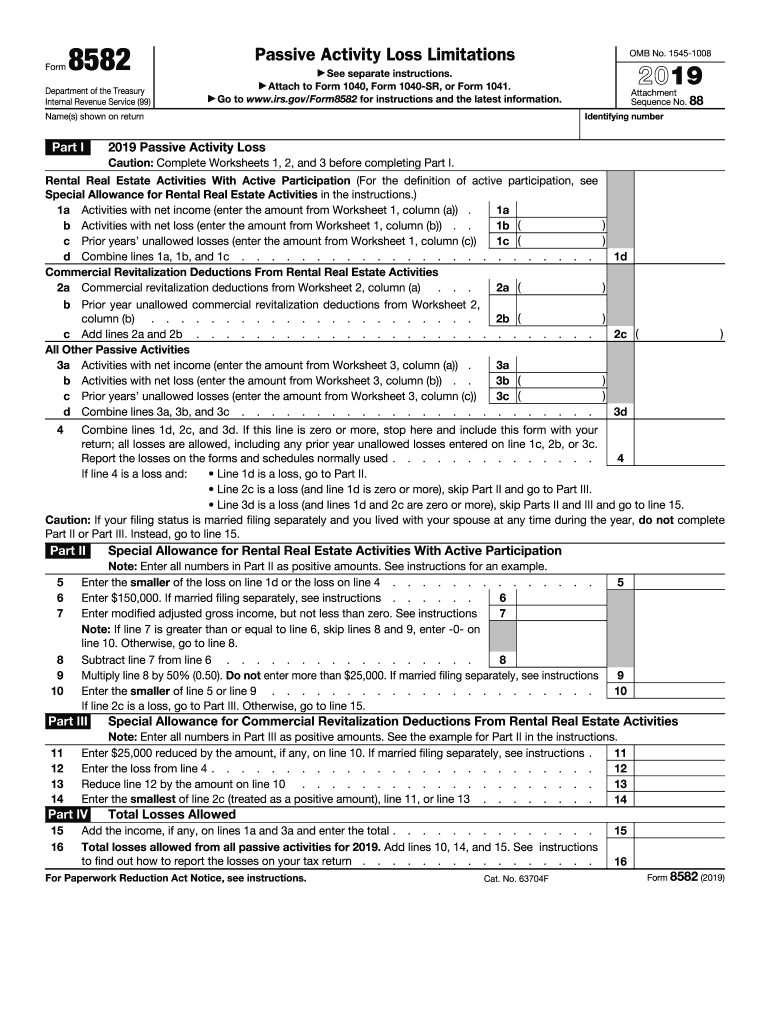

Definition and Meaning of Form 8582

Form 8582, used by the Internal Revenue Service (IRS), is aimed at reporting passive activity loss limitations. For the year 2018, this tax form helps taxpayers calculate and report losses arising from passive activities, including rental real estate and other similar activities where the taxpayer does not materially participate.

The form is crucial for ensuring compliance with IRS regulations about passive activity loss limitations. These limitations were established to differentiate between passive and non-passive income, preventing taxpayers from using losses from passive income to offset active income.

How to Use Form 8

To use Form 8582 effectively, taxpayers must understand the distinction between passive and active income activities. The form subdivides activities based on their nature and the taxpayer’s level of involvement.

-

Identify Passive Activities:

- Activities include rental properties and businesses where the owner does not partake in day-to-day operations.

-

Detail Income and Losses:

- Report all income and expenses related to passive activities. Use worksheets that accompany the form to calculate any deductions accurately.

-

Apply Loss Limitations:

- Input detailed figures into relevant sections that calculate allowed deductions under passive activity loss rules.

Using detailed worksheets within the key sections of Form 8582 is essential for accuracy and compliance.

Steps to Complete Form 8

Completing Form 8582 correctly requires understanding each section and its requirements. The process involves several steps:

-

Gather Necessary Documents:

- Collect all financial documents related to passive activities, including income reports, expense details, and previous tax filings.

-

Complete Worksheets:

- Use the included worksheets to break down the calculations of passive activity gains and losses before transferring these figures to the main form.

-

Fill the Main Sections:

- Enter the totals from the worksheets into the corresponding lines in Form 8582. Confirm that all numbers accurately reflect your passive activities.

-

Review for Accuracy:

- Double-check all entries against your financial documents to avoid discrepancies that could lead to IRS audits.

Importance of Form 8582

Form 8582 plays a critical role in tax compliance, particularly for those with substantial passive income sources. Its importance lies in:

-

Ensuring Legal Compliance:

- Helps taxpayers adhere to IRS rules that limit the use of passive losses, preventing improper deductions against non-passive income.

-

Accurate Deductions:

- Enables the correct calculation of deductible losses, optimizing tax savings without violating federal tax laws.

-

IRS Transparency:

- Provides a clear report of passive activities to the IRS, reducing the risk of audits and associated penalties.

Legal Use of Form 8582

The legal use of Form 8582 involves adhering to guidelines established under the Tax Reform Act. The act delineates when and how losses from passive activities can be claimed:

-

Material Participation Rules:

- Defines whether an activity qualifies as passive, based on the taxpayer’s involvement.

-

Special Allowable Losses:

- Some exceptions allow for greater losses, such as rentals under certain conditions or groupings of similar activities.

Non-compliance with these guidelines can lead to penalties or increased scrutiny from tax authorities.

Key Elements of Form 8582

The critical components of Form 8582 include:

-

Passive Activity Information:

- Sections dedicated to detailing each passive activity and relevant financial figures.

-

Loss Limitation Calculations:

- Worksheets guiding the calculation of losses allowed under passive activity rules.

-

Carryover Provisions:

- Specific lines indicating amounts carried over to future tax years if full deductions aren’t permissible in the current year.

Understanding these elements ensures a comprehensive and accurate filing.

IRS Guidelines for Form 8582

IRS guidelines for Form 8582 articulate the need for transparency and precision in reporting passive income activities. Guidelines are provided in IRS publications that detail:

-

Instructions for Completion:

- How to fill each section of the form, including common mistakes and best practices.

-

Restrictions on Passive Loss Utilization:

- Clarification on limits for deducting passive losses against active income.

Disregarding these guidelines could result in rejected filings or penalties.

Filing Deadlines and Important Dates

The deadline for submitting Form 8582 typically aligns with annual federal tax filings, usually due by April 15 following the tax year. Key dates to remember include:

-

Annual Filing Deadline:

- April 15, but extensions may apply if you file Form 4868.

-

Extension Periods:

- Allows taxpayers additional time, generally until October 15, to submit completed forms without penalties.

Meeting these deadlines is crucial in avoiding late fees and ensuring all tax obligations are met timely.