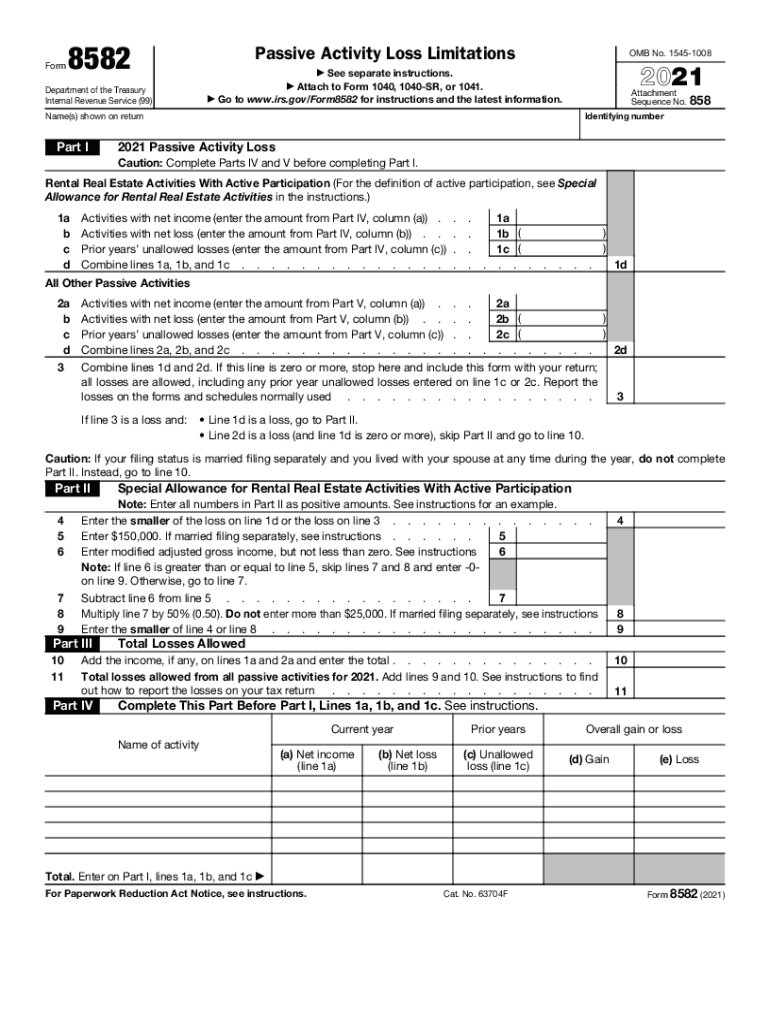

Definition and Purpose of Form 8582

Form 8582, or the Passive Activity Loss Limitations form, is utilized by taxpayers in the United States to report their passive activity losses. The primary purpose of this form is to calculate and disclose any losses derived from passive activities, particularly rental real estate activities where the taxpayer actively participates. Passive activity losses typically cannot offset non-passive income, making Form 8582 essential for properly accounting for those losses within the confines set by the Internal Revenue Service (IRS). Understanding the specific nuances of how passive losses are limited under IRS regulations is crucial for accurate tax reporting.

Key Elements of Form 8582

Form 8582 is structured to ensure a detailed calculation of passive activity losses. It includes several key elements:

- Net Income and Net Loss Worksheets: These worksheets aid in calculating the net income and losses from passive activities.

- Unallowed Losses from Prior Years: This section allows for the reporting of losses that were not permitted in previous years, which may affect current loss calculations.

- Modified Adjusted Gross Income (MAGI) Impact: The form instructs on assessing allowable losses based on the taxpayer's MAGI, recognizing the interplay with passive activity loss limitations.

Important Terms Related to Form 8582

A comprehensive understanding of Form 8582 requires familiarity with specific terms:

- Passive Activity: Activities in which the taxpayer does not materially participate, such as rental operations or limited partnership interests.

- Material Participation: Active involvement in an activity, as opposed to passive involvement, impacting the treatment of losses.

- Tax Shelter: Any investment specifically designed to generate tax deductions or defer income tax.

How to Use Form 8582

Form 8582 is employed by taxpayers for detailed accounting of passive losses. To maximize the utility of this form, taxpayers should begin by listing each passive activity along with the corresponding income or loss. Subsequently, apply the passive activity loss rules to determine the allowable deductions for the tax year, ensuring that unallowed losses are appropriately carried over to future years for potential deduction.

Steps to Complete Form 8582

Completing Form 8582 involves a series of calculated steps:

- Gather Required Information: Collect data on all passive income, losses, and previous year carryovers.

- Determine Gross Income and Total Deductions: Input these figures to calculate the net income or loss per passive activity.

- Calculate Allowable Losses: Use IRS instructions to determine allowable passive activity losses, influenced by total income levels and loss limitations.

- Report and Carry Forward Unallowed Losses: Unallowed losses must be reported and will typically carry forward to subsequent tax years.

IRS Guidelines for Form 8582

The IRS provides specific guidelines governing the submission of Form 8582 to ensure compliance with tax regulations. Instructions emphasize the taxpayer's need to accurately report the total amount of passive activity income and losses each year. The guidance also elucidates calculation methods and criteria for passive versus active participation in activities, necessary to properly claim and limit losses.

Penalties for Non-Compliance

Failing to properly complete Form 8582 can result in significant penalties from the IRS. Non-compliance may lead to fines, audits, and further scrutiny of the taxpayer's returns. Taxpayers must ensure that all passive activity loss calculations are consistently accurate to avoid these repercussions.

Software Compatibility and Filing Methods

Form 8582 is compatible with various tax preparation software, such as TurboTax and QuickBooks, which help streamline the filing process. These software solutions often include modules for passive activity calculations, automatically capping losses according to IRS rules and facilitating electronic filing.

Submission Methods: Online, Mail, and In-Person

Taxpayers have multiple submission methods for Form 8582:

- Online Filing: This is typically the most efficient method, often integrated with tax software for automatic electronic submission.

- Mailing the Form: A traditional method suitable for those preferring physical documentation, albeit slower in processing.

- In-Person Submission: Submission can also be completed at IRS field offices, though this method is less common.

Eligibility Criteria for Using Form 8582

Eligibility to utilize Form 8582 extends to individuals, estates, and trusts engaged in passive activities but restricted by certain thresholds for active participants. Specifically, taxpayers who own rental properties or limited partnerships may find themselves required to file this form to justify their passive activity losses against any income.

State-by-State Differences

While Form 8582 is a federal requirement, different states may have unique regulations and treatments for passive activity losses. Taxpayers should verify their state-specific obligations to ensure comprehensive compliance.

By providing detailed explanations, multiple examples, and structured guidance, this content ensures taxpayers are well-informed about Form 8582, its criteria, and processes.