Definition & Meaning

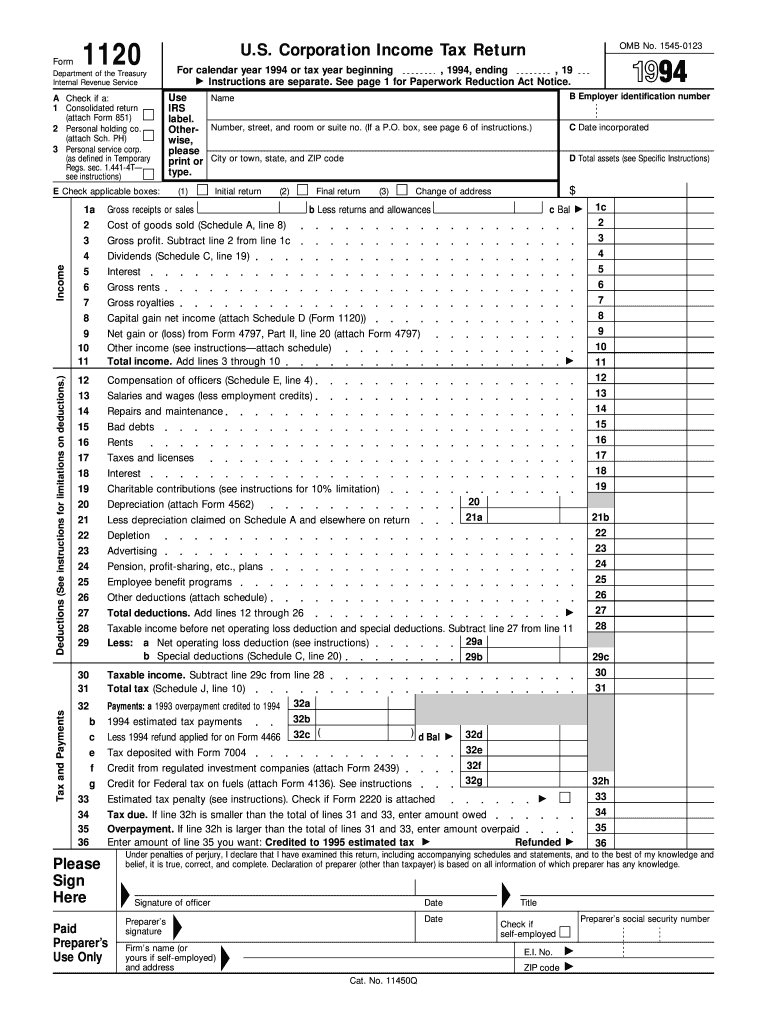

Form 1120, also known as the U.S. Corporation Income Tax Return, is a critical document that corporations are required to file annually with the Internal Revenue Service (IRS). The 1994 version of this form is used for reporting a corporation's income, deductions, and tax computations for that specific tax year. The form provides essential financial data used by the IRS to assess tax liabilities.

Corporations must provide detailed information across various sections, including income, expenses, dividends, and compensation of officers. This structured format ensures consistent reporting across different corporate entities, facilitating accurate tax assessments.

How to Use the 1994 Form 1120

Corporations use this form to document their financial activities from the year 1994, including revenue streams, expenditures, and taxable income. Here are the basic steps involved in utilizing this form:

- Review financial records: Gather all pertinent financial data, including income statements, expense ledgers, and balance sheets, for the 1994 fiscal year.

- Complete income and deduction sections: Fill out sections for revenue, cost of goods sold, and allowable deductions to calculate total taxable income.

- Determine tax liability: Use the completed details to compute the corporation’s total tax liability for the year.

- Attach relevant schedules: Include any additional schedules that apply, such as those for dividends or officer compensation.

- Submit the form: File the completed form with the IRS by the designated deadline.

How to Obtain the 1994 Form 1120

Obtaining an older tax form like the 1994 Form 1120 requires specific steps:

- Visit the IRS website: While current forms are readily available online, older versions may require contacting IRS archives directly.

- IRS offices: Visit an IRS office or call the IRS’s official phone support for assistance in accessing archived forms.

- Request via mail: Some firms, especially law or accounting firms, might hold copies in their archives. They can sometimes provide these if contacted directly.

Steps to Complete the 1994 Form 1120

Preliminary Preparation

- Collect documentation: Gather all financial documents pertinent to the 1994 tax year.

- Identify financial figures: Ensure accuracy in the numbers related to income, expenses, and deductions.

Completing the Form

- Income reporting: Begin with declaring all income from business operations.

- Deduction claims: List all business-related expenses and deductions that are allowable for reducing taxable income.

- Compute tax: Use the form’s guidelines to calculate the total federal tax owed.

Final Steps

- Review and Verify: Double-check all entries for accuracy.

- Submit the form: Ensure timely submission to avoid any penalties.

Key Elements of the 1994 Form 1120

- Income section: Detailing all revenue sources.

- Deductions: Entering allowable business expenses.

- Tax computation: Calculating the final tax liability.

- Schedules: Including additional schedules as required, such as dividends or officer compensations.

IRS Guidelines

The IRS provides specific guidelines to ensure that Form 1120 is completed accurately:

- Instructions: Always refer to the IRS instructions for detailed guidance.

- Compliance: Adhere to the IRS rules concerning credits, deductions, and taxable income.

- Updates: Note any amendments or changes in tax law that may affect the 1994 tax year filings.

Filing Deadlines / Important Dates

For the 1994 Form 1120, the standard filing deadline for corporate taxes typically falls on March 15, unless another date is stipulated due to special circumstances. Extensions may be requested for corporations requiring additional time to gather documentation or manage complex financial details.

Penalties for Non-Compliance

Corporations failing to file Form 1120 on time can face significant penalties. These can include:

- Late filing fees: Charged per month the return is overdue.

- Penalties on unpaid taxes: Additional interest on any tax not paid by the original due date.

Maintaining timely and accurate submissions of this form is crucial to avoid costly penalties and maintain good standing with tax authorities.