Definition and Meaning of the 2015 Form 4797

Form 4797, utilized by the Internal Revenue Service (IRS), is employed to report proceeds from the sale or exchange of business property. This includes involuntary conversions and recapture amounts specified under various IRS sections. The form ensures taxpayers accurately declare gains or losses from business properties, assisting in the comprehensive calculation of income. It also addresses recapture possibilities when property use for business dips below a stipulated percentage.

Who Typically Uses the 2015 Form 4797

Form 4797 is commonly filled out by self-employed individuals, business owners, and corporate entities engaging in business property transactions. These can include those in trades, businesses, or holding properties predominantly for investment. Property owners who experience a decrease in the business use of their assets are also required to use this form to report such changes. It serves a crucial role for LLCs, corporations, partnerships, and sole proprietorships needing to report any taxable gains or losses.

Steps to Complete the 2015 Form 4797

- Gather Required Information: Start by assembling all pertinent documents, including purchase and sale records, to compute the correct gains or losses.

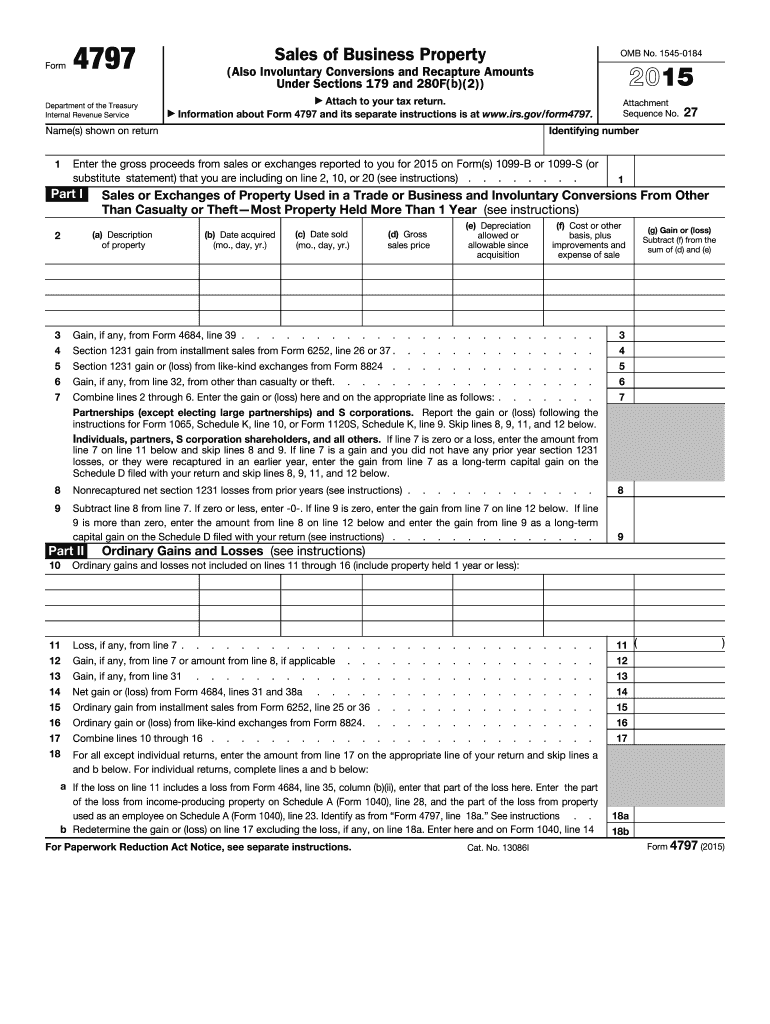

- Understand the Categories: The form is divided into Part I, Part II, Part III, and Part IV. Each section serves a different purpose, such as reporting ordinary gains, losses, and captured recapture sections.

- Fill Part I: For gains from property held over a year or 12 months, like depreciated property, the results are reported in Part I.

- Complete Part II: Short-term gains or losses are entered here, relevant to properties held for a year or less.

- Enter Details in Part III: This section focuses on gains from depreciation recapture, essential to avoid understatement of profits.

- Finalize with Part IV: Part IV considers the helming of non-recaptured gains from the sale of depreciated real estate, offering one more computes space.

Important Terms Related to the 2015 Form 4797

- Involuntary Conversions: These occur when property changes due to devastation like theft or natural disaster.

- Recapture: A crucial term where previously taken depreciation is required to be added back if the business utilization of the property falls below a defined percentage.

- Ordinary Gains: These include but are not limited to, gains not classified as capital gains and are thus taxed differently.

IRS Guidelines for the 2015 Form 4797

The IRS mandates that Form 4797 is clearly and accurately filled to reflect every detail of business transactions involving property. IRS guidelines provide instructions for each part of the form, detailing how to record and compute gains and losses. Taxpayers should always refer to current IRS instructions available for the specific filing year.

Filing Deadlines and Important Dates for the 2015 Form 4797

Form 4797 must be filed with your tax return by April 15 of the year following the tax year you are filing for. If an extension is filed, the deadline can be pushed to October 15, but all tax payments are still due by the April deadline to avoid penalties and interests.

Examples of Using the 2015 Form 4797

- Example 1: A tech business disposed of old servers used for over two years. Recording the sale price, cost, and depreciation assists the owner in calculating either a gain or loss.

- Example 2: An investor suffered property damage due to a flood, leading to an involuntary conversion. Insurance recoveries and deductions impact how the form is filed to reflect the transaction accurately.

Penalties for Non-Compliance with the 2015 Form 4797

Failure to file Form 4797 or providing incorrect information can lead to penalties, varying from a flat rate fine to a certain percentage of the unpaid taxes. The IRS can impose harsh deliberations for intentional non-compliance, including interest on any amount due.

Software Compatibility with the 2015 Form 4797

The 2015 Form 4797 is supported by tax preparation software, such as TurboTax and QuickBooks. These programs assist users in navigating the form correctly, streamlining calculations, and ensuring IRS compliance. The software aids in the step-by-step completion, enforcing data accuracy and providing help regarding complex tax provisions in a user-friendly manner.