Definition and Meaning of the FW8BEN

The W-8BEN, known as the Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting, is a pivotal document in the tax realm. It enables foreign individuals and entities to validate their status as non-U.S. residents and allows them to claim advantageous tax treaty benefits. This form is crucial for reducing or exempting the withholding tax on income sourced from the U.S., such as dividends, royalties, or other passive income. Understanding the W-8BEN is essential for any foreign individual or entity engaged in financial activities with U.S.-based income.

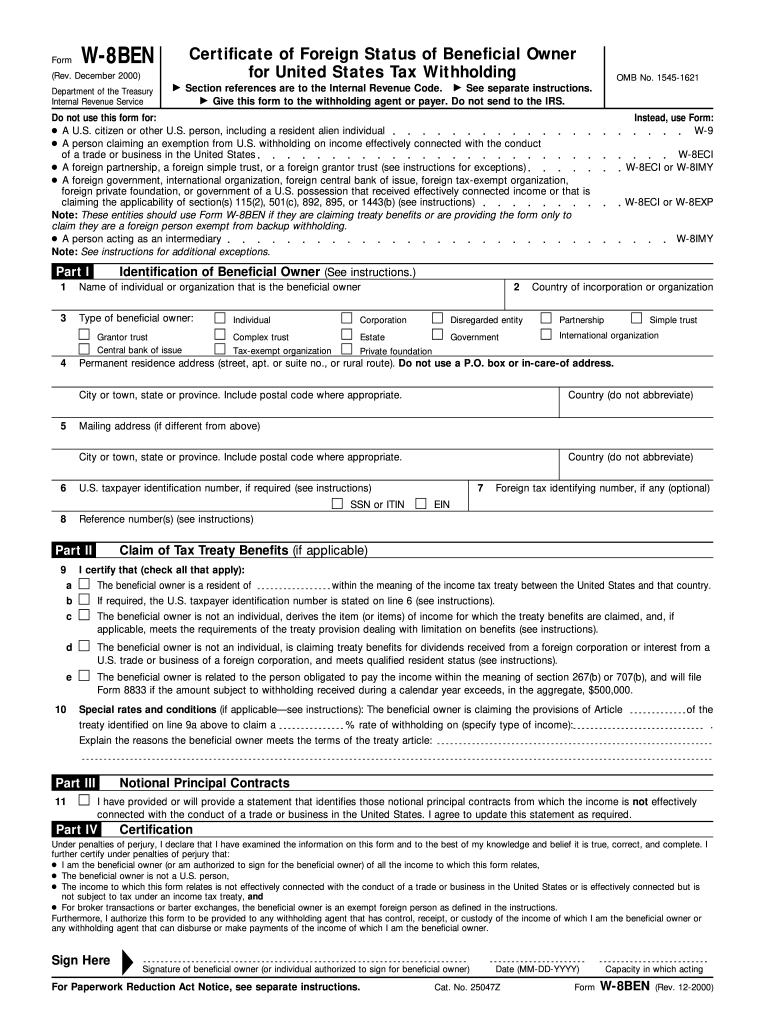

Key Elements of the FW8BEN

To complete the W-8BEN accurately, one needs to be aware of its critical components:

- Part I – Identification of Beneficial Owner: Contains basic information like name, country of citizenship, and permanent address.

- Part II – Claim of Tax Treaty Benefits: Where the filer claims benefits under an applicable tax treaty. This section requires specific details about the treaty article and percentage rate of withholding.

- Part III – Certification: Affirms the accuracy of the information provided. The signatories must ensure all inputs conform to the actual circumstances.

These elements must be filled out accurately to ensure compliance and avoid unnecessary tax withholdings.

Steps to Complete the FW8BEN

Completing the W-8BEN involves several detailed steps:

- Gather Required Information: Collect personal details, including those of residence and taxpayer identification.

- Understand Tax Treaty Provisions: Use resources like IRS publications to determine eligibility for tax treaty benefits.

- Fill Out Part I: Input personal and contact information correctly.

- Complete Part II: Carefully select and fill in applicable tax treaty provisions.

- Sign and Date the Form: Ensure the form's certification section is properly signed and dated.

Attention to detail in each step helps prevent submission errors and resultant delays.

Who Typically Uses the FW8BEN

The W-8BEN form is typically utilized by:

- Foreign Individuals: Non-U.S. residents earning income from U.S. sources.

- Entities: Certain foreign corporations and partnerships that are beneficial owners of U.S.-sourced income.

- Investors: Those receiving dividends or interest from U.S. sources often need to file this form to benefit from reduced tax rates provided by treaties.

Understanding the demographics of typical users can help streamline the form completion process and ensure proper compliance.

IRS Guidelines for the FW8BEN

The IRS provides comprehensive guidelines that are essential for correctly filling out the W-8BEN. These guidelines include specifics about eligibility for tax treaty benefits, detailed instructions on form sections, and conditions that warrant the updating or re-filing of the form. Familiarity with these guidelines is invaluable for maintaining compliance with U.S. tax laws and leveraging any potential tax reductions.

Legal Use of the FW8BEN

The form's legal use is primarily to certify a person's foreign status and to claim treaty benefits. Misuse or misrepresentation on the form can result in penalties or revocation of treaty benefits. It's crucial that individuals and entities use the form in accordance with IRS regulations and legal provisions to ensure it serves its intended purpose without legal complications.

Penalties for Non-Compliance

Failing to submit or inaccurately completing the W-8BEN can result in several consequences:

- Increased Withholding Rates: Without the form, income may be subject to a default 30% withholding rate.

- Legal Repercussions: Providing false information can lead to legal penalties or fines.

- Loss of Treaty Benefits: Incorrect submissions may cause a forfeiture of tax treaty benefits, increasing tax liability.

Understanding and avoiding potential penalties ensures financial operations are unhindered by additional tax burdens.

Form Submission Methods

There are multiple ways to submit the W-8BEN:

- Online Platforms: Many financial institutions allow electronic submission, streamlining the process.

- Mail: Submission via postal services is also a traditional method, though it may involve longer processing times.

- In-Person Delivery: Directly handing the form to the payer or withholding agent ensures immediate acknowledgment.

Selecting the appropriate submission method can enhance efficiency and reliability in processing.