductions among partners as stipulated in partnership agreements.

IRS Guidelines

The IRS issues precise guidelines on the application of Form 4562, emphasizing compliance and accuracy in reporting depreciation:

- Asset Reporting: Requirement to list each asset and track its depreciation schedule distinctively.

- Depreciation Methods: Businesses must choose from approved methods such as straight-line or declining balance, dictated by the asset’s specific circumstances and business needs.

Compliance Example

- Depreciation Records: Maintaining accurate and comprehensive records substantially aids in IRS audits and ensures no overstatement of expenses.

Filing Deadlines and Important Dates

The deadline for filing Form 4562 coincides with the business's annual tax return due date. Businesses are encouraged to integrate this form's completion into their year-end tax strategies to optimize deduction benefits.

Critical Timing Elements

- End of Tax Year Assessment: Businesses should review asset acquisitions and service entries before the tax year's close to fully capture eligible deductions.

- Amendment Periods: Familiarity with periods for amending returns if inaccuracies are discovered post-filing.

Important Terms Related to Form 4562

Understanding critical terminology is vital for leveraging Form 4562 efficiently.

Essential Terms

- Amortization: Refers to the gradual write-off of an intangible asset over its useful life.

- Listed Property: Includes assets like vehicles used for both business and personal purposes, necessitating nuanced accounting.

- MACRS: The Modified Accelerated Cost Recovery System is the predominant method for computing depreciation deductions.

Legal Use of the 2015 Form 4562

Recognizing the significant impact Form 4562 has on taxable income, businesses and practitioners must ensure its legal and ethical application. Accurate reporting on this form upholds the integrity of financial declarations and secures fair tax liabilities.

Ethical Considerations

- Accuracy in Reporting: Diligent record-keeping supports the veracity of reported depreciation and amortization amounts.

Comprehensively addressing these aspects of the 2015 Form 4562 equips users with the knowledge to manage their depreciation and amortization reporting reliably and encourages adherence to best practices.