Understanding the Company Tax Return

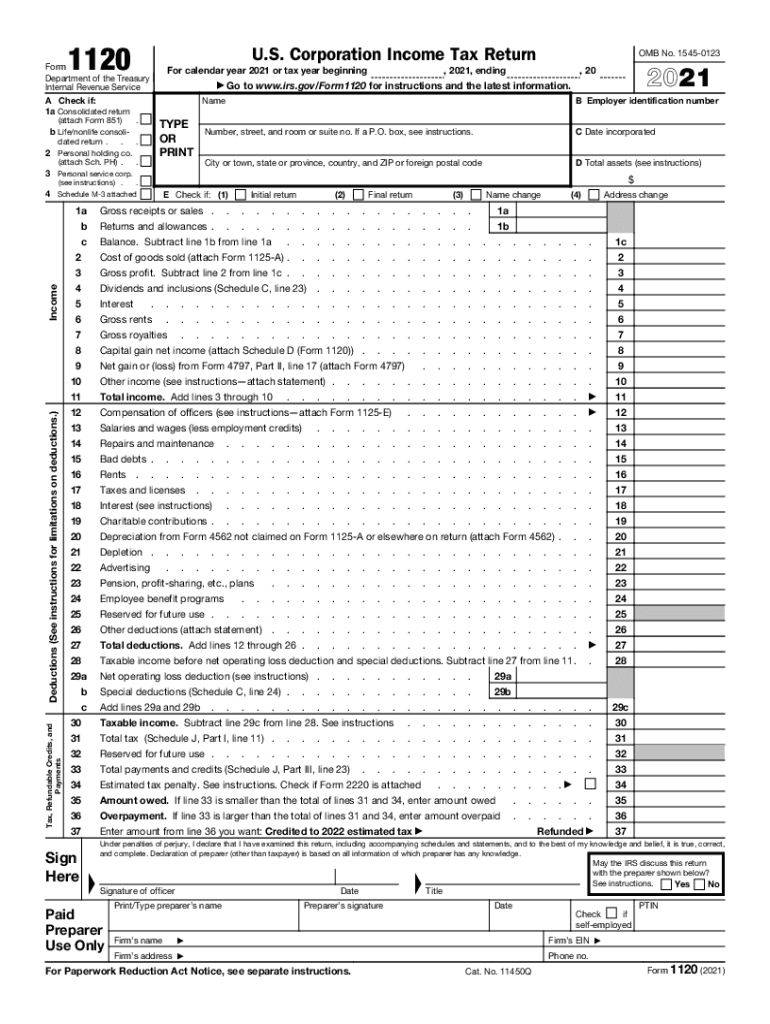

The company tax return, often represented by IRS Form 1120, is a critical document used in the United States by corporations to report their income, deductions, and tax liabilities to the Internal Revenue Service (IRS). This form serves as a comprehensive record of a company’s financial activities, ensuring compliance with federal tax laws. Corporations are required to file this form annually, reflecting their financial performance over the fiscal year.

How to Use the Company Tax Return

Corporations use the company tax return form to declare their income, identify deductible expenses, and calculate the taxes owed to the federal government. By completing this form accurately, businesses ensure that all revenues and expenses are appropriately recorded, which is essential for maintaining financial transparency and avoiding legal complications. This form also serves as a tool for corporate financial planning, enabling companies to optimize their tax strategies and improve fiscal management.

Steps to Complete the Company Tax Return

Completing the company tax return involves several detailed steps:

- Gather Financial Documents: Collect all pertinent financial documents, including income records, expense receipts, and previous tax returns.

- Report Income: Enter the total gross income earned by the corporation.

- Deduct Expenses: Itemize deductible business expenses such as wages, rent, utilities, and materials.

- Calculate Tax Liabilities: Use the provided calculations to determine the amount of tax owed.

- Review and Submit: Carefully review the completed form for accuracy before submitting it to the IRS by the specified deadline.

These steps ensure a thorough and compliant filing process, helping to prevent potential discrepancies.

Required Documents for Filing

When preparing to file a company tax return, corporations must compile several key documents:

- Financial Statements: Income statements and balance sheets.

- Expense Receipts: Evidence of business-related expenses.

- Payroll Records: Documentation of salaries and wages paid to employees.

- Previous Tax Returns: For reference and verification purposes.

Ensuring all necessary documents are in order can facilitate a smoother filing experience and help avoid delays.

Filing Deadlines and Important Dates

The company tax return must be filed annually, with the standard due date being the 15th day of the fourth month following the end of the corporation’s fiscal year, typically April 15 for calendar-year taxpayers. However, if this date falls on a weekend or holiday, the deadline extends to the next business day. Corporations should keep track of these dates to avoid penalties.

Software Compatibility for Filing

Form 1120 can be prepared and filed using various tax software platforms such as TurboTax, QuickBooks, and DocHub itself. These tools enhance accuracy and efficiency by guiding users through the tax filing process, ensuring all required fields are completed correctly. Many programs also offer integration with business accounting software, streamlining data entry and verification.

Penalties for Non-Compliance

Failure to file a company tax return or pay taxes due can result in significant penalties and interest charges. The IRS imposes fines based on the amount of tax owed, coupled with accruing interest on late payments. Additionally, consistent non-compliance may trigger audits or further legal action, underscoring the importance of timely and accurate filings.

Business Entity Types and the Company Tax Return

Different types of business entities, such as C corporations, are required to file Form 1120. In contrast, S corporations use a different form, the 1120S, which is tailored to their unique tax requirements. Understanding the specific filing requirements for each entity type helps businesses adhere to regulatory obligations and utilize appropriate forms.

State-Specific Rules and Variations

While the company tax return covers federal tax obligations, corporations must also be aware of state-specific tax filing requirements, as these can vary significantly. Each state has its own set of tax laws and forms, which may include additional liabilities or credits. Reviewing state regulations is essential for complete compliance at both federal and state levels.