Definition and Purpose of Form 1099-R

Form 1099-R is an important tax document used in the United States to report distributions from pensions, annuities, retirement plans, IRAs, and similar sources. This form is crucial for both the payers and recipients of such income distributions as it outlines the taxable amount that must be reported on their yearly tax returns. Issued primarily by financial institutions, insurers, or retirement plan custodians, the 2014 Form 1099-R captures specific details on the type of distribution and its tax implications, ensuring that recipients accurately reflect their income from these sources.

How to Obtain the 2014 Form 1099-R

Individuals can obtain the 2014 Form 1099-R typically through the entity disbursing the retirement-related funds. Most institutions send this document by January 31 of the year following the tax year in question. In case of a non-receipt scenario, individuals should reach out directly to their financial institution or retirement plan administrator to request a copy. The IRS also provides downloadable PDFs of their official forms on their website, although these versions should not be filed directly due to non-scannability concerns.

Steps to Complete the 2014 Form 1099-R

- Verify Personal Information: Ensure the accuracy of the recipient's name, address, and taxpayer identification number.

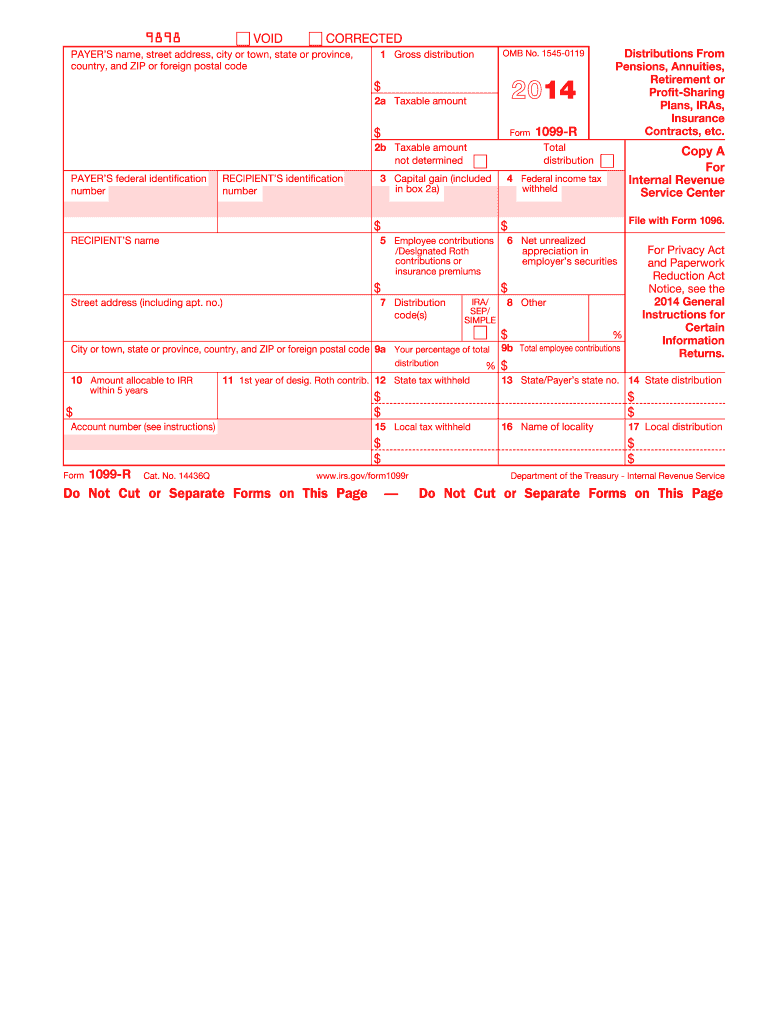

- Review Distribution Amounts: Check Box 1 for total distribution amounts and Box 2a for the taxable portion.

- Distribution Codes: Familiarize yourself with IRS distribution codes in Box 7, which explain the nature of the distribution (e.g., normal distribution, early withdrawal, etc.).

- State and Federal Tax Details: Examine Boxes 12 through 15 for any federal or state tax withholdings.

- Consult IRS Instructions: Follow IRS guidelines on how to report the received distribution when filing your income tax return.

Legal Requirements for Form 1099-R

The Form 1099-R is a federally mandated document that complies with various taxation regulations. The IRS requires that payers furnish this form to both the recipient and the IRS itself, detailing income derived from retirement accounts and related plans. Legal compliance involves accurate and timely filing, failure of which can result in penalties for both the payer (financial institutions or plan administrators) and the recipient.

Key Elements of the 2014 Form 1099-R

- Payer's Information: Identifies the entity providing the distribution.

- Recipient's Information: Includes taxpayer identification details.

- Gross Distribution: The total amount disbursed before taxes or fees.

- Taxable Amount: The portion of the distribution subject to taxation.

- Federal and State Tax Withheld: Prepaid taxes reported that apply to the distribution.

- Distribution Codes: Reflect the type of distribution and any special conditions.

Who Typically Uses Form 1099-R

Form 1099-R is typically used by retirees, beneficiaries of retirement account holders, individuals receiving annuities, and those who have executed a rollover of funds from one retirement plan to another. Financial institutions and employers disbursing retirement benefits are responsible for generating and issuing this form to the relevant recipients for tax filing purposes.

IRS Guidelines and Filing Deadlines

- Issuance Deadline: The form must be distributed to recipients by January 31st.

- IRS Filing Deadline: Institutions issue the form to the IRS by March 31st if filing electronically.

- Reporting Requirements: The IRS mandates that all distributions, including rollovers and transfers, be reported accurately to reflect taxable income correctly.

- Compliance Details: Adhere strictly to IRS instructions for reporting distributions on individual federal tax returns.

Penalties for Non-Compliance

The IRS imposes penalties for inaccuracies or late submissions concerning Form 1099-R. Payers who fail to issue this form promptly to recipients or report inaccurately to the IRS may incur financial penalties. Similarly, recipients risk fines if they underreport taxable distributions derived from retirement accounts on their tax returns. Being informed about these responsibilities helps prevent unnecessary penalties and ensures compliance with tax laws.