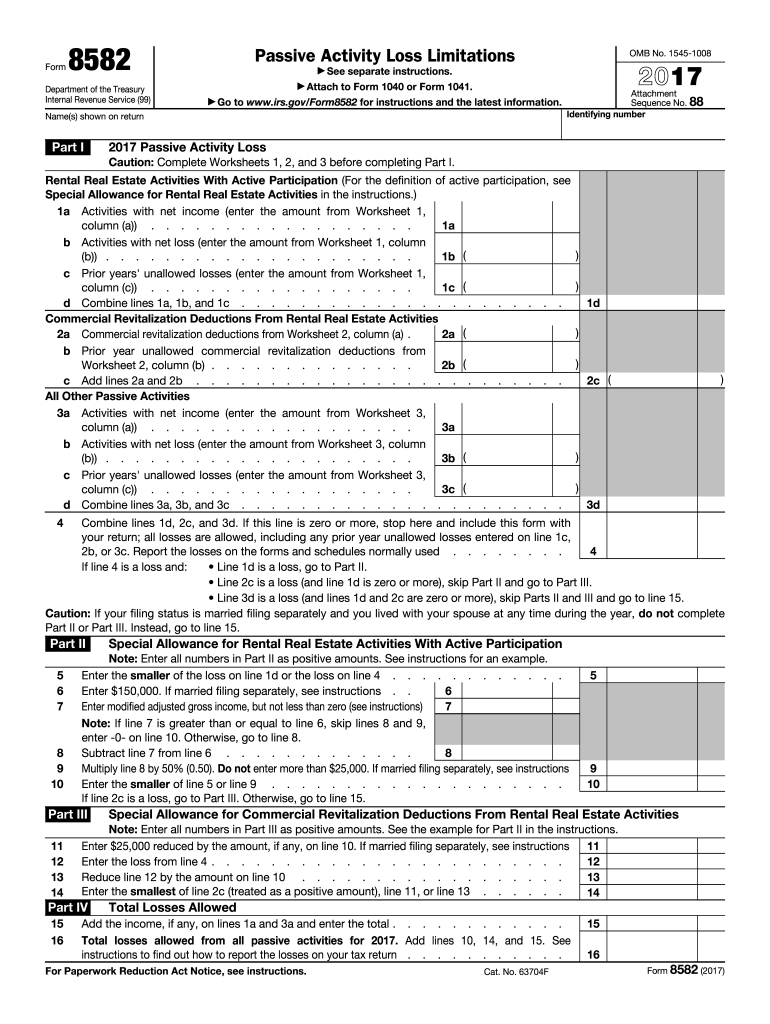

Understanding Form 8582 for Passive Activity Losses

Form 8582, an IRS-sanctioned document, serves a critical function in managing passive activity loss limitations for both individuals and estates. Its primary purpose is to help taxpayers calculate and report losses generated from various passive activities, such as rental real estate and commercial revitalization deductions. With careful application, this form allows taxpayers to understand and appropriately manage their passive activity financials.

Passive Activities Defined

Passive activities generally consist of trade or business activities in which a taxpayer does not materially participate. This includes rentals, even if there is active involvement, unless exceptions apply. Passive activity limitations can affect the total amount of deductible losses, thus making Form 8582 essential in the proper reporting of these financial structures.

Step-by-Step Instructions for Completing Form 8582

- Review IRS Instructions: Beginning with a thorough review of the IRS instructions for Form 8582 can provide clarity on data requirements and prevent errors.

- Enter Income Information: Start by entering your total rental real estate activity income and any other passive income sources in the designated sections of the form.

- Record Passive Activity Deductions: Carefully document any expenditures related to your passive activities, ensuring consistency with previous tax filings.

- Utilize Worksheets: Form 8582 includes necessary worksheets that help calculate the allowable losses deductibles, integrating details like gains and losses from prior years.

- Verify Entries: Conduct a detailed review of all entered data to confirm its accuracy before submission. Cross-reference this information against your financial and tax documents.

Considerations for Using Form 8582

Form 8582 requires a rigorous approach to correctly capture financial nuances associated with passive activities. Pay attention to how state-specific tax codes might affect filings, particularly if managing investments across multiple states.

Methods to Obtain Form 8582

- Electronic Access: The form is readily available for download directly from the IRS website. Utilizing this method also ensures access to the most updated version.

- Tax Software: Form 8582 is supported by widely-used tax software, facilitating integration with other digital tax documents and simplifying the filing process.

- Professional Tax Services: Engage accountants or tax preparation services who can provide personalized guidance and aid in obtaining and completing the form.

Importance of Form 8582

This form is pivotal to legally optimizing tax liabilities by accurately reporting permissible deductions from passive losses. Properly completing Form 8582 helps prevent potential IRS audits triggered by improperly recorded losses that exceed allowable limits.

Eligibility Criteria for Filing Form 8582

Eligibility for utilizing this form generally hinges on the involvement in passive activity investments, such as:

- Individuals generating income from rental properties.

- Estates that hold interests in passive activities.

- Taxpayers exceeding income thresholds where passive activity loss limitations become applicable.

Considerations for Different Taxpayer Scenarios

- Self-employed Individuals: Need to balance passive activity gains without skewing personal income tax liabilities.

- Retirees: May increasingly rely on rental income, affecting how losses are reported and offset.

- Students with Property Investments: Require careful documentation to effectively balance academic financial assistance and rental income deductions.

Examples of Utilizing Form 8582

Examples often bring clarity to the practical application of Form 8582:

- Rental Properties: A taxpayer with multiple rental properties uses Form 8582 to track cumulative annual losses, balancing them against any gains.

- Investment Partnerships: For those involved in partnerships holding passive income interests, the form aids in the equitable distribution of losses among various stakeholders.

Software Compatibility with Form 8582

Common tax preparation tools like TurboTax and QuickBooks recognize Form 8582, streamlining the integration of passive activity reporting within broader tax filings. Their step-by-step guides can ease the data entry process, reducing errors and ensuring compliance.

Penalties and Compliance Considerations

Neglecting to file Form 8582 or submitting incorrect data can lead to costly audits and penalties. It is crucial to uphold stringent review standards and maintain comprehensive documentation to substantiate all submitted data.

Ensuring Legal Compliance

Adherence to IRS regulations regarding passive activity loss limitations not only facilitates legal tax deductions but also mitigates potential legal complications from inaccurate filing. Regular consultation with IRS updates on policy changes ensures ongoing compliance.