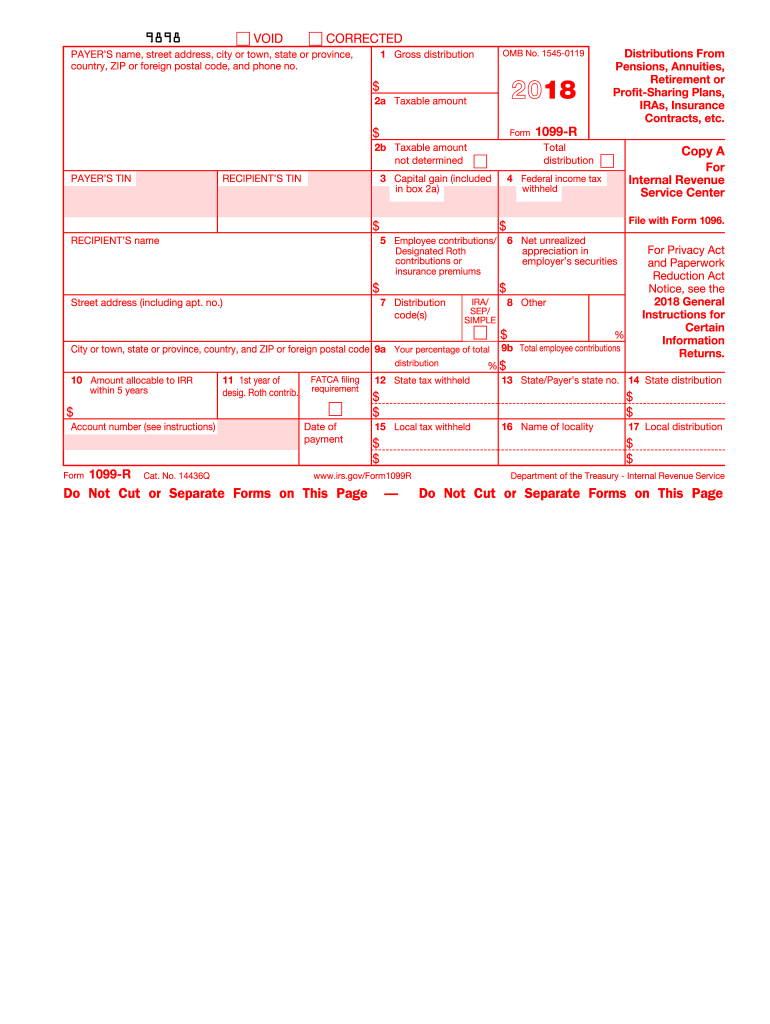

Definition & Purpose of the 2-R Blank

The 2-R blank form is used to report distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, insurance contracts, and other similar sources. This form is essential for taxpayers and financial institutions in tracking and reporting income that may be subject to federal income tax. Specifically, it helps document how much was distributed to recipients, whether any part of it is taxable, and if any taxes were withheld from the distribution. Proper completion of this form ensures compliance with IRS regulations and accurate compensation reporting for income tax purposes.

How to Use the 2-R Blank

Utilizing the 2-R blank form involves several precise steps to ensure accurate reporting. The issuer of the 1099-R, typically a financial institution or retirement plan manager, must first enter the payer and recipient's identification details, including names, addresses, and taxpayer identification numbers. Next, they must report the gross distribution amount, any taxable amount, federal income tax withheld, and any other pertinent financial details such as capital gains or distributions. Carefully review each section for accuracy to avoid penalties or delays with the IRS. It is crucial that both issuers and recipients retain copies for their records, as this form will impact both parties' financial reporting obligations.

Steps to Complete the 2-R Blank

- Identify Payer and Recipient Information: Fill in the payer's name, address, and taxpayer identification number. Similarly, enter the recipient's details to ensure clear identification between both parties.

- Input Distribution Details: Record the gross distribution amount in Box 1. Determine the taxable amount (if applicable) and report this in Box 2a while also noting any federal tax withholdings in Box 4.

- Complete Additional Fields: If applicable, include state or local payment information and any other supplemental data required by the specific distribution type.

- Review for Accuracy: Double-check all entered information for compliance with IRS requirements to minimize errors.

- Distribute Copies and Submit: Send copies B, C, and others to the appropriate parties (e.g., recipients, filing with federal or state agencies as necessary).

Key Elements of the 2-R Blank

The 1099-R form contains several critical sections that need careful attention:

- Payer's Details: Critical for IRS tracking, ensuring accurate correspondence and accountability.

- Recipient's Information: Ensures accurate identification for tax purposes.

- Distribution Amounts: Reports the total distribution and distinguishes between taxable amounts, tax withholdings, and other relevant financial data.

- IRS Codes: Used to indicate specifics about the distribution, such as early withdrawal penalties or direct rollovers.

Legal Use and Compliance of the 2-R Blank

The legal use of the 2-R involves strict adherence to IRS regulations concerning information reporting. Issuers are required by law to provide correct financial details no later than January 31 following the reporting year. Compliance requires accurately categorizing distributions and knowing the correct IRS distribution codes that apply to each payout. Failure to comply with these requirements can result in penalties for both payers and the recipients for underreporting income.

Who Typically Uses the 2-R Blank

This form is predominantly utilized by financial institutions, insurance companies, retirement plan administrators, and any entities that manage or distribute retirement benefits. The recipients typically include retirees, beneficiaries of retirement plan distributions, and other individuals withdrawing from their retirement savings plans. Similarly, finance professionals, accountants, and tax preparers regularly interact with this form during the tax filing season to ensure their clients' income is accurately reported.

Filing Deadlines and Important Dates

For the 2-R blank, issuers needed to ensure that completed forms were sent to recipients by January 31, 2014, and filed with the IRS by February 28, 2014, for paper submissions, or April 1, 2014, for electronic filings. Adhering to these deadlines is crucial to avoid late filing penalties and ensure that recipients have enough time to incorporate the information into their tax returns, which are due by April 15. It's important to keep these timelines in mind for compliance and to avoid any fines.

IRS Guidelines for the 2-R Blank

The IRS provides numerous guidelines to assist with the proper completion and filing of the 1099-R form. This includes clear instructions on how to determine the taxable portion of distributions, appropriate codes for various situations, and the specifics of federal and state withholding requirements. The guidelines also emphasize the necessity of using the official IRS printed version of Copy A when filing with the IRS directly. Other copies may be printed from electronic sources for issuing to recipients. Familiarity with these guidelines is critical for accurate reporting and helps mitigate any risks associated with non-compliance.