Definition & Meaning

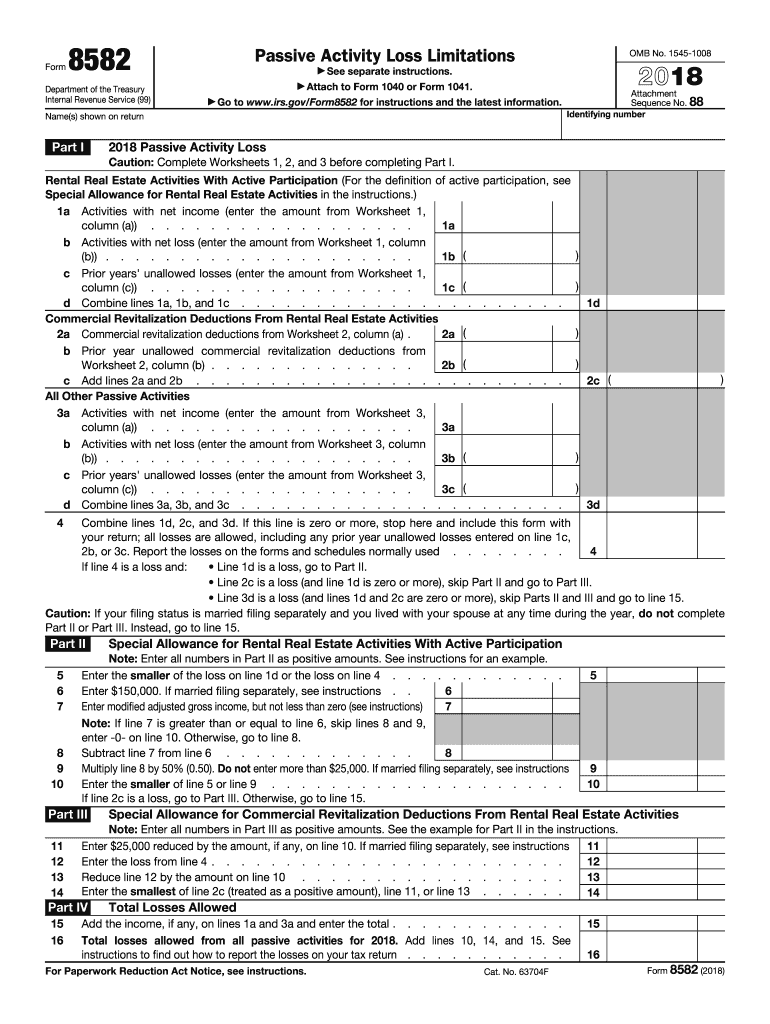

Tax Form 8582, commonly referred to as the PAL form, is utilized by the Internal Revenue Service (IRS) to monitor Passive Activity Loss Limitations. It is designed for taxpayers who need to report financial losses from passive activities such as rental properties and other business activities in which they do not materially participate. The form sets guidelines for calculating and reporting allowable losses, ensuring these do not exceed passive income.

How to Use the Tax Form 8 Instructions

- Identify Passive Activities: Begin by listing all your passive activities, which include rental properties and any business ventures where you do not actively participate.

- Calculate Income and Losses: Use the form to calculate both your income and any losses arising from these activities. The form provides worksheets to assist with this.

- Complete Worksheets: The 2017 instructions guide you through various worksheets to determine the amount of passive activity losses you can deduct.

- Transfer Amounts to Tax Return: Once you have completed the calculations, the instructions will help you identify where to report these figures on your main tax return.

Steps to Complete the Tax Form 8 Instructions

- Gather Required Information: Collect financial records for each passive activity, including profit/loss statements and previous year carryover amounts.

- Fill Out Worksheets: These worksheets are essential to figuring out your allowable passive losses. Ensure accuracy by double-checking figures.

- Total Passive Losses: Calculate the total of your current year passive losses and previously suspended losses.

- Report Totals on Main Tax Form: Use the instructions to accurately enter these totals in the correct sections on your primary tax submission.

Important Terms Related to Tax Form 8 Instructions

- Passive Activity: A business activity in which the taxpayer does not materially participate.

- Material Participation: Active involvement in the business on a regular, continuous, and substantial basis.

- Suspended Losses: Losses that cannot be deducted in the current year and must be carried forward to future tax years.

IRS Guidelines

The IRS guidelines for the 2017 tax year emphasize clarity and compliance. They outline the procedures for filing Form 8582 and detail the limitations on passive income losses. The IRS uses these rules to prevent excessive loss deductions, ensuring taxpayers only claim losses from allowable activities.

Filing Deadlines / Important Dates

Taxpayers must submit Form 8582 along with their federal tax return, generally due by April 15th. If the deadline falls on a weekend or holiday, the filing date shifts to the next business day. Staying aware of these deadlines is crucial to avoid late penalties.

Required Documents

To accurately complete Form 8582, you need:

- Income and loss statements from each passive activity.

- Previous year's tax return to verify carryover losses.

- Statements of expenses associated with passive activities, such as maintenance and management fees.

Software Compatibility (TurboTax, QuickBooks, etc.)

Form 8582 can be seamlessly integrated with most tax preparation software like TurboTax and QuickBooks. These platforms offer automated calculations for allowable losses and can import data directly from related financial records, ensuring accurate and efficient tax filing.

Eligibility Criteria

Form 8582 is required if you are reporting losses from passive activities. To claim these losses, taxpayers must meet criteria set by the IRS, such as owning rental properties or running a business with limited participation. It is imperative to ensure that all activities comply with the IRS's definition of passive activities to avoid filing errors.