Definition and Purpose of IRS Form 4

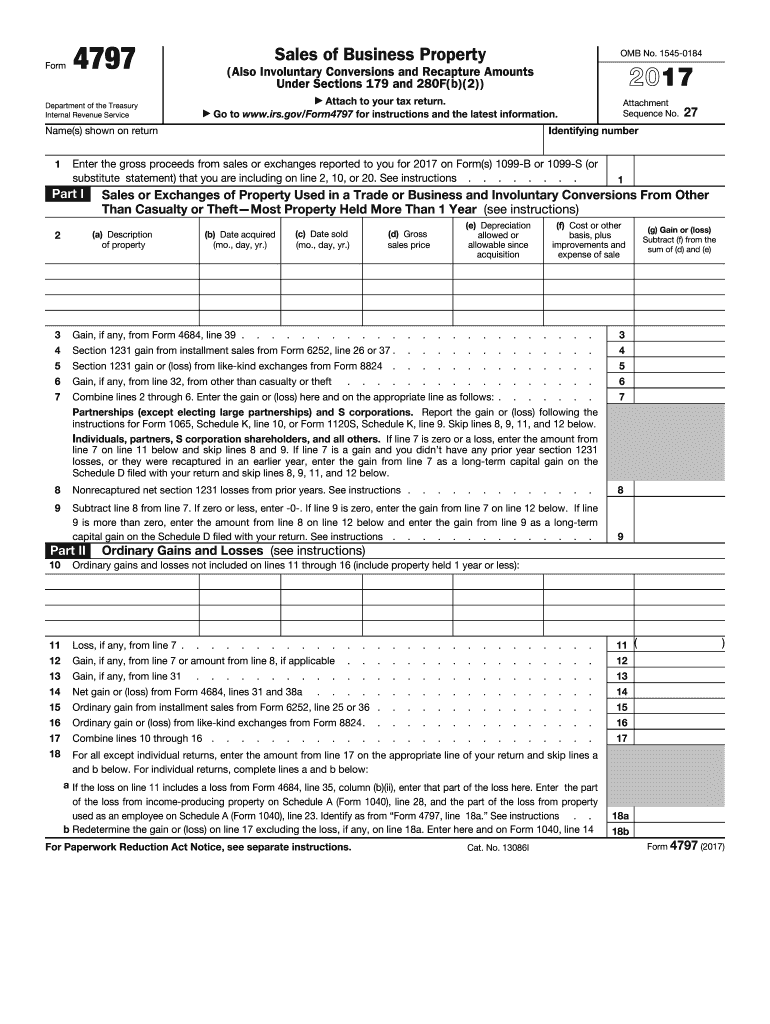

IRS Form 4797, titled "Sales of Business Property," is a tax document used by the IRS to record sales, exchanges, or involuntary conversions of certain types of property. This form is crucial in reporting gains or losses from such transactions. It is specifically designed to help taxpayers document any recapture of depreciation or other expenses that have been previously deducted. Knowing how to file this form accurately is essential for maintaining compliance with U.S. tax regulations and ensuring that all taxable events are correctly reported.

Steps to Complete the IRS Form 4

-

Identify the Type of Property:

- Properties are categorized into different sections on the form: Section 1245 (e.g., machinery, equipment), Section 1250 (e.g., buildings), and other types.

- Depending on the property, different calculations and tax treatments may apply.

-

Calculate Gross Proceeds:

- Report the total gross proceeds received from the sale or exchange of the property.

- Ensure that accurate figures are used to avoid discrepancies.

-

Determine Gain or Loss:

- Calculate the gain or loss by deducting the adjusted basis of the property from the gross proceeds.

- Adjusted basis is typically the cost of acquisition plus improvements minus allowable depreciation.

-

Report Recapture Amounts:

- If depreciation or amortization was previously claimed, determine if any of it needs to be recaptured and included as income.

- Recapture rules differ between property types and are an essential part of complying with tax laws.

-

Complete the Necessary Sections:

- Fill out Part I for sales or exchanges of property used in the trade or business.

- Use Part II for ordinary gains and losses.

- The form may require additional attachments or details depending on the complexity of the transactions.

-

Verify and Submit:

- Double-check all calculations to ensure accuracy.

- Submit the completed form as part of your federal income tax return using your preferred method (mail or electronic filing).

Important Terms Related to IRS Form 4

- Adjusted Basis: The original cost of a property, adjusted for improvements, depreciation, and other factors.

- Recapture: The inclusion of previously deducted depreciation as taxable income during the sale of a property.

- Ordinary Gain/Loss: Refers to regular business income/loss as opposed to capital gains or losses.

- Section 1245 Property: Typically includes depreciable personal property.

- Section 1250 Property: Generally refers to real property, like buildings, that are subject to different recapture rules.

Who Typically Uses the IRS Form 4

- Businesses and Corporations: Entities that sell or exchange business property regularly use Form 4797 to report such transactions.

- Individuals with Business Property Sales: Self-employed individuals or those involved in real estate or other property transactions.

- Partnerships and S Corporations: Often involved in property transactions related to their operations, these entities must report using Form 4797.

Filing Deadlines and Important Dates

- Form 4797 typically needs to be filed with your annual tax return by the standard IRS tax deadline, which is usually April 15th. However, if this date falls on a weekend or holiday, the deadline may be extended.

- Missing the deadline could result in penalties or interest on unpaid taxes.

IRS Guidelines for IRS Form 4

- The IRS provides detailed guidelines on how to complete Form 4797 in Publication 544, "Sales and Other Dispositions of Assets."

- It is vital to follow the IRS instructions closely to avoid errors that could lead to audits or penalties.

Required Documents for Completing IRS Form 4

- Sale Contracts or Exchange Agreements: Documenting the transaction details.

- Depreciation Schedules: Showing the depreciation claimed on the property.

- Property Appraisals or Valuations: To support reporting of fair market values.

- Records of Improvements or Repairs: Assisting in determining the adjusted basis.

Penalties for Non-Compliance

- Failing to file Form 4797 correctly or omitting significant information can lead to penalties or additional scrutiny from the IRS.

- Penalties may include fines or additional interest charges on underreported taxes, highlighting the importance of accuracy and timely submission.