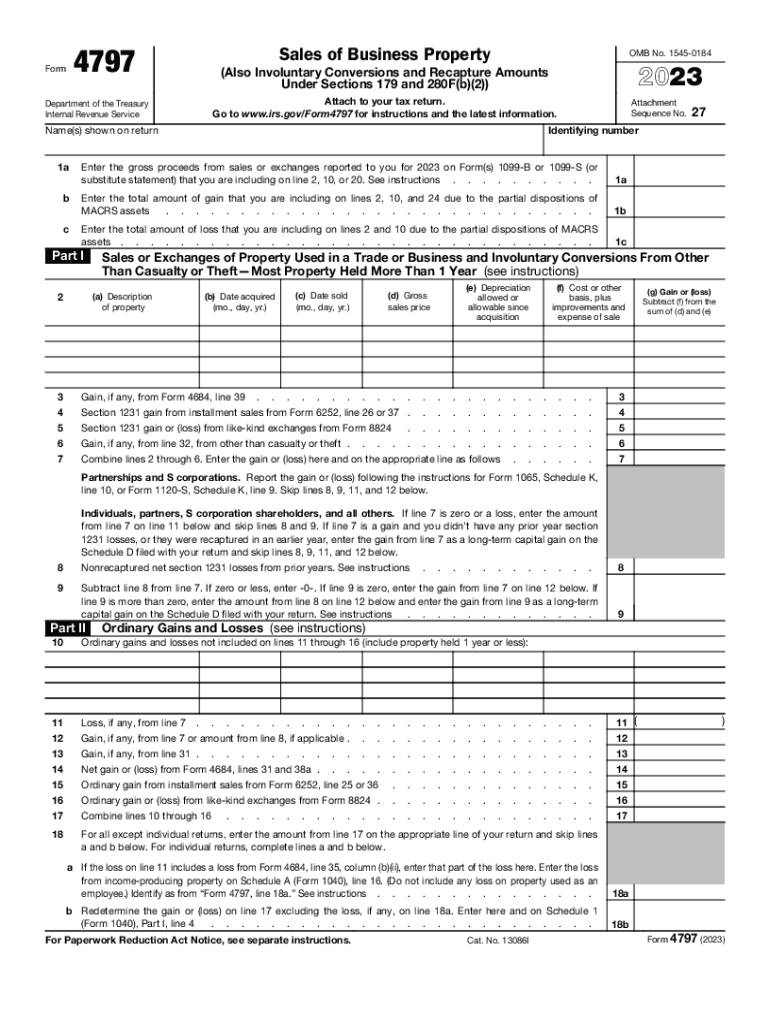

Definition & Purpose of Form 4797

Form 4797, Sales of Business Property, is essential for taxpayers to report gains or losses from the sale, exchange, or involuntary conversion of business property. It covers detailed information about transactions involving assets used in a trade or business, including capital gains or losses, recapture amounts under certain IRS sections, and depreciable property sales. Completing this form accurately ensures compliance with U.S. tax regulations and helps taxpayers determine the correct amount of tax liability.

Practical Examples

- Small Businesses: A small café owner selling kitchen equipment would use Form 4797 to report gains or losses from the disposal of such business assets.

- Real Estate Transactions: For individuals selling commercial property, this form is crucial for reporting any gains or deductions resulting from the sale.

Steps to Complete Form 4797

Filing Form 4797 involves several steps, including gathering necessary documentation and understanding specific sections of the form.

- Identify Transactions: Determine which sales, exchanges, or involuntary conversions of business property need to be reported.

- Gather Documentation: Collect all pertinent financial documents, such as purchase invoices, sale contracts, or depreciation schedules.

- Fill Out Sections I-IV:

- Part I: Report sales or exchanges of property used in a trade or business.

- Part II: Detail ordinary gains and losses.

- Part III: Provide information on gains from involuntary conversions.

- Part IV: Summarize recaptured depreciation and any other applicable recapture amounts.

- Calculate Gains or Losses: Utilize the figures from the parts above to compute the overall gain or loss.

- Review & Submit: Double-check entries for accuracy and submit the completed form with your federal tax return.

Common Pitfalls

- Incorrect Depreciation Recapture: Ensure correct calculations to avoid misreporting of taxable income.

- Missed Transactions: Double-check that all relevant transactions are included to prevent penalties.

Important Terms & Definitions

Understanding key terminologies is crucial for accurate completion of Form 4797.

- Depreciable Property: Assets that lose value over time due to use, wear, and obsolescence, which are subject to depreciation deductions.

- Recapture: The process of re-adding previously deducted depreciation to taxable income when the asset is sold at a profit.

- Involuntary Conversion: Occurs when property is destroyed, stolen, or condemned, leading to compensation that triggers tax obligations.

Who Typically Uses Form 4797

Form 4797 is primarily used by individuals, partnerships, and corporations involved in the sale or exchange of business property.

User Scenarios

- Self-employed Professionals: Independent contractors disposing of work-related equipment.

- Corporations: Entities selling machinery or office furniture no longer needed.

Key Elements of Form 4797

The form consists of several essential parts that require careful completion.

- Transaction Details: Full disclosure of all relevant sales, including dates, sales price, and adjusted basis.

- Recapture Information: Accurate depiction of recaptured depreciation to reflect true taxable gains or losses.

- Separate Entries: Ensure different transactions are individually itemized for clarity.

Legal Use & Considerations

Legally, Form 4797 is recognized as an official IRS form necessary for reporting sales and exchanges of business-used property accurately. Misrepresenting information or underreporting earnings can lead to significant penalties and legal implications.

IRS Compliance

Taxpayers must follow guidelines specified by the IRS to prevent non-compliance issues, including:

- Timely Filing: Submit by the tax return deadline to avoid late fees.

- Accurate Reporting: Ensure all entries are true and verifiable with proper documentation.

Filing Deadlines & Important Dates

The completion of Form 4797 typically aligns with federal tax return deadlines.

- General Deadline: April 15 of each year, unless it falls on a weekend or holiday.

- Extensions: Taxpayers can request extensions for additional time if necessary, usually up to six months.

Taxpayer Scenarios & Business Types

Certain business types and taxpayer categories gain specific benefits and responsibilities when using Form 4797.

Beneficial Business Types

- LLCs & Partnerships: Allows clear reporting of asset sales used in active business operations.

- Real Estate Investors: Essential for accurately documenting property sales and renovations for tax benefits.

Specific Taxpayer Groups

- Retired Individuals: Selling business assets post-retirement.

- Students & Part-Time Business Owners: Reporting sales of part-time venture equipment.

IRS Guidelines & Document Submission

Ensure adherence to IRS standards when filing Form 4797.

- Submission Methods: Can be mailed or e-filed with federal tax returns.

- Documentation: Attach supportive documents like sales agreements, purchase contracts, and record evidence for reported transactions.

Software Compatibility

- Tax Software: Often, systems like TurboTax or QuickBooks streamline the process, offering templates and automated calculations. However, manual review is advised to catch discrepancies.

This comprehensive guide to Form 4797 highlights its utility, correct application, and ensures taxpayers meet their reporting obligations effectively, adhering to the required guidelines set forth by the IRS.