Type text, add images, blackout confidential details, add comments, highlights and more.

02. Sign it in a few clicks

Draw your signature, type it, upload its image, or use your mobile device as a signature pad.

03. Share your form with others

Send dr 5714 form via email, link, or fax. You can also download it, export it or print it out.

How to use or fill out form dr 5714 2014 with our platform

Ease of Setup

DocHub User Ratings on G2

Ease of Use

DocHub User Ratings on G2

Click ‘Get Form’ to open it in the editor.

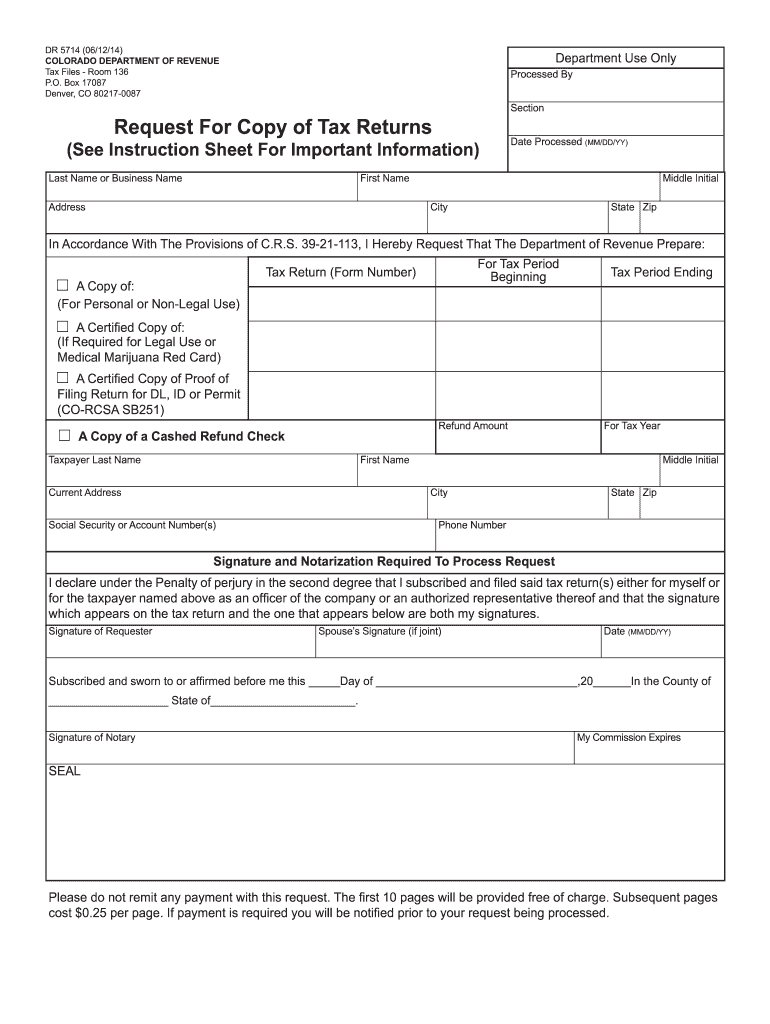

Begin by entering your last name or business name in the designated field. Follow this by filling in your first name and middle initial, along with your current address, city, state, and zip code.

Specify the tax period for which you are requesting copies by entering the beginning and ending dates in the appropriate fields. Be precise to ensure accurate processing.

Indicate whether you need a copy of the tax return or a certified copy for legal use. If applicable, provide details for any additional requests such as proof of filing.

Complete the signature section. Ensure that both you and your spouse (if joint) sign where indicated. Remember, notarization is required for processing.

Review all entered information for accuracy before submitting. Once confirmed, mail the completed form to the Colorado Department of Revenue as instructed.

Start using our platform today to fill out form dr 5714 2014 easily and efficiently!

Form dr 5714 2014 pdfForm dr 5714 2014 instructionsForm dr 5714 2014 downloadForm 5713Colorado Department of RevenueColorado tax transcriptDr 5785State tax transcript online

Security and compliance

At DocHub, your data security is our priority. We follow HIPAA, SOC2, GDPR, and other standards, so you can work on your documents with confidence.

TISKBOOK OKUGASA. 3. The white copy of this form is a record of persons who have read or had disclosed to them any part of the document identified in Item 2Read more

Feb 28, 2026 Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No.Read more

Cookie consent notice

This site uses cookies to enhance site navigation and personalize your experience.

By using this site you agree to our use of cookies as described in our Privacy Notice.

You can modify your selections by visiting our Cookie and Advertising Notice.