Definition and Meaning of the 2-R Form

The 2-R form is a tax document used to report distributions from pensions, annuities, retirement, or profit-sharing plans, IRAs, and insurance contracts. This form is a critical part of documenting income from these sources for both the taxpayer and the Internal Revenue Service (IRS). The information on the 1099-R form helps determine the taxable portion of these distributions and ensures accurate reporting for federal income tax purposes. Taxpayers must ensure the data reported on their tax return matches the amounts disclosed on their 1099-R to avoid discrepancies or penalties.

How to Use the 2-R Form

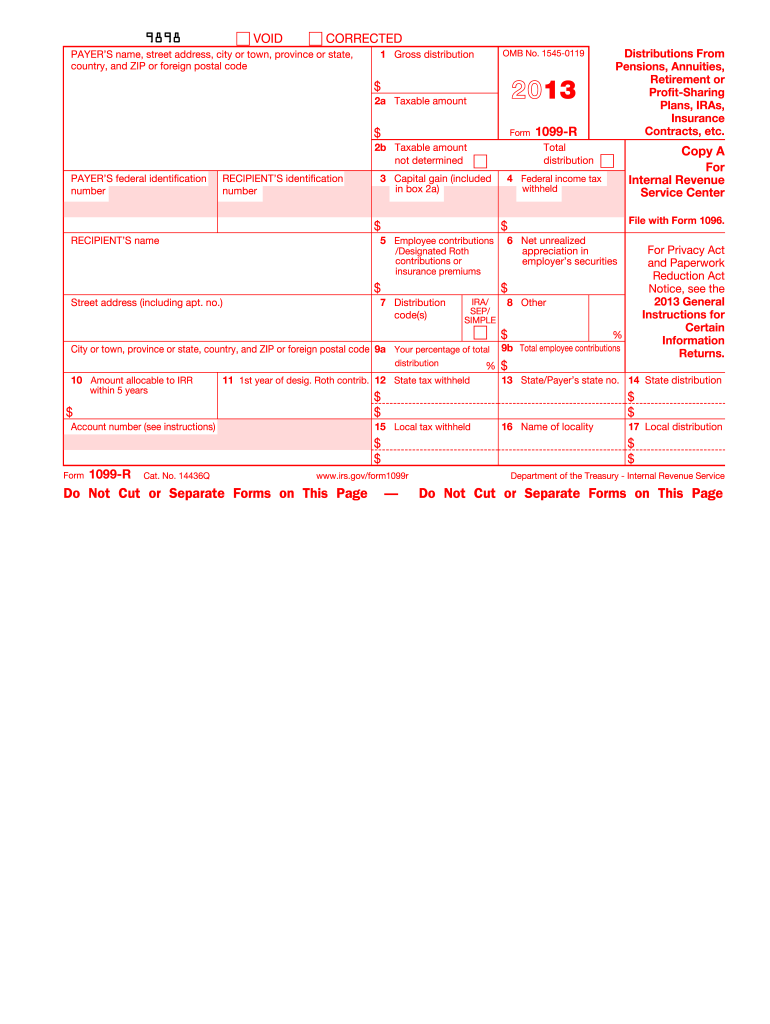

Using the 2-R form involves reporting the distributions indicated on the form on your annual tax return. Taxpayers should first receive the completed 1099-R from the financial institution or plan administrator that made the distributions. The IRS requires taxpayers to report these distributions on their tax returns, typically using forms like the 1040 or 1040A. It's essential to examine each box on the 1099-R carefully; for example, Box 1 indicates the gross distribution amount, while Box 2a provides the taxable amount. Ensuring consistency between the 1099-R and your tax return is crucial in accurately determining your taxable income and avoiding penalties.

How to Obtain the 2-R Form

The 2-R form should be provided by the entity that issued the distribution, such as a bank, financial institution, or annuity provider. These institutions are responsible for generating and mailing the form to you by January 31 of the year following the tax year in question. If you do not receive this form, contact the issuer directly to request a duplicate. It's also possible to access copies through online portals offered by some financial service providers, facilitating easy retrieval of this essential document for tax filing.

Steps to Complete the 2-R Form

Although taxpayers generally do not complete the 1099-R form themselves, understanding its components is helpful for cross-verifying received information. Here are the typical steps involved in handling this form:

- Receive the Form: Ensure you receive a copy from each distribution provider.

- Check for Accuracy: Verify that personal details and distribution amounts are correct.

- Report on Tax Return: Use information from boxes like 1 and 2a to fill out your tax return.

- Consult with a Tax Professional: If necessary, consult a tax advisor to ensure accurate reporting and understanding of taxable amounts.

Who Typically Uses the 2-R Form

Individuals who have received income through distributions from retirement accounts or annuities are typically the primary users of the 2-R form. This includes retirees receiving periodic pension payments, individuals withdrawing from IRA accounts, and beneficiaries of insurance contracts. This form is not exclusive to retirees; any taxpayer who took a withdrawal from a qualifying plan would utilize this form to report the income received.

Key Elements of the 2-R Form

The key elements of the 2-R form encompass various information box fields:

- Box 1: Gross distribution amount received.

- Box 2a: Taxable amount of the distribution.

- Box 2b: Indicates if the taxable amount is determined.

- Box 4: Federal income tax withheld.

- Box 7: Distribution code explaining the type of distribution. Understanding these boxes ensures you correctly report distributions on your tax return and understand the tax implications of your retirement income.

IRS Guidelines for the 2-R Form

According to IRS guidelines, the information on the 2-R form assists in determining the taxable and non-taxable portions of received distributions. The IRS mandates accuracy in reporting these amounts on your annual tax return to avert additional taxes due to underreporting. The IRS may also require supporting documentation if discrepancies arise, making it essential to retain copies of all 1099-R forms along with tax records for at least three years.

Penalties for Non-Compliance with the 2-R Form

Failure to accurately report details from the 2-R form on your tax return could lead to penalties. These might include fines for underreporting income or failing to pay the correct amount of tax. Additionally, intentional disregard for filing requirements can result in more severe penalties. Using accurate information from the 1099-R in your tax filings is crucial to maintain compliance and prevent unnecessary financial penalties.

Filing Deadlines and Important Dates for the 2-R Form

Financial institutions must issue the 2-R form by January 31 of the following year. Taxpayers should report the data from the 1099-R on their tax return by the April 15 deadline, unless an extension has been granted. It is advisable to confirm all amounts before this date to mitigate stress and potential errors in last-minute adjustments.