Definition and Purpose of Form 4

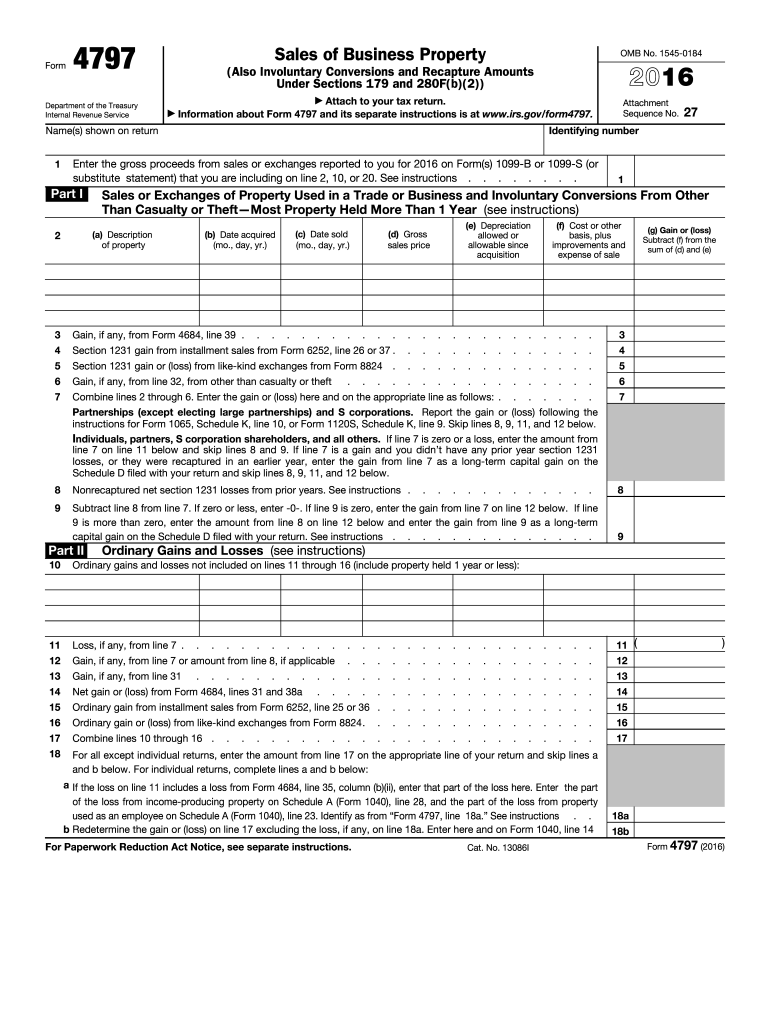

Form 4797, titled "Sales of Business Property," is an official document issued by the Internal Revenue Service (IRS) used for reporting the sale or exchange of business property and calculating any associated gain or loss. Businesses utilize this form to report the sale of real estate, machinery, vehicles, and other business assets. Completing Form 4797 helps ensure compliance with U.S. tax regulations and accurately reflects the entity's financial transactions related to the disposition of business property. The essence of Form 4797 is to facilitate transparent reporting of financial activities that affect taxable income, thereby aligning with IRS mandates for accurate taxation.

-

Real World Scenario: A small manufacturing business sells an underutilized piece of equipment. They use Form 4797 to report this sale to the IRS for the 2011 tax year.

-

Types of Property: This form covers various asset types, including real estate improvements, intangible property like patents, and depreciable equipment.

How to Use Form 4 Effectively

Properly using Form 4797 necessitates a step-by-step approach to ensure all relevant transactions are reported accurately. Business owners or accountants must first identify all applicable sales or exchanges and then gather the necessary financial documentation, such as purchase receipts and previous tax returns.

-

Step-by-Step Process:

- Gather Financial Records: Collect all documents related to asset purchases and sales, including invoices and depreciation schedules.

- Calculate Gains and Losses: Determine the original purchase price, any improvements, and compare this with the selling price.

- Complete Sections I, II, and III: Include details such as description of property, date acquired, date sold, and the computation of gains or losses.

-

Special Considerations: Pay attention to involuntary conversions and recapture amounts which require detailed computation under sections 179 and 280F.

Steps to Complete Form 4

Filling out Form 4797 requires careful detailing of each transaction. Follow these structured instructions:

- Part I - Sales or Exchanges of Property: Report sales of business property that do not meet the criteria for capital gains treatment.

- Part II - Ordinary Gains and Losses: For business assets that did not qualify for capital gains treatment according to IRS rules.

- Part III - Gain from Dispositions of Property Used in a Trade or Business: Calculate net gain from property used in a trade or business.

- Part IV - Recapture Amounts Under Sections 179 and 280F(b)(2): Address recapture of depreciation if business assets have been expensed.

- Example: A mechanic shop sells a company vehicle. They report the transaction in Part III, considering any depreciation previously claimed.

Key Elements of Form 4

Understanding the essential components of Form 4797 is crucial for accurate completion. These key elements include basic information about the business, specific transaction details, and calculations of financial outcomes from property sales.

-

Basic Business Information: Name, identification number, and tax year specifics.

-

Transaction Details: Includes type of property, acquisition and sale dates, and the original purchase price.

-

Financial Calculation Sections: Areas for computing adjusted basis, selling price, and net changes to taxable income.

-

Pro Tip: Use accounting software to maintain accuracy and streamline the calculation processes for parts I-IV.

IRS Guidelines for Form 4

The IRS provides explicit guidelines to ensure Form 4797 is completed in accordance with federal tax laws. Follow these regulations to confirm compliance and optimal reporting.

-

Understanding IRS Codes: Familiarize with Sections 179, 1231, and 280F, which govern property depreciation recapture.

-

Avoid Common Errors: Double-check calculations and ensure all financial data correlates with provided IRS rules.

-

Example: Proper adherence to IRS guidelines can prevent potential audits and penalties for incorrect reporting.

Filing Deadlines and Important Dates

Form 4797 should be submitted as part of the taxpayer's annual return. The deadline typically aligns with the April 15 deadline for individual taxes but can vary based on extensions or different fiscal year ends for businesses.

-

Calendar Milestones:

- April 15: Standard filing deadline for calendar year taxpayers.

- Electronic Extensions: Available if more time is needed, usually granting an additional six months.

-

Important Note: Confirm specific deadlines through the IRS resources or consult with a tax professional to ensure timely filing.

Penalties for Non-Compliance with Form 4

Failure to file Form 4797 accurately or on time can result in penalties and interest charges. Understanding potential consequences can motivate businesses to prioritize compliance.

-

Late Filing Penalties: A financial penalty assessed for not submitting the form by the due date.

-

Accuracy Penalties: Inaccurate reporting can lead to further scrutiny by the IRS and additional charges.

-

Preventative Measures: Maintaining thorough documentation and possibly consulting tax professionals can reduce errors and penalties associated with non-compliance.

Software Compatibility and Filing Options

Modern tax software aids in the preparation and submission of Form 4797, offering various ways to integrate records and ensure accuracy.

-

Software Compatibility:

- Compatibility with platforms like TurboTax and QuickBooks can simplify filing by automating calculations and generating necessary reports.

-

Filing Methods: Whether filing electronically or by mail, using recognized tax software can ensure that all data aligns with IRS formats and standards.

-

Digital Filing Benefits: Electronic submissions are typically more fast and secure, reducing the likelihood of lost documents or data errors.