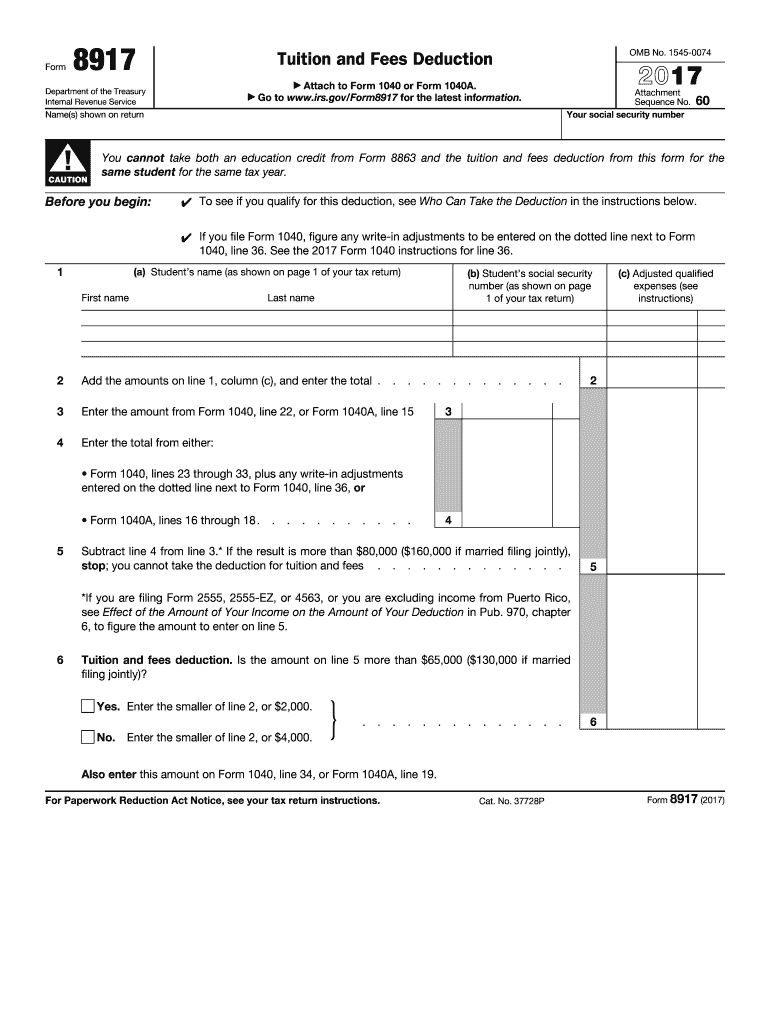

Definition & Meaning

Form 8917, officially known as the Tuition and Fees Deduction Form, is utilized by taxpayers in the United States to claim an educational expense deduction for qualified tuition and related fees paid during a tax year. For the 2013 tax year, this form allowed taxpayers to deduct up to $4,000 from their taxable income for tuition paid for themselves, their spouse, or dependent children. The deductions apply only if the expenses relate to post-secondary education and meet specific eligibility criteria. Importantly, this deduction cannot be claimed in conjunction with educational credits like the American Opportunity Credit or Lifetime Learning Credit for the same student in the same year.

Eligibility Criteria

To qualify for the tuition and fees deduction using the 2013 Form 8917, taxpayers must meet certain income limitations, which vary depending on filing status. For instance, single filers had to have a modified adjusted gross income (MAGI) of $80,000 or less, while married couples filing jointly needed a MAGI of $160,000 or less. Additionally, the deduction was available only if the tuition was paid to an eligible educational institution and the taxpayer was not claimed as a dependent on another person's tax return. Students must have been enrolled in eligible programs at least part-time to qualify.

Steps to Complete the 2013 Form 8917

-

Complete Personal Information: Fill in your name and Social Security number at the top of the form.

-

Enter Tuition and Fees: Calculate and enter the total amount of tuition and related fees paid in 2013. This figure should reflect only qualified expenses that are not covered by scholarships or similar financial aid.

-

Determine Deduction Amount: Use the IRS instructions provided with the form to determine the deduction you are eligible for, adjusting for any income limitations and restrictions.

-

File with Your Return: Attach the completed Form 8917 to your federal tax return for 2013 when filing, ensuring that all information is accurate and complete.

Important Terms Related to 2013 Form 8917

-

Qualified Education Expenses: Tuition and required enrollment fees for eligible post-secondary institutions, excluding costs for books, room, board, and other personal expenses.

-

Modified Adjusted Gross Income (MAGI): A calculation used by the IRS to determine eligibility for certain tax benefits, including the tuition and fees deduction.

-

Eligible Educational Institution: Any university, college, or vocational school that participates in student aid programs administered by the U.S. Department of Education.

How to Obtain the 2013 Form 8917

Individuals could obtain the 2013 Form 8917 directly from the IRS website as a downloadable PDF. Alternatively, it was available at IRS offices or could be requested by mail. For those using tax software like TurboTax or QuickBooks, the form was typically included as part of the tax preparation package, streamlining the process of completing and filing tax returns.

IRS Guidelines

The IRS provided comprehensive guidelines accompanying Form 8917 to ensure taxpayers correctly applied for the tuition and fees deduction. Guidance included clarifications on eligible expenses, step-by-step instructions for calculating deductions, and illustrative examples to highlight common scenarios. Taxpayers were advised to carefully review these guidelines to maximize deduction benefits and comply with tax regulations.

Key Elements of the 2013 Form 8917

-

Personal and Student Information: Identifies the taxpayer and eligible student for whom the deduction is claimed.

-

Calculation of Deduction: Requires taxpayers to meticulously calculate all qualified expenses, considering deductibility limits.

-

Income Eligibility Verification: Taxpayers must provide income details to ascertain eligibility based on the MAGI thresholds.

Who Typically Uses the 2013 Form 8917

The form was primarily used by individual taxpayers who paid qualified tuition and related fees in 2013 for post-secondary education. This included parents supporting dependent children in college, independent students funding their own education, and spouses who attended educational programs to improve career prospects. Users of this form sought to reduce their taxable income by deducting allowable education expenses, understanding that they could not double-claim via education credits.

Filing Deadlines / Important Dates

The filing deadline for using the 2013 Form 8917 coincided with the traditional federal tax filing deadline—typically April 15, 2014. Taxpayers requiring an extension had until October 15, 2014, to file the completed form with their tax return, as long as they had filed for an extension. Timeliness was crucial to ensure eligibility for deductions in the relevant tax year.