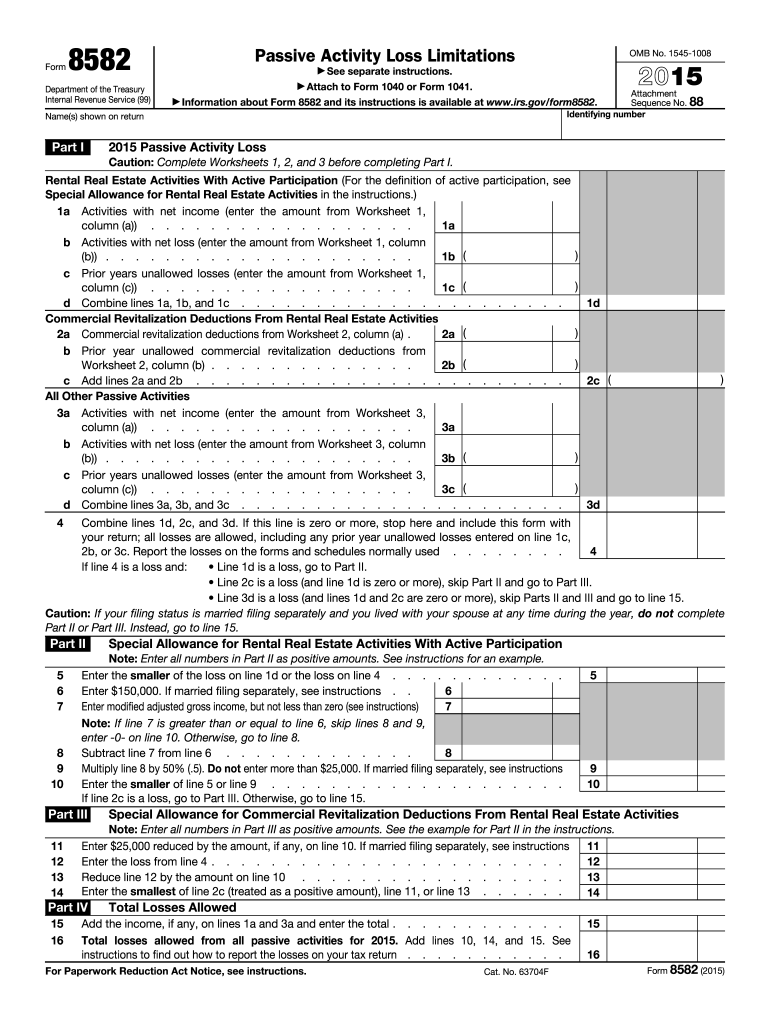

Definition and Purpose of the 2015 Form 8582

Form 8582, utilized by the IRS, reports passive activity loss limitations for individuals and estates. These losses stem from rental real estate activities, commercial revitalization deductions, and other passive activities. The form includes calculations necessary for determining allowable losses, following specific IRS guidelines. Taxpayers must complete related worksheets that help in accurately assessing these losses, which are then reported on their tax returns. This form is essential for taxpayers involved in real estate or other passive income-generating activities, aiming to provide clarity in reporting such financial elements.

How to Obtain the 2015 Form 8582

To acquire the 2015 version of Form 8582, taxpayers can visit the official IRS website, where downloadable forms are available. Alternatively, tax preparation software often includes access to historical tax forms, such as the 2015 version. Professional tax preparers also keep an archive of forms and can provide one upon request. It’s crucial to verify the year when downloading the form to ensure it matches the tax year for which the filing is being completed.

Steps to Complete the 2015 Form 8582

- Gather Necessary Documents: Ensure all sources of passive income and related financial information are available.

- Complete Worksheets: Follow the instructions provided within the form to fill out the necessary calculations for passive activity losses.

- Input Data on Form: Transfer the calculated figures from your worksheets into the designated sections of Form 8582.

- Review for Accuracy: Double-check all entries for accuracy. Errors can lead to incorrect tax reporting.

- Attach to Tax Return: Once final, attach Form 8582 to your annual tax return before submission.

Detailed Completion Example

- Example Scenario: A taxpayer with a rental property generates passive income. They calculate their total income and allowable expenses, ending with a net passive loss. This loss is recorded on the form after adjustments as indicated by form instructions.

Why Use the 2015 Form 8582

Using Form 8582 is necessary for those with passive activities where loss limitations apply. It helps taxpayers offset specific passive gains, reducing taxable income effectively. This form ensures adherence to IRS regulations, avoiding penalties and inaccuracies in tax reports. It’s specifically beneficial for investors with rental properties, enabling them to manage financials with greater precision.

Who Typically Uses the 2015 Form 8582

Form 8582 is designed for individuals and estates engaged in activities recognized as passive by IRS standards. This includes real estate owners, investors in limited partnerships, and those involved in business activities where they do not materially participate. These taxpayers use the form to calculate losses and determine what can be reported against their passive income, affecting their taxable income conclusions.

Key Elements of the 2015 Form 8582

- Worksheet Completion: Essential for determining allowable losses.

- Loss Limitation Calculation: A critical part of the form to prevent exceeding loss deductions beyond set IRS limits.

- Required Attachments: Comprehensive records of passive activities and financial transactions are necessary to ensure accuracy.

Form Structure Overview

- Part I: Deals with income and losses calculation.

- Part II: Involves special allowance for rental real estate.

- Part III: Focuses on unimproved or incomplete activities.

IRS Guidelines for the 2015 Form 8582

The IRS provides explicit instructions on who should file Form 8582 and how calculations should be completed. Adherence to these guidelines ensures compliance and minimizes errors. Comprehensive instructions and examples within IRS publications give taxpayers a clear process for completing the form, addressing common scenarios and potential complexities.

Examples of Using the 2015 Form 8582

Consider a taxpayer with multiple rental properties. Each property generates income and incurs expenses which must be accounted for on Form 8582. For instance, if one property has a net loss, it can be applied against gains from another, subject to IRS rules. Thus, Form 8582 provides a structured manner for handling such iterative calculations and reporting them appropriately.