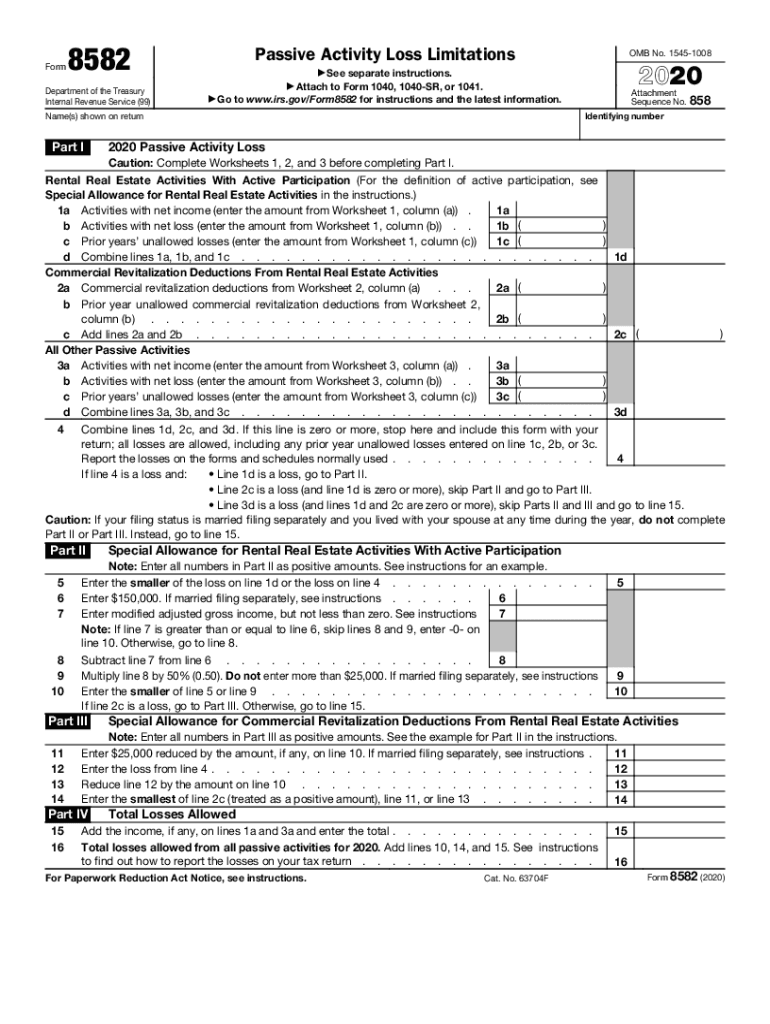

Definition and Purpose of Form 8582

Form 8582, issued by the IRS, is used to report passive activity loss limitations. This form plays a crucial role for taxpayers who own rental real estate or other passive income-generating activities and are subject to passive loss restrictions. The form calculates the allowed losses based on the taxpayer’s income and pending passive activity losses carried over from previous years. It ensures that individuals do not offset more income than IRS regulations permit, maintaining compliance with tax rules.

Key Elements of Form 8582

Form 8582 includes several critical sections that taxpayers need to carefully complete:

- Part I – 2020 Passive Activity Losses: This section addresses losses from activities that fall under passive income rules, including rental real estate. Taxpayers must list their current year losses.

- Part II – Special Allowance for Rental Real Estate: Allows up to $25,000 of combined deductions from rental real estate activities if specific criteria are met, such as adjusted gross income being below $150,000.

- Part III – Computation of Allowable Passive Activity Losses: To determine the amount of losses that can be deducted, calculated by considering suspended losses carried over from previous years.

Understanding each part ensures accurate reporting and compliance with IRS guidelines.

Steps to Complete Form 8582

Completing Form 8582 requires careful attention to detail. Here is a step-by-step guide to help:

- Gather Required Documents: Before starting, collect all records of passive activity income, losses, prior year disallowed losses, and current year income.

- Fill Out Part I: Enter the current year’s passive losses from trade, business, or rental real estate activities.

- Calculate Potential Special Allowance: Use Part II to determine eligibility for a special $25,000 allowance for rental real estate losses.

- Determine Allowable Losses: Part III requires you to calculate total deductions allowed by aggregating suspended and current year expenses.

- Review and Verify: Double-check all figures and entries to ensure accuracy and compliance with IRS regulations.

- Submit the Form: Once completed, attach Form 8582 to the main income tax return and file it by the designated deadline.

Who Typically Uses Form 8582?

Form 8582 is primarily used by individual taxpayers who:

- Are involved in rental real estate activities that generate passive income or losses.

- Own partnerships or S corporations with passive activities that generate losses.

- Have prior unallowed passive losses that may be deductible in the current tax year.

This form is not required for taxpayers who meet the criteria for material participation in businesses or activities.

How to Obtain Form 8582

Taxpayers can easily access Form 8582 through multiple methods:

- IRS Website: The form is available for download as a PDF from the IRS official site, ensuring the latest version and instructions.

- Tax Preparation Software: Software like TurboTax and H&R Block includes integrated versions of Form 8582 for ease of use during tax preparation.

- Professional Tax Preparers: Many tax professionals provide the necessary forms as part of their service package.

Software Compatibility for Form 8582

Form 8582 is compatible with most mainstream tax software platforms, which streamline the data input and calculation process:

- TurboTax and H&R Block: These platforms offer guided walkthroughs that simplify the completion of this form through user-friendly interfaces.

- QuickBooks: For business entities, QuickBooks integrates financial data that can be transferred to tax schedules, supporting accurate passive loss reporting.

IRS Guidelines and Compliance

The IRS provides specific guidelines and documentation requirements for Form 8582:

- Publication 925: This resource offers comprehensive details on passive activity rules, including exceptions and examples.

- Consistent Record-Keeping: Maintain comprehensive records over several years to substantiate claims of passive losses and future applications of these losses.

- Suspended Losses: Taxpayers must calculate and carry over any disallowed losses to future years, per IRS guidelines, until offsetting passive income is available.

Penalties and Important Filing Dates

Failure to accurately complete Form 8582 or comply with IRS regulations can lead to penalties:

- Penalties for Misreporting: Incorrect filings can result in fines and interest on unpaid taxes if losses are improperly deducted.

- Important Filing Dates: Align completion of Form 8582 with the general federal income tax deadline, typically April 15, unless extensions have been filed.

Taxpayer Scenarios and Examples

To illustrate the application of Form 8582, here are scenarios where the form is essential:

- Rental Property Owners: Mary owns three rental properties and incurs a significant loss in a tax year. She uses Form 8582 to report her losses and carry over unallowed losses.

- Limited Partnerships: John receives a K-1 from a limited partnership that has generated a passive loss. He reports the loss on Form 8582 to comply with passive activity limitations.

These diverse cases highlight the importance of Form 8582 for different taxpayer situations, applicable across various sectors with different tax obligations.